An OAG360® Exclusive: Interview with EIA Administrator Adam Sieminski

The United States Energy Information Administration (EIA) is the principal agency of the U.S. Federal Statistical System responsible for collecting, analyzing and disseminating energy information to promote sound policymaking and market efficiency on a national level. The EIA conducts a comprehensive data collection program that covers the full spectrum of energy sources, end uses, and energy flows; generates short- and long-term domestic and international energy projections; and performs informative energy analyses.

Adam Sieminski

Administrator of the EIA

At the helm of the Administration is Adam Sieminski, an energy economist veteran with roughly four decades of experience under his belt. Prior to being sworn in as the EIA’s eighth Administrator in 2012, Mr. Sieminski forecasted market trends for Deutsche Bank from 1998 to 2012, being named the Bank’s chief energy economist in 2005. Other accolades include acting as a senior adviser to the Energy and National Security Program at the Center for Strategic and International Studies, in addition to being the former president of both the U.S. Association for Energy Economics and the National Association of Petroleum Investment Analysts.

Oil & Gas 360® spoke with Mr. Sieminski from his office in Washington, D.C. on the evolving oil and gas industry in this installment of TOP MINDS IN THE BUSINESS.

Oil & Gas 360®: Thank you for tuning into Oil & Gas 360, my name is Derek Staudt. It’s my pleasure to be joined today by Mr. Adam Sieminski, he is the Administrator of the Energy Information Administration. Adam, thanks for joining us today.

EIA ADMINISTRATOR ADAM SIEMINSKI: Happy to be with you.

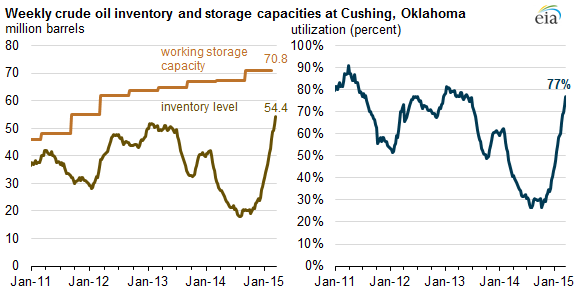

OAG360: So let’s start by looking at storage inventory levels. Cushing, Oklahoma, is nearing its maximum capacity. Whose storage is in these storage tanks? How much is from the U.S. and how much is from Canada?

Source: EIA’s “Today in Energy” for 3/25/15

Cushing inventory topped out at 62.2 MMBO and 88% capacity on 4/17/15

SIEMINSKI: Well, I don’t think we’re actually tracking the origin of the oil that’s in the storage tanks. We track the volume and so I’m not sure I can answer that question. What we do know is that in Cushing, this is the third week with crude stocks having come down somewhat, which kind of fits in with what EIA has been saying for some time now. We thought oil prices would firm up a bit and the concerns that Cushing would completely fill up and lead to a collapse in oil prices was somewhat overdone, from the standpoint of analysts.

Our view has always been that spreads would change which would then incentivize transportation away from Cushing towards other storage areas like the Gulf Coast for example.

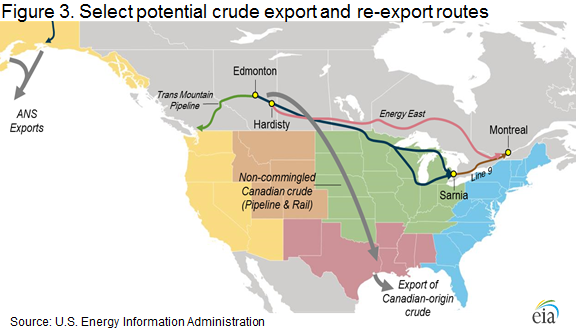

OAG360: Do the Canadians have a competitive advantage when they move crude through the US? Is it easier for them to refine it and export it as opposed to the U.S. producers?

