Whiting Petroleum (ticker: WLL) has announced the acquisition of Kodiak Oil & Gas (ticker: KOG), making the company the largest producer in the prolific Bakken/Three Forks area in the Williston Basin.

COMBINED COMPANY

- 107,000 BOEPD (Q1 2014) Production

- 370 MMBOE Reserves

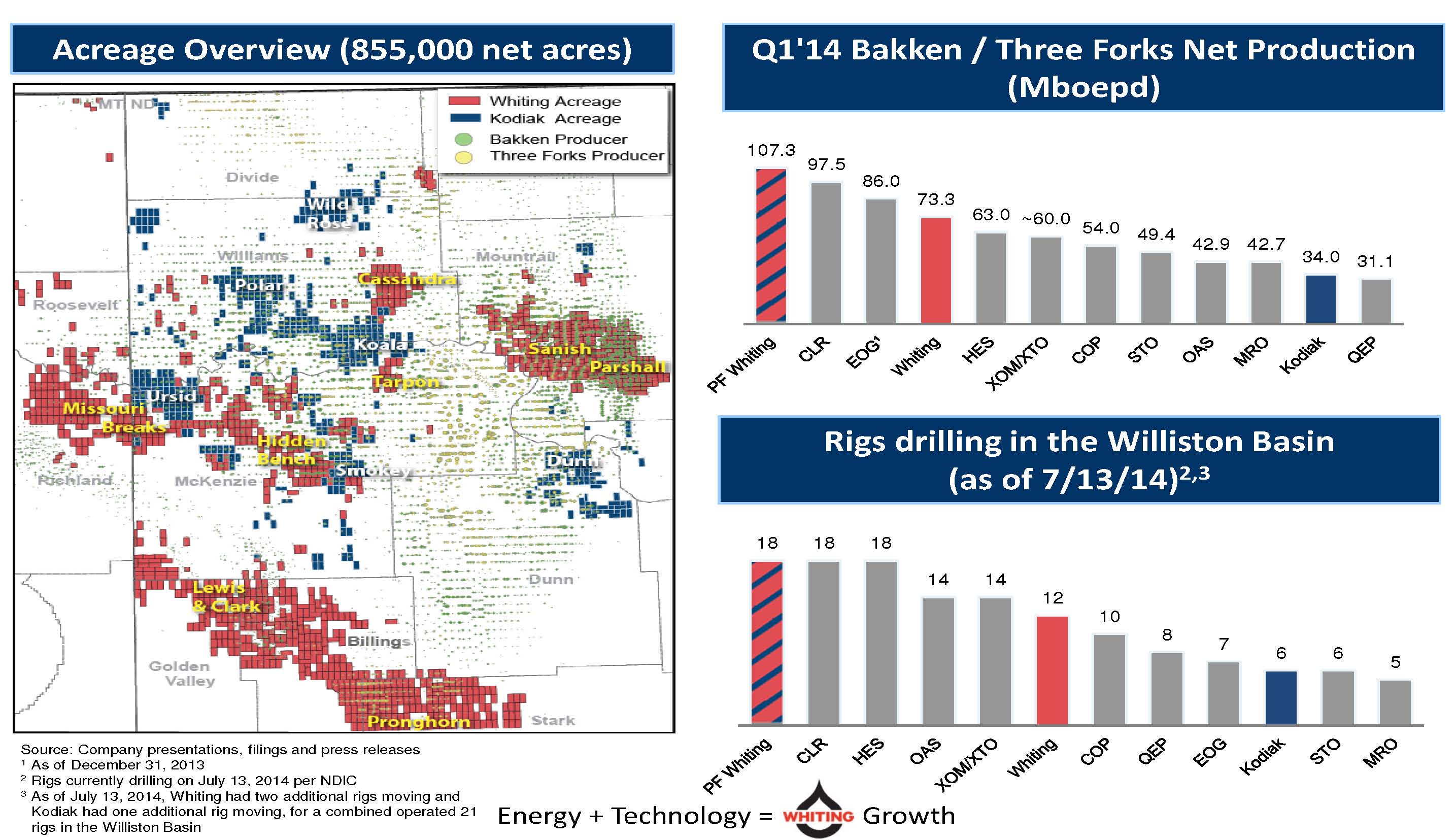

- 855,000 Net Bakken Acres (strongest acreage position in the Bakken)

