Denver-based PDC Energy (ticker: PDCE) is an independent oil and natural gas company that operates in Colorado within the liquid-rich Wattenberg Field and the Appalachian Basin including the emerging liquid-rich Utica Shale play in Ohio and the Marcellus Shale in West Virginia.

PDC announced its total proved reserves for year-end 2013 were 266 MMBOE, an increase of 38% compared to 2012’s year-end reserves of 193 MMBOE. Approximately 54% of the company’s production was from liquids. The commodity makeup achieves the company goal of reaching at least 50% liquid production in order to better balance its portfolio between liquid and gas, as stated in its Q4’12 news release.

In addition, the company sold approximately 16 MMBOE worth of proved developed reserves in June 2013. If the divesture is excluded from year-end numbers, PDC’s proved reserves actually grew organically by 50%. PV-10 value for the company climbed to $2.7 billion, an increase of 59% compared to 2012’s value of $1.7 billion. Its year-end 2013 3P reserves rose to 854 MMBOE (56% liquids), a 45% increase from 2012’s total of 589 MMBOE.

The estimates were conducted by Ryder Scott Company, L.P., using NYMEX prices of $96.94 per barrel and $3.67 per million British Thermal Units.

PDC Continues Investment in Wattenberg

PDC management said much of the reserve increases were a result of downspacing in the Wattenberg, and the play’s proved reserves increased by 42%. PDC holds 98,000 net acres with 95% held by production, and is the third largest leaseholder and producer in the region. The project has now identified 623 proved undeveloped horizontal locations in the play, with 543 in the Niobrara and 80 in the Codell formation. Other increases resulted from initial reserve bookings in the Utica Shale. Due to its attention on oil, PDC management said it will not be drilling on any of its Marcellus Shale acreage in 2014.

In terms of 3P reserves, the Wattenberg downspacing project has revealed roughly 22 wells per section, increasing the 3P well inventory to more than 2,800 gross locations. Overall, the company has now identified more than 3,600 gross 3P locations.

In 2014, PDC plans on running 16 wells per 640-acre section. The company will progress on its Wattenberg acreage by adding a fifth rig in Q2’14. The region’s fourth rig was placed online in December 2013. Management said it plans on conducting a 25 well per section downspacing test with an outside operator in the upcoming year. A 16 well test in November 2013 on its Waste Management section exceeded company expectations with total production of 7.6 MBOEPD (88% crude oil).

The Utica, meanwhile, will receive its second rig in 2H’14. PDC management said 11 wells were drilled in 2013 and the new rig will assist in the planned drilling of 18 wells in 2014.

PDC Energy’s Shift to Oil

The ongoing horizontal program is being utilized to meet PDC’s shift from gas to liquids production. The company had 113 producing horizontals according to its most recent presentation on January 24, 2014, and spud 119 (70 operated) in 2013. The company plans on spudding 133 total operated horizontals in 2014, with 115 in the Wattenberg. Its 2014 capital budget of $647 is still largely dedicated to the ongoing development of the play, and an estimated 89% will account for its expenditures.

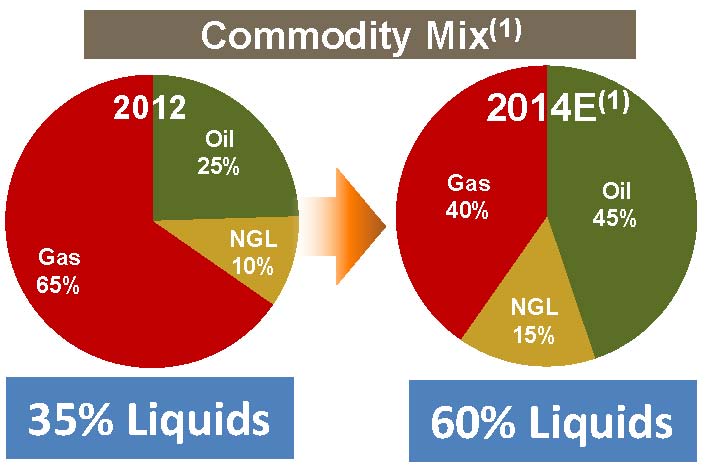

As indicated by PDC’s chart on the right, liquids production in terms of commodity mix has grown by more than 70% since 2012. Production dropped to 7.3 MMBOE in 2013 from 8.9 MMBOE in 2012 as a result of the shift to a more oil-oriented approach. Despite the drop in daily production as a result of the change, PDC expects its downspacing and horizontal program to compensate for the drop. Initial guidance for the upcoming year expects production to reach 9.5 MMBOE to 10 MMBOE, with oil being the driver going forward.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. As of the report date, neither EnerCom nor any of its employees has a financial interest in any equity or debt of any company mentioned in this report.