SIEMINSKI: I’m going to presume that the Canadians have to pay for transportation in the same way that other users would to gain access to the pipeline network, so I don’t know what the competitive advantage would be in Canada.

There have been significant obstacles to getting new pipelines built in Canada to move Alberta crude oil to either the West Coast of Canada or even the East Coast.

There have been significant obstacles to getting new pipelines built in Canada to move Alberta crude oil to either the West Coast of Canada or even the East Coast.

West Coast proposals have run into what the Canadians refer to as the ‘First Nations.’ Opposition of getting pipelines and port facilities cited is basically difficult almost anywhere because the public doesn’t seem to like any kind of big construction projects in their back yard, and so that has been an issue in Canada as well as in the United States.

There have been reports that some Canadian oil has come through U.S. pipeline systems kind of in Bond, and there have been some exports from the Gulf Coast of the U.S. of Canadian crude oil. I suspect that the extent of that would probably be somewhat limited by the fact that the appetite in the Gulf Coast for heavy sour crudes from Canada is probably pretty strong and, as a consequence, Canadian crudes would most likely be used [by refineries] in the Gulf Coast.

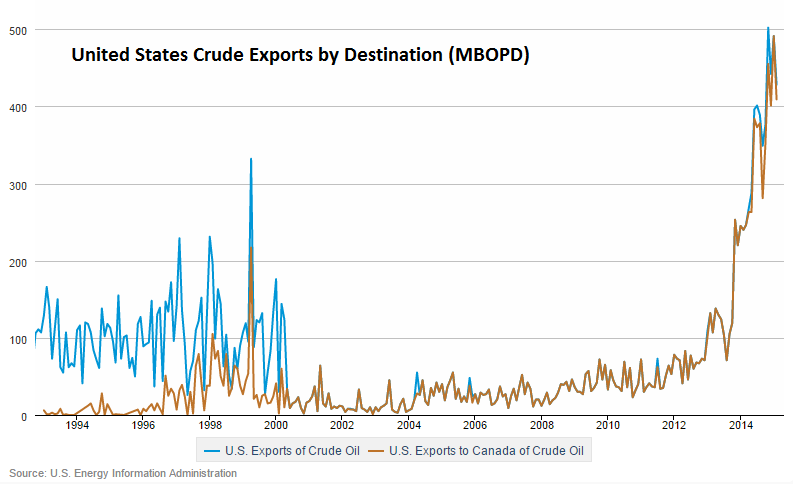

We do know that as part of the crude oil export rules, which are under the auspices of the Commerce Department – not the Energy Department where the EIA is – that the U.S. oil can be exported to Canada as long as the oil is used and refined in Canada. The EIA has been tracking that, and there have been increasing exports from the Gulf Coast of the U.S. up to eastern Canada to be refined there.

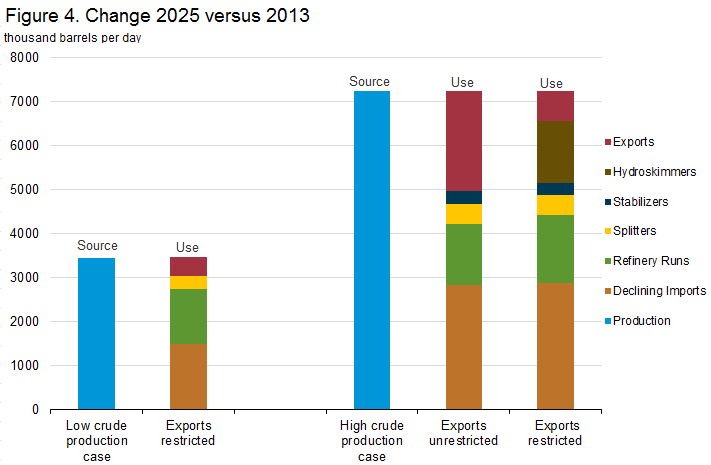

OAG360: What would happen on a global sphere if the crude oil export ban is lifted here in the United States?

