*This story was corrected from an earlier version to reflect Energy & Exploration Partners’ debt level

Low oil prices push 41 energy companies into bankruptcy

Saying that 2015 has been a difficult year for the oil and gas sector would be an understatement.

U.S. crude oil benchmark WTI averaged $91.23 per barrel in 2014, while in 2015 it has, to date, averaged $49.12. That’s a 46% decline, and it shows no signs of recovering soon. WTI today stands at $36.08, 34% lower than the year-ago price of $55.26. Future crude oil prices for December 2024 currently sit at just $54.96.

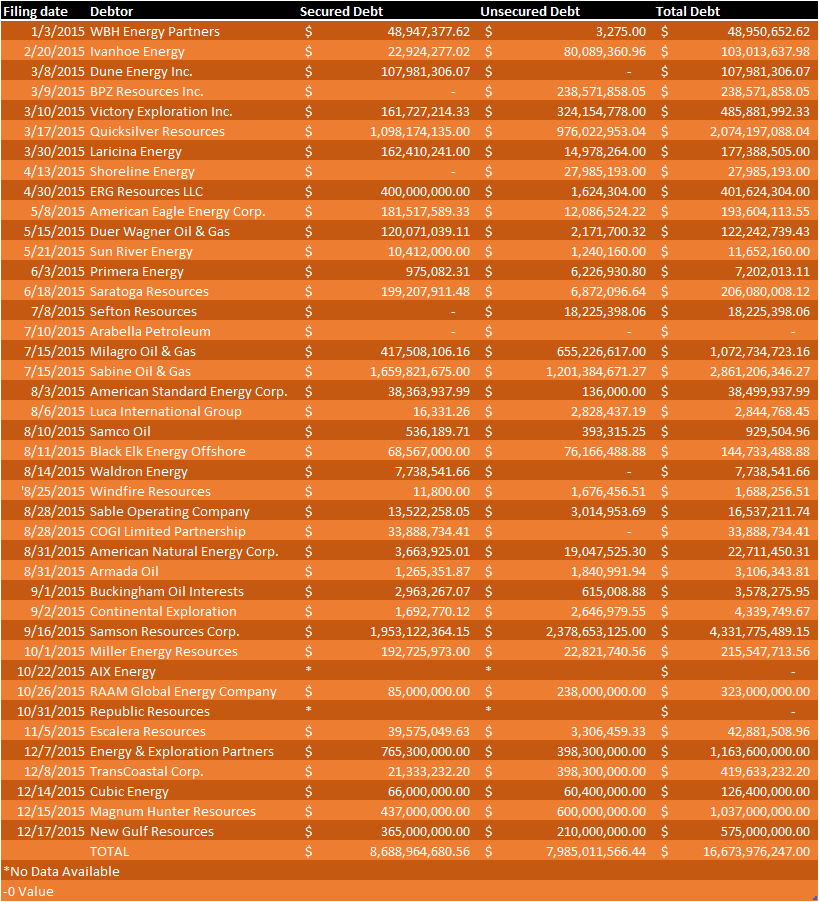

This sharp decline in prices has put the oil and gas industry in a difficult position. Many companies have adapted to the new reality of low oil prices, but that’s easier to accomplish for companies with right-sized balance sheets. Not all have been so fortunate. As of mid-December, 41 oil and gas companies filed for bankruptcy protection under Chapter 11 or Chapter 7 of the U.S. Bankruptcy Code with the court system. Their collective debt, both secured and unsecured, totals more than $16 billion dollars.

Once a company files for Chapter 11 protection with the court system, management continues to run the day-to-day business operations, but all significant business decisions must be approved by a bankruptcy court. Once a company files Chapter 11, one or more committees is appointed to represent the interests of creditors and stockholders in a process of working with the company to develop a plan of reorganizing to get it out of debt.

Creditors with secured debt, which is backed by collateral, are paid back first after the company files Chapter 11, with those holding unsecured debt paid next. Common equity stockholders are last in line. Although a company may emerge from bankruptcy as a viable entity, generally, the creditors and the bondholders become the new owners of the shares.

Instead of allowing a company to continuing operating, those in Chapter 7 bankruptcy are forced to sell off any un-exempt assets to pay creditors. A trustee is appointed, and they ensure that any assets that are secured are sold and that the proceeds are paid to the specific creditors.

