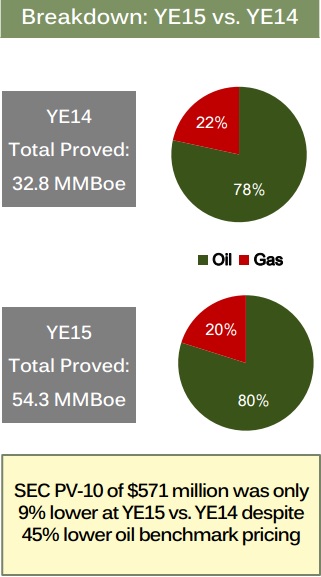

Year-End 2015 Proved Reserves Increase by 65%

In an operational update on February 1, 2016, Callon Petroleum (ticker: CPE, callon.com) maintained its goal for cash flow neutrality by mid-2016 while announcing advancements in both production and its reserve base.

For fiscal 2016, Callon expects average production of 11,500 to 12,000 BOEPD, representing a midpoint year-over-year increase of 23%, based on estimates from Q3’15. Its previous 2015 estimates may come above guidance, however, as CPE announced Q4’15 production of 10,500 to 10,700 BOEPD (80% oil volumes) – beating previous guidance of 10,200 to 10,500 BOEPD. Fred Callon, Chairman and Chief Executive Office of Callon Petroleum, attributed the volumes to “sustained performance from our Lower Spraberry program that has exceeded expectations.”

Lower Spraberry Overview

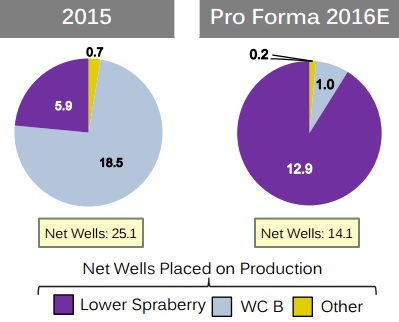

CPE, along with many of its peers, is dialing down its drilling program in the current environment with intentions to live within cash flows. The Mississippi-based exploration and production company plans on running one rig program in the near-term but assures the public that a second rig can be “quickly redeploy[ed]” in the event of a commodity rebound. In the meantime, its operational program will complete two to three wells per pad.

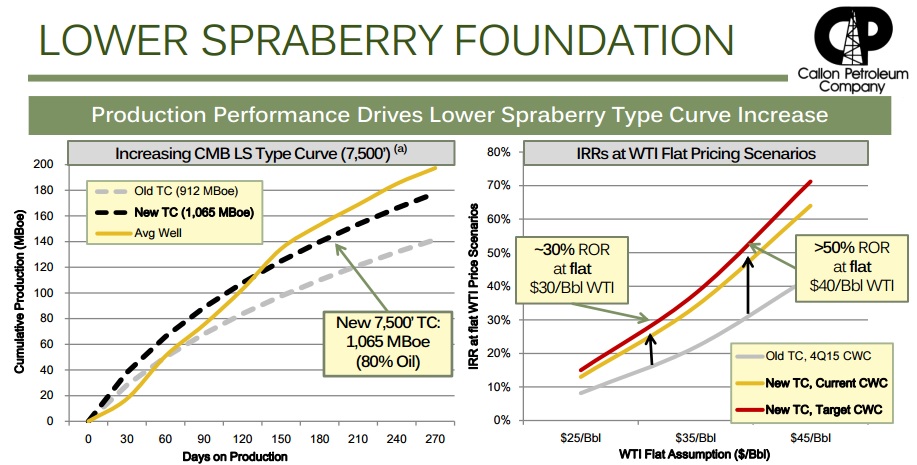

Many analysts have waited for CPE to update its type curves, and management obliged in its latest presentation. Updated type curves place Lower Spraberry EURs at 1,065 MBOE – an increase of 14% compared to previous curves of 912 MBOE. Operation costs are projected at $4.2 million for a 5,000 foot lateral well and $5.8 million for a 9,000 foot lateral well, down from previous estimates of $5.2 million for a 7,500 foot lateral. On a per capita basis at $30/barrel strip pricing, those 5,000 and 9,000 foot laterals can provide returns of 30% and 35%, respectively.