Analyst Commentary

Bank of America Merrill Lynch Note – (1.28.14)

4Q13 production tops expectations

PDCE released its 2013 year end reserves this morning, which saw a YoY increase from continuing operations of 50% to 266MMBoe and PV-10 rise to $2.7bn from $1.7bn, based on $96.94/bbl oil and $3.67/MMBtu gas. However, in our opinion, the key takeaway from today's release was a 2013 FY production estimate of 7.3mmboe, which implies 4Q13 average daily production of 24.2mboe/d, above both our estimate (22.7mboe/d) and consensus (23.3mboe/d). This is a strong result given the anticipated impact of severe weather in Colorado and a shut-down of DCP's Eaton plan in late December.

2013 reserves show increase in PUD % and locations

While total proved reserves from continuing operations at YE 2013 increased ~50% yoy, this was driven largely by an increase in PUD reserves which grew ~75% yoy and now make up 72% of total reserves compared to 62% at YE12. Overall reserve growth was driven by additions from Wattenberg downspacing, increased per well reserves in the horizontal Niobrara and Codell, and initial reserve bookings in the Utica, where PDC booked 14.4MMBoe. The percentage of liquids also increased to 54% compared to a year ago (~52%) while PDC reported an increase of ~800 locations in its 3P inventory in the Wattenberg, based on tighter assumed spacing of 22-wells per section compared to the prior assumption of 16-wells per section. Note that at this point PDC has yet to test beyond 16 wells.

Increasing 4Q estimates, focus remains on Wattenberg

We increase our 4Q13 production and EPS estimates to 24.2mboe/d and $0.24/sh (vs. 22.7mboe/d and $0.21 prior). Our LT estimates and NAV based PO of $73 remain unchanged as we do not attribute any value to the as yet untested 22-well per section Wattenberg inventory (i.e., ~800 locations). As noted before, we believe that near term risks for PDCE have now largely played out, allowing focus to shift back to the company's core Wattenberg position. That said, our cautious stance on the sector given near-term oil price risk leaves us Neutral.

Johnson Rice & Company Note – (1.28.14)

This morning, PDCE announced FY:13 production of 7.3 mmboe (in-line with guidance of 7.0-7.5 mmboe) above consensus' and our 7.1 mmboe. YE:13 proved reserves were also given at 266 mmboe (54% liquids; YE:13 was 193 mmboe and 48% liquids), a strong increase considering the company's net divestiture of 15.0 mmboe of reserves. PDCE's internal 3P reserves moved from 589 mmboe to 854 mmboe, the primary driver of which was the Wattenberg, where gross horizontal locations was increased from 2,000 to 2,800.

The company announced FY:13 production of 7.3 mmboe, coming in above consensus' and our 7.1 mmboe and at the midpoint of guidance of 7.0-7.5 mmboe. We would expect the street's 4Q:13 CFPS estimates to move upward (we moved from $1.72 to $2.01), however we would note that our FY:14 estimate remains flat at 26.7 mboe/d (in-line with company guidance) but on a more front loaded base from the larger than expected 4Q:13. Consensus' 27.2 mboe/d was previously above FY:14 guidance and will likely remain there, however you should not expect an increase beyond the magnitude of the 4Q:13 beat (~2 mboe/d).

We are adjusting our 4Q:13 production and CFPS estimates from 22.8 mboe/d and $1.72 to 24.7 mboe/d and $2.01. FY:14 moves from 26.7 mboe/d and $8.19 to 26.7 mboe/d and $9.21.

SunTrust Robinson Humphrey Note – (1.28.14)

Big Reserve Growth, Nice Production Beat and Encouraging 3P Report

What's incremental. PDC announced a strong reserve report that despite some caveats was quite impressive. Additionally, the 3P (proved, probable and possible) estimate suggests potential upside to our Wattenberg resource estimates. Finally, the company beat 4Q production estimates handily. We see the announcement as encouraging and expect outperformance today.

Strong reserve and production growth. PDC Energy announced reserves grew 38% y/y to 266 Mmboe (54% liquids, 28% developed). Reserve replacement was very impressive at 1,320% and the company reported 7.3 Mmboe in 2013 production versus the 7.2 Mmboe we and the Street expected. Before-tax PV-10 rose from $1.7 billion to $2.7 billion. Interestingly, the company booked 14.4 Mmboe from the Utica.

Some caveats. We see the report as quite strong, though proved developed reserves as a portion of the total have come down from 46% in 2011 and 42% in 2012 to only 28% in 2013. Also, we did not see a capital spending figure provided. That said, the 2013 production beat implies ~5% upside to 4Q production.

3P report encouraging for potential spacing. PDC's own internal estimate of 3P reserves increased ~45% to 854 Mmboe (56% liquids). Interestingly, the company modeled its 3P estimate on 22 total wells per section in the DJ Basin versus the 16 total it successfully tested with the Waste Management pad. This represents potential upside to our resource estimates, which are based on 16 wells per section. We will likely wait for a successful proof of concept before making any potential changes.