Oil and gas debt from bankruptcies 52% secured

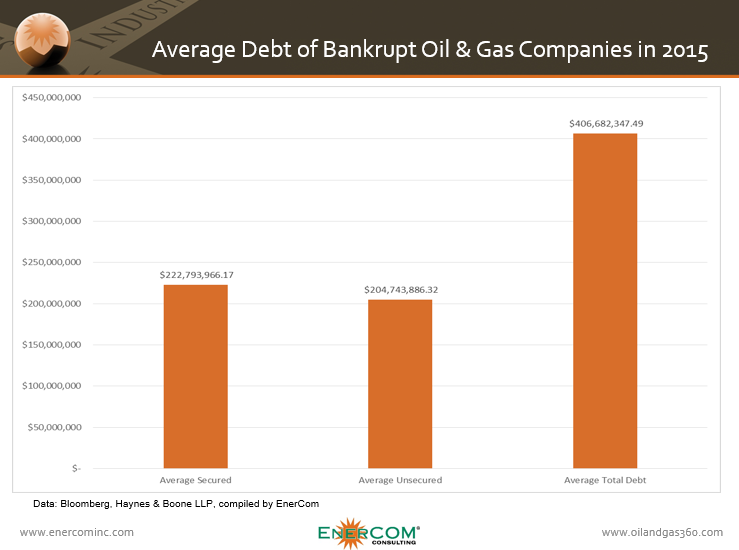

Debt in the oil and gas companies that filed for bankruptcy in 2015 was split very nearly down the middle of secured and unsecured debt. The 41 companies had a combined secured debt load of $8.7 billion, with another $8.0 billion in unsecured debt. The total debt of the companies was approximately $16.7 billion.

The average total level of debt for the companies that filed for bankruptcy in 2015 was $406.7 million dollars. The average secured debt was $222.8 million, while the average unsecured debt for the companies was $204.7 million.

The largest bankruptcy of any single E&P company happened on September 16, 2015. Samson Resources filed for Chapter 11 protection reporting total debt was $4.3 billion. Its bankruptcy made up roughly 30% of the total dollar value of oil and gas bankruptcy filings.

Samson entered bankruptcy with a pre-arranged plan to reduce its debt by swapping control to a group of investors who held the company’s $1 billion second-lien loan. Those lenders were also planning to buy $450 million in stock in the reorganized Samson. There has been no final plan announcement as of December 18.

Kohlberg Kravis Roberts & Co. LP purchased Samson for $7.2 billion in 2011. Phil Cook, Samson CFO, made known Samson’s thinking, and the industry’s for that matter, during bankruptcy court proceedings:

“Oil and gas companies across the United States and around the world are feeling the pressure from the downward spiral in commodity prices, and the fate of many of these companies is yet to be determined. Access to capital is the lifeblood of exploration and production companies. With increasing leverage because of a constant need for capital, together with the recent rising cost of capital in the industry, operating in the current environment has been—and likely will remain—challenging . . . . Some companies will attempt to wait out the current conditions, hoping for a rebound in commodity pricing and increased access to low-cost capital; others will succumb to market pressures and be forced to sell at depressed prices or otherwise permanently halt operations. Other companies will take a proactive approach and work to reshape their operations and balance sheet in a manner that will allow them to weather the macroeconomic environment in all circumstances.”

[Declaration of Philip Cook In Support of Chapter 11 Petitions and First Day Motions (Docket No. 2) at pg.1;In re Samson Resources Corp., Case No. 15-11934 (Bankr. D. Del. Sept. 17, 2015) (emphasis added).]

