Cheniere Board of Directors Appoints Board Members to Run the Company Until New CEO Found

Cheniere Energy’s (ticker: LNG) first LNG shipment is just weeks away, and the man who co-founded the colossal operation will not be present to witness his company’s achievement.

Charif Souki, the former Chairman, President and Chief Executive Officer of Cheniere Energy, has been removed from his position effective immediately, the company said in a news release on Sunday, December 13, 2015. Souki co-founded Cheniere Energy in 1996 and guided the company from an unknown to one that revolutionized the highly publicized (and highly capital intensive) LNG market. The undertaking was massive – costs neared $20 billion and involved more than a decade of development and construction, but the first LNG export terminal in the United States is rapidly approaching the finish line.

In the meantime, Cheniere will be searching for a new CEO after the Board of Directors removed Souki from his position. Two board members will serve as interims for Souki’s titles until successors are named.

The Buildup

Charif Souki is certainly an interesting enigma: his early background included starting a high-end restaurant and managing global investments before eventually discovering a niche in the oil and gas industry. The sight of Cheniere’s export facility is one to behold, and is even more impressive to consider Souki basically started from scratch. In a June 2001, the Beirut-born Souki visited 30 private equity firms in hopes of raising cash for his multi-billion dollar venture. He returned without a dime.

A minor breakthrough finally occurred in 2002, via a partnership with Freeport LNG. The partnership eventually disbanded, but not before Souki began developing an import terminal (keep in mind, this was before the shale boom) and signed two oil majors to 20-year deals with annual commitments of $250 million. After surviving the industry downturn of 2008 and reshaping his company to an export terminal, he secured an $8 billion contract with BG Group and received billion dollar investments from overseas governments and private equity groups.

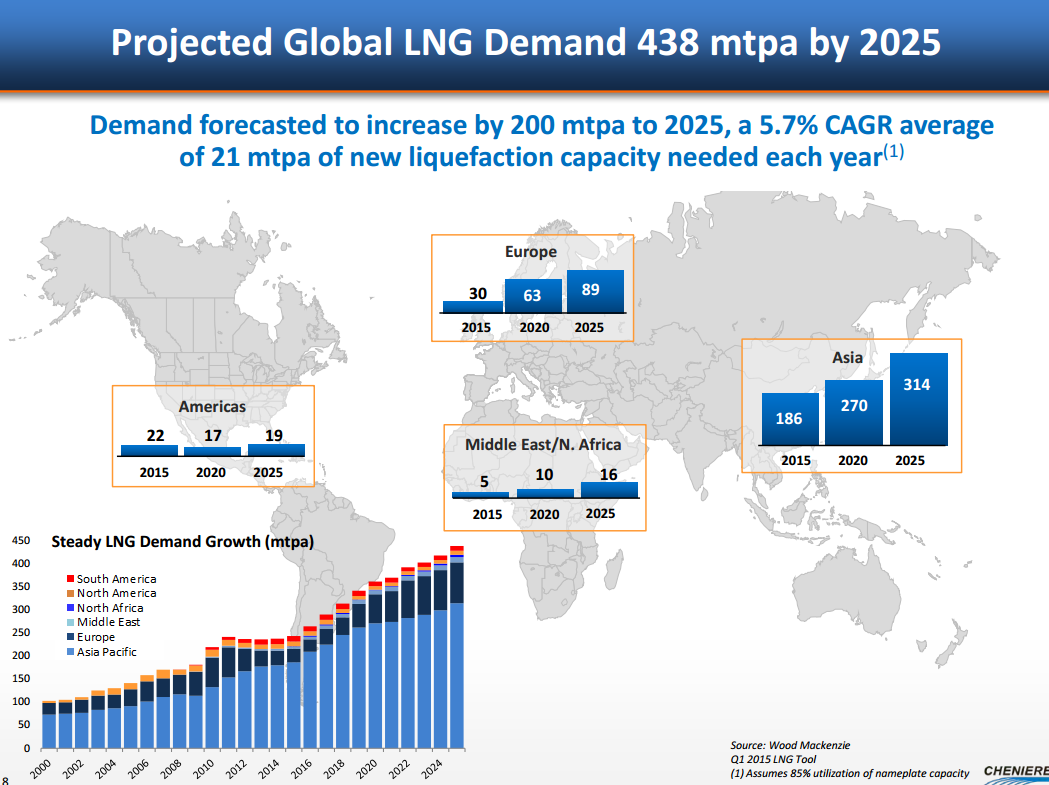

Source: Cheniere 2015 Analyst Day Presentation

Today, roughly 80% of Cheniere’s LNG is contracted to buyers that are required to pay annual fees, regardless if they choose to take the product or not. Sabine Pass, the first phase of Cheniere’s LNG projects, will hold export capacity of 3.8 Bcf/d once all six trains are completed. The terminal now stands as the beacon of an industry whose high costs have come under intense scrutiny and doubt in the midst of the latest commodity downturn. It stands to eventually bring in more than $4 billion in annual fees.

