Energy XXI (ticker: EXXI) is an independent oil and natural gas exploration and production company whose growth strategy emphasizes acquisitions, enhanced by its value-added organic drilling program. The company finalized the acquisition of EPL Oil & Gas on June 3, 2014, and is now the largest independent operating in the Gulf of Mexico with ownership of ten separate fields (nearly 800,000 net acres).

EXXI’s “acquire and exploit” strategy focuses on building its inventory and replacing reserves. At a conference on May 22, 2014, West Griffin, Chief Financial Officer of Energy XXI, said: “If you add up all of our acquisitions, we’ve acquired about 146 MMBOE of reserves, and we’ve proved almost 80 MMBOE of reserves.”

OAG360 notes that EXXI currently holds 261 MMBOE of reserves following the EPL acquisition, meaning 115 MMBOE, or 44% of its reserve base has been added through the drill bit.

Energy XXI is scheduled to make a 30-minute presentation in London during EnerCom’s London Oil & Gas Conference™ 6. The webcast of the presentation starts at 9:30 AM British Summer Time, or 4:30 AM U.S. Eastern Daylight Time, and can be accessed by clicking on this link.

Transaction Details

Source: EXXI June 2014 Presentation

Total consideration for the EPL acquisition was $2.30 billion. Included in the transaction was $1.02 billion in cash, roughly 23 million shares of EXXI stock and EPL’s full debt balance of $805 million. Energy XXI completed the private placement of $650 million in notes on May 12, 2014, to provide extra cash for the merger. Pro forma for the closing, EXXI now has 93 million shares outstanding. Its credit facility has been raised to $1.5 billion and will hold the majority of cash considerations to EPL. Since the acquisition costs are being deferred to the revolver, Energy XII has $980 million in liquidity.

“New Chapter”

In a press release confirming the merger, John Schiller, Chairman and Chief Executive Officer of Energy XXI, said: “This transaction begins a new chapter for Energy XXI. With assets that fit together hand-in-glove, along with the additional professionals who have joined our team, we have formed a stronger company focused on delivering value for our shareholders.”

Source: EXXI June 2014 Presentation

EXXI is now producing 62 MBOEPD (73% oil), representing a 51% increase compared to Q3’14 production of 41 MBOEPD (following a small divesture). Production totals for fiscal Q4’14 (EXXI’s fiscal year ends on June 30, 2014) will include one month of EPL’s volumes, and average quarterly production is expected to be 45 MBOEPD to 46 MBOEPD (68% oil). Due to the proximity of EPL’s assets, EXXI already has the infrastructure and facilities in place to proceed with development.

“The acquisition in itself is important,” said Antonio de Pinho , Executive Vice President, Exploitation & Exploration and Mergers & Acquisitions for Energy XXI. “But equally important is the overlap and the integration of our properties.”