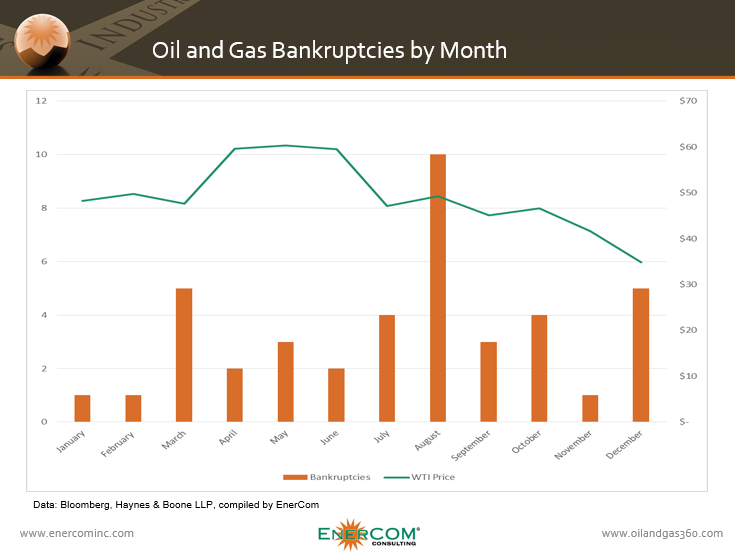

Black August

Bankruptcies in the oil and gas business happened every month this year, with seven companies filing for bankruptcy over the course of the first quarter, with WTI prices averaging $48.53. By far the darkest month for the industry this year in terms of bankruptcies, however, was August. With WTI closing out the month at $49.20, 10 companies filed for bankruptcy as the industry began to show signs of stress under the continued low oil price.

The Federal Reserve’s Red Flag

The Shared National Credits (SNC) exam, a Federal Reserve initiative to review and classify large syndicated loans, rated one in seven loans in the oil and gas industry over $20 million as “classified loans” – those with unpaid interest and principal outstanding that are in danger of defaulting.

The SNC report said: “Oil and gas commitments to the exploration and production sector and the services sector totaled $276.5 billion, or 7.1%, of the SNC portfolio. Classified commitments – a credit rated as substandard, doubtful, or loss – among oil and gas borrowers totaled $34.2 billion, or 15.0%, of total classified commitments, compared with $6.9 billion, or 3.6%, in 2014.“

Lower SEC price deck creating pressure

The amount of reserves companies have to borrow against have also been coming down as the SEC lowers its price deck for 2016. The dramatic decrease in oil prices since November of last year has pulled the SEC’s price deck down to about $50.13, based off the average of the price for WTI on the first day of every month this year, down 48% from the price deck used in 2015.

The lower price deck means companies have fewer reserves to borrow against, which saw many of them come out of their borrowing base redeterminations with less available credit from banks than they had before oil prices crashed. According to information from EnerCom Analytics, oil and gas companies saw their borrowing bases reduced by 11.7% on average during the most recent redetermination.

What’s coming next?

EnerCom’s database indicates that as of the week ended December 18, 2015, the average debt-to-EBITDA ratio of E&P companies was 2.6x, with a median of 2.9x. Those with the highest debt-to-EBITDA will like be the first to run into issues down the road.

With bank redeterminations lowering the amount available for most energy companies to borrow, and with several companies highly levered, it is likely that more bankruptcies could be in store in 2016. Options still remain for companies that file Chapter 11, however.

Samson Resources’ plan to hand equity in the restructured company to junior lenders, including large investment firms Silver Point Capital LP, Cerberus Capital Management LP and Anschutz Investment Co., in exchange for debt forgiveness will help keep the company operating. Those lenders have also agreed to recapitalize the company with as much as $485 million in new loans and to support a rights offering.

Other companies could follow in Samson’s footsteps, working to convince debt holders to forgive their indebtedness in exchange for equity, or seek new equity investors to take out the debt as a “get out of bankruptcy” card, according to EnerCom Analytics. A company’s ability to manage its bankruptcy will ultimately come down to their assets, says EnerCom. “The ultimate debt-for-equity truth will be in the rock.”

Some companies still in a strong position

Even as the oil and gas industry goes through a difficult downturn, some companies continue to prosper.

In fact, based on their most recent filings, several companies have managed to position themselves to make it through in good shape despite the lower price of oil. Companies that have kept a strong balance sheet and optimized operations and overhead look like they will be able to weather the storm of the current commodity environment and come out the other side positioned to take a leading role when a recovery begins.

Companies like Gulfport Energy Corp. (ticker: GPOR), Occidental Petroleum Corp. (ticker: OXY), PDC Energy (ticker: PDCE), Panhandle Oil and Gas (ticker: PHX) and Synergy Resources (ticker: SYRG) have all managed to maintain strong financial metrics despite today’s lower oil prices.

All the companies in that group have lower than the average 2.6x net debt-to-EBITDA ratio, which is the group average from EnerCom’s E&P Weekly, while still maintaining low G&A costs, and using their capital more efficiently than most of their peers.