The Conflict

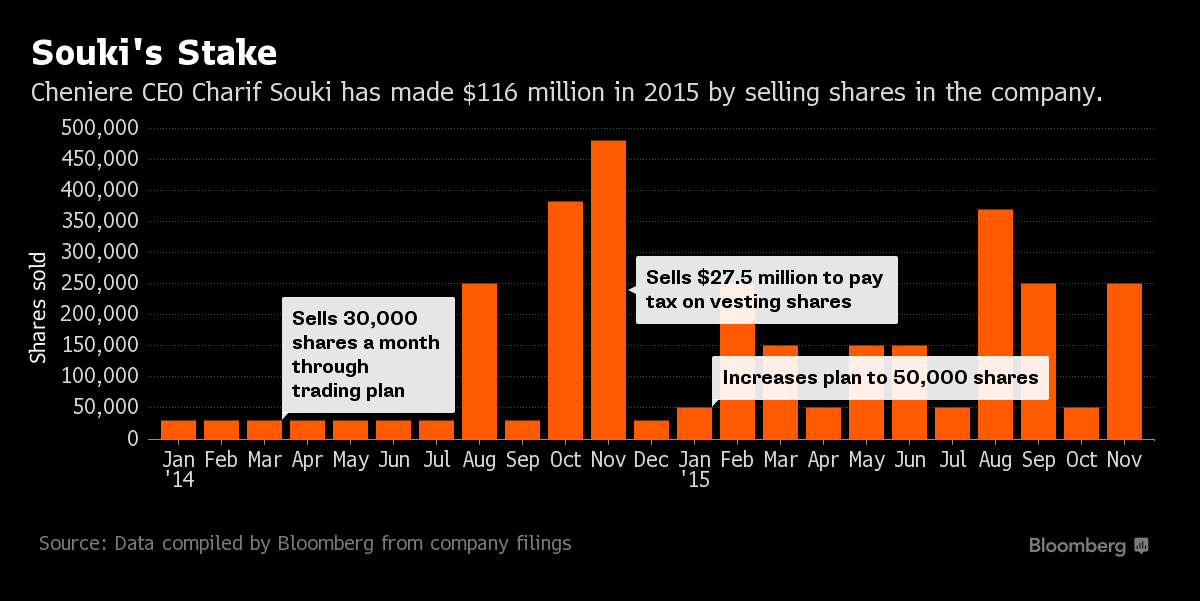

Today, Cheniere has a market capitalization of nearly $10 billion – similar in size to larger E&Ps like Continental Resources (ticker: CLR), EQT Corp. (ticker: EQT) and Cimarex Energy (ticker: XEC). A major difference among the four is that Cheniere has yet to deliver any of its product to market, reflecting Souki’s remarkable achievement of locking in significant investments and long term sales contracts. Shareholders rewarded management by distributing 27 million shares among current employees in 2011 and 2013. Those same shareholders revolted upon discovering Souki’s total compensation in 2014 was $142 million. Roughly $130 million was from the stocks, and Souki has unloaded more than $150 million in shares since September 2014.

A class action lawsuit against the company was settled in March 2015, which included restraints on stock grants for management. Cheniere executives denied any wrongdoing.

The Shakeup

While Souki was dealing away his shares, a prominent Wall Street figure was snatching them up. Carl Icahn, an activist shareholder with the largest stake in Apple Inc. (ticker: AAPL), among others, began disclosing purchases in Cheniere. By September 2015, Icahn snatched up roughly 9.59% of all LNG shares and criticized the direction of management. Shortly afterwards, Icahn secured two seats on the board, increasing the numbers of directors to 11 from nine. Critics believed his influence could “more closely align management with shareholders.” Icahn’s stake had climbed to about 14% of outstanding shares the day Souki was dismissed. Cheniere did not disclose the exact voting results from the Board.

Icahn released a short statement addressing the Board’s decision. It reads:

“There is no doubt that Charif Souki has proven that he is a talented entrepreneur but at this time there is also little doubt that the board wished to move the company in a direction that differed greatly from the path Mr. Souki wanted. It is also telling that Mr. Souki sold a great deal of his stock, which made it somewhat easier for him to “swing for the fences” making it a win-win for Mr. Souki but not necessarily for the shareholders.

“I thank Mr. Souki for helping to build a great company. I also thank Mr. Neal Shear and Mr. G. Andrea Botta for stepping in at this time, but most importantly I thank and congratulate the board for having the “guts” to take these actions, which I fully support.”

The Analysis

Icahn entering the fold certainly piqued interest among the investment community, and many believed Cheniere Energy would eventually reach a fork in the road that could determine the fate of management moving forward. “The termination of Mr. Souki was abrupt although not completely unexpected given that recent shareholder activism was at odds with Mr. Souki’s goals of reinvesting Cheniere’s free cash flow in other parts of the energy value chain,” said a note from Faisel Khan of Citigroup. “Our concern is that Mr. Souki’s sudden departure could cause other critical management team members to leave the firm… We believe it is critical that certain management team members remain in place.”

A general consensus among analysts is that Icahn’s goal of unifying shareholders is on track. Seaport Global Securities said, “We expect that improving shareholder value by establishing a clear path for returning capital to shareholders will come under increasing focus following this management change.” Citigroup also said Souki’s intention of “reinvesting all cash flows,” a sharp change from previous dividend plans, is now out the window.

“There isn’t an obvious catalyst that we can see,” said analysts of Raymond James Equity Research. Tudor Pickering Holt & Co. called the announcement “pretty darn shocking” in their note.

In a telephone interview with Bloomberg, Souki disagreed with Icahn’s assessment regarding his stock sales and said he still plans to be a “vocal investor.” The former Cheniere chief executive also said the Board did “what was best for the company” and still considers them to be longtime friends.

Oil & Gas 360® conducted the following interview with Souki in August 2015.