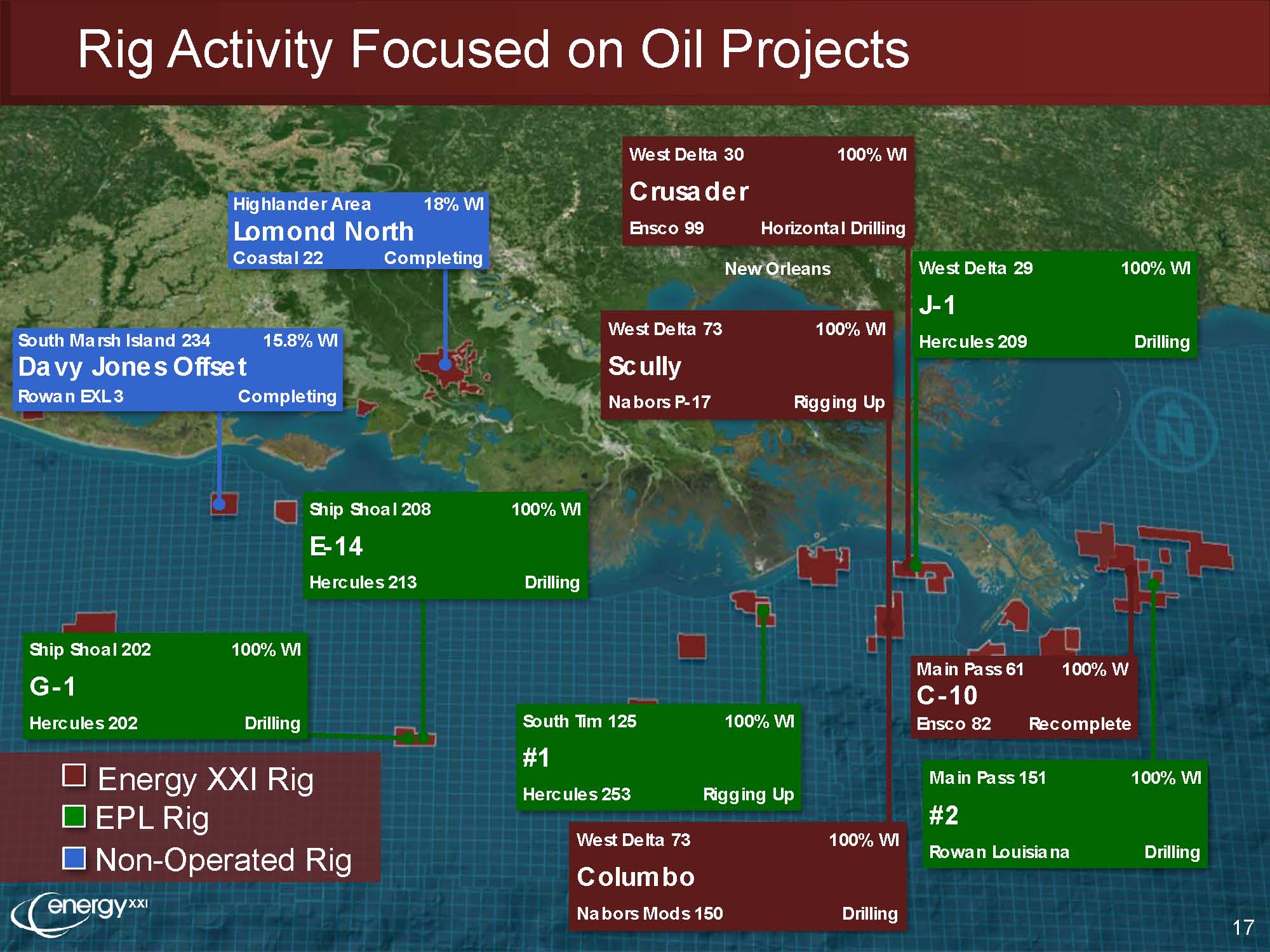

Updated Operations

EXXI has nine operated rigs (compared to four prior to the acquisition) running in the GOM and is focused on increasing its oil stream on low-risk development in established fields. Its Main Pass and West Delta (WD) 30 fields are identified as drivers moving forward, and its ongoing horizontal development drilling program targeting the WD 30 in addition to WD 73. Separate wells in both the WD 28 and 29 are expected to come online in July 2014 and represent an extension of operations in the WD 30 block.

Source: EXXI June 2014 Presentation

In its investor presentation, EXXI said its completed nine wells to date and an additional eight well locations have been identified as part of its fiscal 2014 drill plans. A well in Main Pass 61 was spud in April and is targeting the same sands hit in the Don Carlos well, which produced 1,250 BOPD. At a conference on May 22, the company said the Banshee well was complete and was being brought online. The Banshee is a dual completion well and, similar to the Black Widow recompletion, is a gas well that will be “swamped over to oil,” as production continues.

A development well was drilled at Ship Shoal 208 and flow testing is expected to begin within the month of June. The Ship Shoal 208, in addition to South Pass 78, are two fields formerly run by EPL and EXXI believes the company can reverse the region’s base decline without much capital.

Tables Set, Organic Growth Next

West Griffin, Chief Financial Officer of Energy XXI, went in-depth on the company’s outlook at a conference on May 14, 2014. “We’re no longer just drilling wildcat wells,” he said. “We’re shifting more and more into the development phase. And with that, becomes a little bit more of a lower risk environment. We’re very excited that this is going towards the development of shallower, cheaper opportunities.”

Schiller echoed Griffin’s comments at a conference on May 22. Exploration will be minimal, except for possibly one ultra-deep well, for the next 12 to 18 months. Possible projects in Malaysia have been terminated for the time being as EXXI works to strengthen its balance sheet and fully integrate EPL’s inventory into the pipeline.

EXXI’s debt-to-market cap is approximately 65% – above the company’s comfort ratio of 40% to 60%. However, Griffin says: “You’re going to see cash flow of these assets to drive that leverage down below 60%. We’ve done it before. We did it with Exxon ($1.01 billion acquisition in December 2010). It’s about the same amount of leverage. And we were very, very successful in driving that leverage down over 18 months to 24 months.”

Capital expenditures moving forward are not expected to exceed $800 million.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. A member of EnerCom, Inc. has a long-only position in EXXI.