- 3,460 Future Drilling Locations

- 21 Active Williston Rigs

- 1,200+ Employees

- Economies of Scale: $700,000 Expected Cost Savings per Completed Well

- Liquidity ($400 million cash)

- Access to Capital ($4.5 billion revolving credit facility)

- “All Oil, All the Time” – James Volker, Whiting Petroleum CEO

Whiting Petroleum announced the $6.0 billion acquisition of Kodiak Oil & Gas on July 13, 2014. The purchase price includes the assumption of KOG’s $2.2 billion in net debt and will commence as an all-stock transaction. The transaction is expected to close in Q4’14.

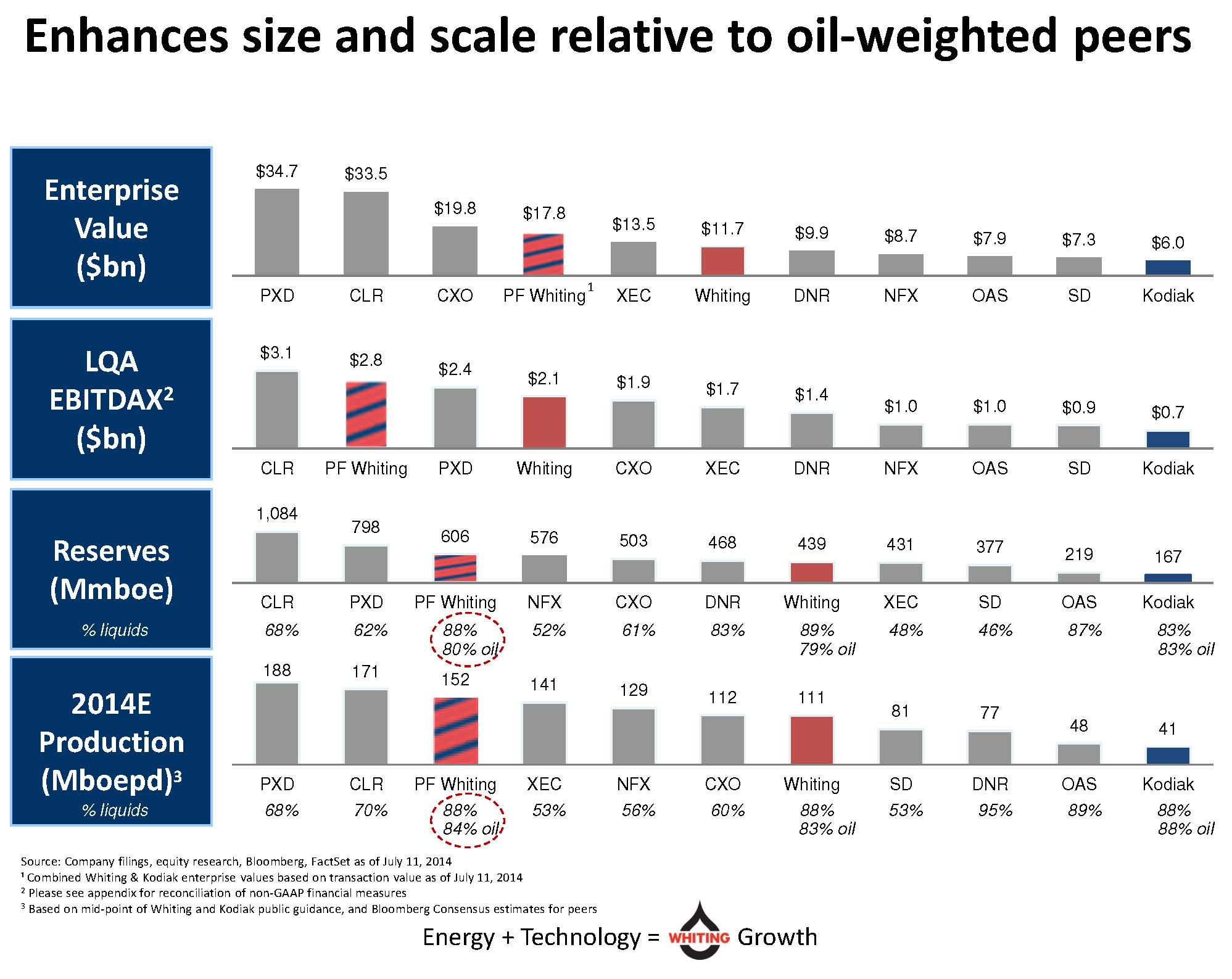

Pro forma for the acquisition, Whiting Petroleum is now the largest producer in the Bakken/Three Forks region. Combined production regarding Q1’14 results would be more than 107 MBOEPD. The company also holds a total of 3,460 net future drilling locations spanned across 855,000 net acres. Its updated reserves consists of roughly 370 MMBOE.

“We expect the combined entity to have an initial enterprise value of $17.8 billion,” said James Volker, Chairman, Chief Executive Officer and President of Whiting Petroleum in the release. “Total 2014 production of 152 thousand barrels of oil equivalent per day, and proved reserves of 606 million barrels of oil equivalent (80% oil), provides a leading platform for future oil-driven growth.”

Source: WLL/KOG July Presentation

Overall assets, including Whiting’s Redtail position in the DJ-Niobrara and other smaller pieces in the Gulf Coast, Mid-continent and Permian, equal total production of 134 MBOEPD in reference to Q1’14. Proved reserves are 606 MMBOE, with 88% liquids. The Bakken/Three Forks is expected to consist of 80% of all production.

Whiting’s New Makeup

The current senior management team of Whiting will continue to serve as the executive leadership for the new company, while two members of Kodiak’s management will assume positions on the board of directors. Shareholders for Kodiak will receive .177 of a WLL share in exchange for a KOG share,representing a 5.1% premium in regards to each company’s closing price on July 11, 2014. Consideration per share is $13.90. Once complete, WLL and KOG shareholders will own 71% and 29% of the company, respectively.