In the drilling update, CPE reported four Lower Spraberry wells brought online in Q4’15 returned peak 24-hour average IP rates of 1,000 BOEPD. When considering a 30-day average, the volume sustained an average of 781 BOEPD. In the update, CPE said it plans to target the Lower Spraberry “almost exclusively.”

Capital Spending Update

Due to results from its Lower Spraberry campaign, CPE management plans on a 2016 operational budget of $75 to $80 million, which is nearly half of 2015 levels. Despite the capital cut, the company believes its production volumes can increase from 20% to 25%.

An increased hedging profile baked additional security into forthcoming revenue, as its percentage of hedged oil production climbed to 63% from 60% at average weighted prices of $58.23/barrel.

An increased hedging profile baked additional security into forthcoming revenue, as its percentage of hedged oil production climbed to 63% from 60% at average weighted prices of $58.23/barrel.

As part of its one-rig program in 2016, Callon expects to place 19 gross (13.7 net) wells online, all of which will be located in the Central Midland Basin. The Lower Spraberry will host 17 gross (12.6 net) wells, with the remaining two (1.1 net) exploiting the Wolfcamp B formation. Callon brought one Wolfcamp B well online in Q4’15, resulting in peak 24-hour and 30-day initial production rates of 1,197 and 807 BOEPD, respectively.

Reserves Continue to Rise

An independent auditor listed CPE 2015 year-end proved reserves at 54.3 MMBOE (80% oil), an increase of 65% on a year-over-year basis. Approximately 53% of the property is classified as proved developed across its 109,918 net acres, pro forma for a recent acquisition of 4.9% working interest.

The footprint is slowly expanding, as transactions have been hard to come by in the United States’ chief producing basin. The working interest acquisition, announced in the company release, added net Q4’15 volumes of 170 BOEPD in the Casselman and Bohannon fields at a price of $9.3 million. Callon now owns a 71.3% working interest (53.5% net revenue interest) in the Cabo area, and a total of ten wells in the region are either drilling, completing or flowing back.

The footprint is slowly expanding, as transactions have been hard to come by in the United States’ chief producing basin. The working interest acquisition, announced in the company release, added net Q4’15 volumes of 170 BOEPD in the Casselman and Bohannon fields at a price of $9.3 million. Callon now owns a 71.3% working interest (53.5% net revenue interest) in the Cabo area, and a total of ten wells in the region are either drilling, completing or flowing back.

With the Cabo interest boost in consideration, Callon has spent $38.8 million to acquire 933 net surface acres dating back to Q4’15, adding 56 net horizontal drilling locations (42 in the Spraberry/Wolfcamp) to its portfolio. Average volumes from the acquired acreage is 530 BOEPD, amounting to a purchase price of about $73,200/flowing BOE. According to a recent CPE presentation, its costs per adjusted surface acre, along with de-risked horizontal locations, are the lowest among its peers.

Analyst Commentary

Chad Mabry, Senior Vice President of FBR Capital, called the update “overwhelmingly positive” in a note on February 1, 2016. Meanwhile, SunTrust Robinson Humphrey is forecasting Permian acquisitions and transactions to rise in the near term, and Johnson Rice & Company believes Callon is a “favored way to gain/increase exposure to the Permian Basin.”

Callon has plenty of dry powder to prolong its reduced operations, as it has only $40 million drawn on its $300 million borrowing base. Lease operating expenses are down more than 45% compared to Q3’14, adding to its efficiency on the development side. The company is scheduled to discuss its Q4’15 results via conference call on March 3, 2016.