Bolt-on acquisition extends Enterprise’s infrastructure into the Eagle Ford

Enterprise Product Partners (ticker: EPD) announced today that it agreed to purchase all member interest in EFS Midstream LLC from affiliates of Pioneer Natural Resources (ticker: PXD) and Reliance Industries (ticker: RIL) for $2.15 billion. The purchase price will be paid in two installments with the first payment of $1.15 billion due at closing and the remaining $1.0 billion paid no later than 12 months after the closing date, according to an EPD press release.

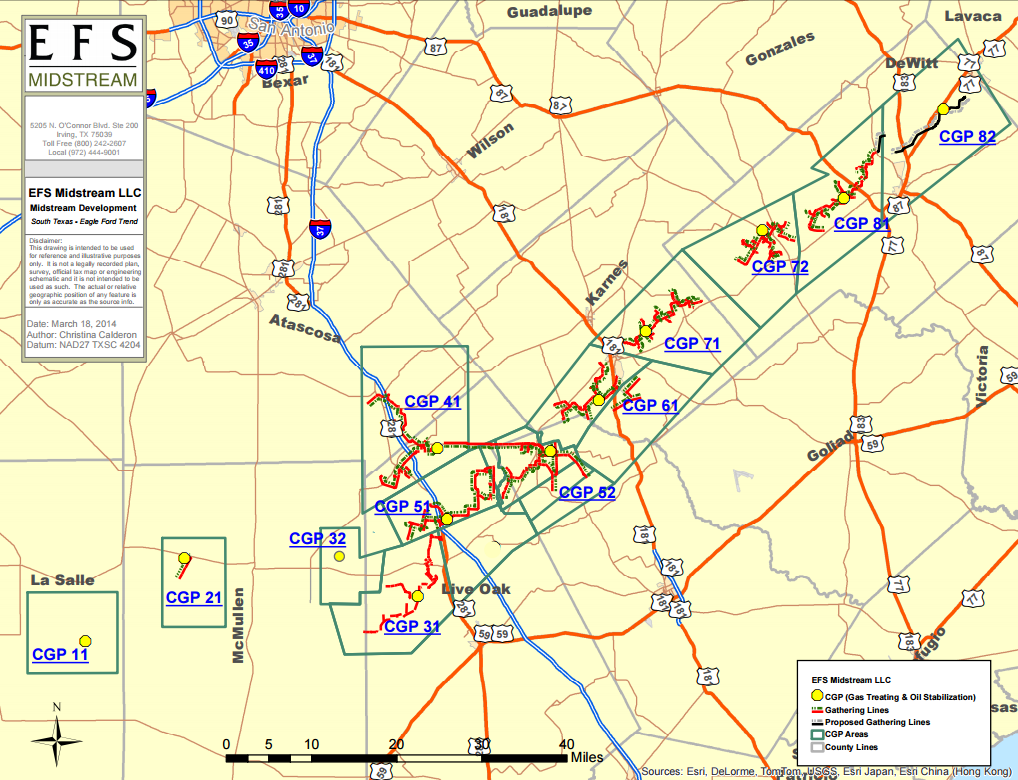

The EFS Midstream system includes approximately 460 miles of natural gas gathering pipelines, 10 central gathering plants, 780 MMcf/d of natural gas treating capacity and 119 MBOPD of condensate stabilization capacity in the Eagle Ford Shale. The transaction is expected to close in Q3’15.

Under the agreement, the sellers will continue to use the EFS Midstream system for 20 years, including a minimum volume requirement for the first seven years. EPD plans on spending $270 million throughout the next ten years to expand and improve the facilities in the region.

EFS Midstream Assets

Enterprise CEO Michael Creel said the bolt-on acquisition extends the company’s reach into the Eagle Ford, providing EPD with the ability to offer services to additional producers and increase volumes on its system. “The minimum volume commitments support annual revenue growth and cash flow assurance. We expect the transaction to be immediately accretive to distributable cash flow,” said Creel.

Pioneer was expecting the assets to generate more than $100 million in cash flow in 2015, with its 50.1% interest in mind. The E&P plans on spending the additional capital to ramp up its Eagle Ford operations, which will in turn contribute to the volume agreements with EPD.

Enterprise in 2015

Enterprise is the largest master limited partnership (MLP) in EnerCom’s MLP Weekly, with a market capitalization of $63 billion for the week ended May 29, 2015. The company’s debt to market cap ratio of 34% is well below the MLP Weekly group’s median of 54%, while its ROIC and ROA of 11.7% and 10.4%, respectively, are above the group median of 9.5% and 8.7%.

In the company’s first quarter report, EPD showed a 19% decrease in net income, but showed growth in some segments, including its petrochemical and refined products divisions. Enterprise also increased its dividend for the 43rd consecutive time to $0.375 per unit, a 5.6% increase from Q1’14.

Enterprise and the Export Market

Enterprise is one of only three companies currently allowed to export condensate, and its presence in South Texas provides the midstream giant with a prime position to send its product abroad. EPD’s Gulf Coast assets increased last year with the $6.0 billion merger with Oiltanking Partners, the world’s second largest storage provider. Noncrude exports from the United States have increased for 13 straight years but are still miniscule numbers compared to what the company might export if the crude oil export ban is lifted.

EPD management addressed the export ban in its Q1’15 conference call, with Jim Teague, Chief Operating Officer, leading the charge to lift the export ban. “There are only two countries in the world that are living under restrictions that prevent them from freely exporting crude, Iran and the U.S., and news reports suggest that soon there may be only one,” he said. “Ultimately, we believe that could undermine the positions of those industries that are prospering because of the bets they’re making on U.S. E&P. If U.S. E&P is the foundation of your success, then denying markets will ultimately undermine your foundation.”