WLL increased its borrowing base for $4.5 billion with commitments totaling $3.5 billion – an amount capable of funding the company’s ongoing liquidity needs. Interestingly, the purchase is in line with an approach taken by investors. Whiting management said roughly 60% of its shareholders also have a stake in Kodiak Oil & Gas.

All Oil, All the Time

Volker established Whiting’s goal succintly in a conference call following the release. “The company will continue to be all oil, all the time,” he said.

Source: WLL/KOG July Presentation

The combined company had 18 rigs running in the region at the time of its acquisition announcement. The company expects to ramp up to 26 Williston-based rigs by Q4’15, which would be the most of any E&P in the area. Of the 26 rigs, 12 will run in KOG’s current area, which is nearly double its current count of seven. “Whiting’s plan of increasing operating rigs from 7 to 12 on our acreage was not something we felt comfortable doing on our own with our financial profile,” said Lynn Peterson, Chief Executive Officer of Kodiak Oil & Gas, in the call. “This increase in rig count will drive increased value for both sets of shareholders.”

Whiting management also expects cost savings of $0.7 million per well, with the realized effects forecasted to begin in January 2015. If the savings are reached, the average well costs will drop to $8.5 million per well from $9.2 million per well.

Whiting/Kodiak Metrics – EnerCom

Based on information from EnerCom’s E&P Weekly, which compromises financials from 86 E&P companies, Kodiak was among the best in three-year production replacement. Its percentage of 1009% was more than three times greater than the industry median of 314% and ranked seventh among all companies. On a comparison with 25 other mid-cap companies, Kodiak’s three-year production replacement ranked second. Its price to cash flow per share (P/CFPS) multiple of 5.0x was below the industry median of 5.6x, but EnerCom predicted the 2014 P/CFPS multiple to reach 7.7x prior to the acquisition.

