Saudi Arabia sees a squeeze in liquidity as oil prices remain low

Demand for deposits dropped 4.7%, or about $13.5 billion, in Saudi Arabia over the course of October, forcing banks to borrow more from each other. The rate at which banks in Saudi Arabia lend overnight to each other jumped the most in seven years in November, the fifth straight month of increases, following the lower deposits in October, according to information from Bloomberg.

“The drop in deposits in October, in absolute amount, is probably the biggest since the 1990s,” Murad Ansari, a bank analyst at EFG-Hermes Holding SAE, said from Riyadh on Monday. “There are payment delays from the government to contractors, which is one of the reasons for the decline in private sector deposits, and public sector deposits are shrinking as the government is running a deficit.”

The squeeze on Saudi banks comes as the group continues to lead OPEC in a policy of defending market share over prices. About 90% of the government’s revenue comes from energy, meaning the drastic fall in oil prices since November of last year have put Saudi Arabia in a position where it has to run a deficit.

The three-month Saudi Interbank Offered Rate, which is used to price some loans, climbed 13 basis points this month to 1.11625 percent on Monday, according to data from the Saudi Arabian Monetary Agency on Bloomberg. That’s the biggest gain since October 2008 and the rate is at its highest since April 2009.

Standard & Poor’s lowered Saudi Arabia’s credit rating in October, citing concerns over the budget deficit, which S&P forecasts will increase to 16% of GDP this year. The Saudi riyal 12-month forward points rose 650 last week, the highest in more than 16 years, as investors bet the government would abandon its fixed exchange rate amid oil’s decline.

Tightening loans-to-deposits ratio

The loans-to-deposits ratio tightened to 83.8% in October 2015 from 82.5% a year earlier, indicating less liquidity. The government has borrowed at least 55 billion riyals ($14.7 billion) from local banks and institutions through bond issues this year to bridge its fiscal gap, which the International Monetary Fund projects will by more than 20% of economic output, up from 2.3% last year.

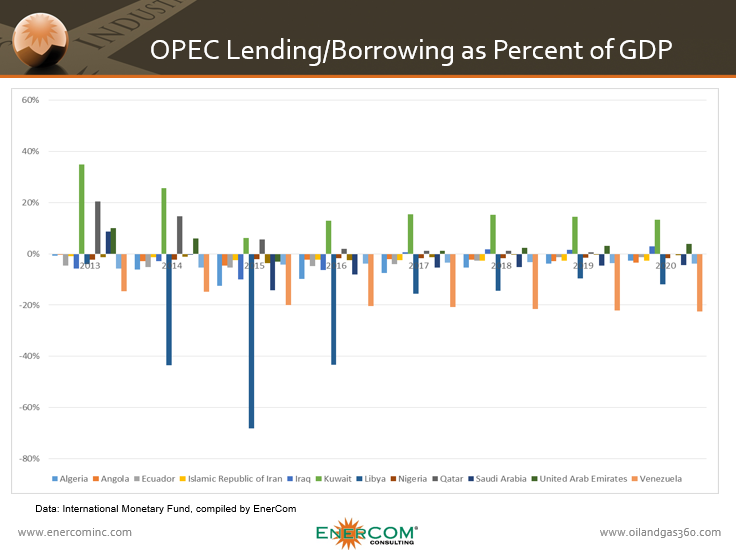

Borrowing is an OPEC-wide epidemic

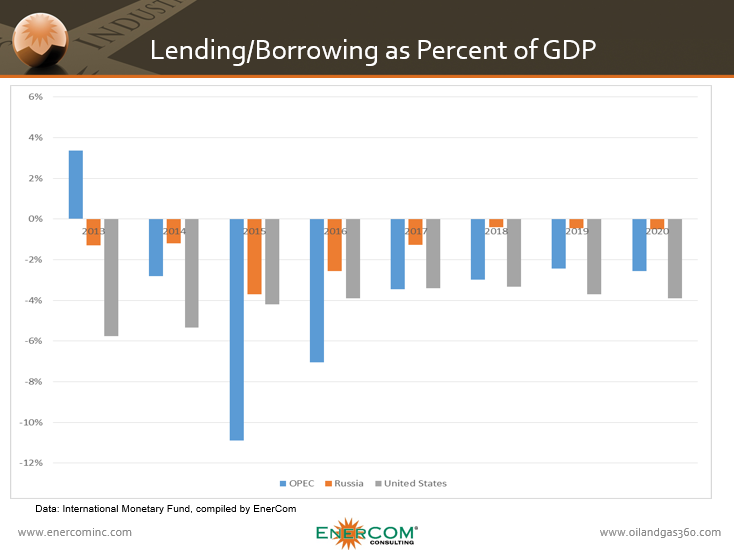

Saudi Arabia is not alone in needing to borrow more money in order to shore-up its budgets as the price of international crude benchmark Brent remains 61% below its high of $115.07 in June of last year. Many of OPEC’s members are not as well equipped financially to handle the decline in crude oil prices as Saudi Arabia.

Based on data from the IMF, the average borrowing as a percent of GDP for OPEC countries will exceed 10% this year, and remain above the 2.8% average seen in 2014 for the next five years.

Kuwait and Qatar are the only OPEC members expected to lend money, rather than borrow, this year, according to the IMF. Kuwait’s level of lending is expected to remain elevated compared to other OPEC members through the end of the decade, but most other members are not expected to fare as well. Libya, in particular, is expected to borrow large sums of money compared to its GDP over the next four years.

The IMF believes Libya will borrow roughly 68% of its GDP this year, and 43% next year, before falling back to the 10-15% range through the end of the decade. Venezuela, which has called on OPEC to change its policy and set a price floor, is expected to borrow 20-22% of its GDP this year through 2020 as its oil-dependent economy struggles to adjust to low crude oil prices.