Whiting has been efficient in managing its balance sheet, as evidenced by a debt to market cap of 28% before the acquisition. The percentage is below the overall industry median and mid-cap median, which are 31% and 38%, respectively. Volker said, “You’ll see a slight uptick in our leverage due to the assumption of the existing borrowing under Kodiak’s credit facility and existing notes. However, given the growth projected in the business, you can see it delevers very quickly.”

Source: WLL/KOG July Presentation

Similarly to KOG, WLL shares also appear to be undervalued. WLL currently trades at a 4.5x multiple to cash flow, but EnerCom predicted it to reach 6.7x without taking the acquisition into account.

Continental Resources (ticker: CLR) and Pioneer Natural Resources (ticker: PXD), the two companies singled out as WLL’s oil-weighted competitors, have current P/CFPS multiples of 8.8x and 13.5x, respectively, with the number forecasted by EnerCom to reach 11.2x and 12.7x.

Whiting’s Future

Whiting had forecasted 2014 growth of 17% to 19% in a press release in May. WLL’s oil focus and its ability to implement new techniques supported the company’s cash flow per share at a yearly compound growth rate of 26% since 2009. Kodiak, meanwhile, was forecasting volume growth of 40% at its midpoint in its Q1’14 earnings release.

Whiting management reminded analysts and investors that although the acquisition of KOG boosts its net Williston drilling location count by 158%, WLL has also increased the number organically.

“The growth we show here is not only what we get through our acquisition of Kodiak. It’s also due to the

success Whiting has had on a standalone basis year-to-date,” said Volker. Although he expects growth of 20% in 2015 and 2016, he expects the rate of increase to remain consistent. “We do think again that our objective would be in the 20%-plus growth, which can be achieved and can be achieved for a long period of time.”

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.

Analyst Commentary

Stifel Note (7.14.14)

Positive for KOG Despite Discount

While some KOG shareholders may be disappointed with an all-stock deal priced 2% below the previous trading day's close, we believe the transaction is positive for KOG, given the stock's recent outperformance (+14% since 5/1/14 vs our peer group average +3%). Moreover, KOG has long been viewed as a takeover candidate, and management has openly admitted to exploring a potential sale of the company. We doubt KOG management passed on more attractive opportunities than this one, which values the stock only 6% below its all-time high.

Bank of America Merrill Lynch (7.13.14)

With this proposed acquisition, Whiting will have consolidated its position as a premier player in the Bakken shale without having to pay a significant premium. WLL shares remain amongst the cheapest in the sector, and the proposed addition of Kodiak's acreage gives the company top tier acreage and inventory in the Bakken alongside an emerging 123,000 net acre position in the Redtail play in Colorado. We see little read-through to other names, as our view on M&A has been and continues to be that the drivers of any deal are most likely to be company-specific. Whiting remains our top pick in the SMID E&P space.

Wunderlich Securities – (7.14.14)

WLL is paying just $13.90 per share for KOG in an all-equity deal. You read that right, and frankly its the most interesting part in our view, as KOG's stock closed Friday over 2% higher than that figure and the premium as of now is just 5% above the 60 day average for KOG. In our view, this is a great/accretive price for WLL and its shareholders but for KOG and its shareholders it doesn't seem all that compelling. Granted it's an all equity deal so the upside isn't gone but none is realized today.

Great buy for WLL in our opinion and it supports our thesis on both names. Obviously given our ratings we like WLL and this deal should show that as we adjust our numbers, adding the high-growth assets of KOG. Honestly though the Street has believed KOG to be for sale for quite some times (years) it surprises us that the price it's finally taking is below the market's valuation of the company.

Either way, a job well done for KOG and its management. Overall the rise of KOG over the past few years has been fantastic and it has increased the value of its company tremendously alongside the Williston Basin as it became a large oil producer. Combining with WLL could allow investors to keep moving the value higher and given WLL's performance the last few years that end game looks very possible.

The boards have both approved the deal and it will now go to the shareholders. Based on the price we think WLL shareholders likely overwhelmingly approve the deal but wonder how well received the deal will be to KOG investors. Many investors of KOG have been in the stock for a potential transaction, and here it is, but given the price we wonder if KOG investors will be satisfied.