SIEMINSKI: Well the EIA has been doing a series of reports on crude oil exports. We were asked to do that by a number of committee members in the U.S. Senate and in the House. Our first report was a year ago in May of 2014 and that was a forecast of crude oil production by type, that is, by A.P.I. gravity. That’s important because the increasing level of light sweet crude oil production does have some constraints at the refinery level in terms of how much light sweet crude oil can be processed by U.S. refineries.

So we did that in May and in July we had a summary of a number of other studies that were being worked on by other people. We did workshops in September and October on condensates and how condensates were being defined and issues associated with gasoline price setting in the U.S.

Source: EIA Study

Exports and the Effect on US Refining

We actually published in October of 2014 a kind of a combination of two studies: How do gasoline prices in the U.S. get set and what the relationship was between product prices in the U.S. and product prices overseas.

Let me just very quickly summarize those findings. Certainly looking back in the historical data, gasoline prices in the U.S. are tied to Brent Crude Oil benchmarks more so than they reflect changes in West Texas Intermediate prices. Similarly, product prices in various markets in the U.S. seem to be more tied to global markets, so product prices in New York and the Gulf Coast, for example, are more tied to Rotterdam then they are to each other.

The same goes for the West Coast, where those product prices are more tied to Singapore markets than they are to markets in the US. The conclusion a lot of people have come to, and EIA would not argue with, is that if the crude export ban were to be loosened it would most likely NOT result in an increase in gasoline prices in the United States. The lifting could lead to incremental volumes of crude oil on the global markets could very well result in lower crude oil prices globally which would then be reflected in lower gasoline and other product prices in the United States.

OAG360: Some analysts have been saying that U.S. shale developers have created a free market for oil for the first time. Do you agree with that assessment, I mean is there really a free market to be had?

Source: EIA Drilling Productivity Report – May 2015

SIEMINSKI: I would say that there has obviously been a role for OPEC, for example, in the global oil markets for a long time. We have seen in the past occasions where OPEC increases or decreases in production and policy announcements can change the pricing structure for oil on a global basis. I think that, in general, most energy economists believe product prices and crude oil prices tend to get set in the marketplace that it’s fairly competitive that in a larger sense that it’s a balancing of supply and demand that generally tends to set prices.This collapse in prices from, as you know, from over $100 to down into the $50 to $60 range that we had here recently, has precedence in my career in this area which started in the early 1970’s. This is the (count ‘em!) sixth time that oil prices have come down substantially.

Generally speaking, it tends to be market developments that move prices around. A lot of times the downward movement in prices have been associated with slowdowns in the global economy and demand, and in many circumstances price increases have occurred when there have been geopolitical events that have taken oil supply off the market. I can remember one instance in 2004 when prices really started climbing that was attributed to the rapidly rising consumption of crude oil in China. That led to need for markets to rebalance supply and demand because of the unexpected strong growth of demand in China. So geopolitical events play a role, the global economy plays a role, lots of moving pieces get involved but I would say that oil tend to be pretty freely traded and it’s those economic and trade relationships that really count the most.

Source: EIA Drilling Productivity Report – May 2015

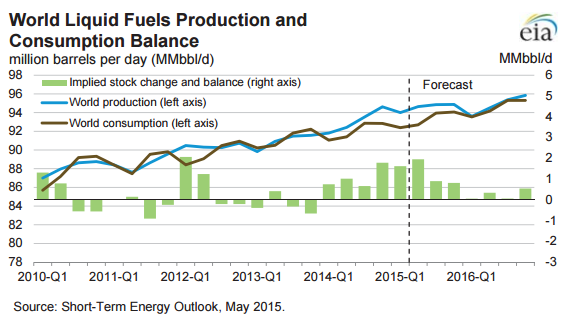

OAG360: If global production right now is, say, about 92 MMBOPD and consumption is about 93 MMBOPD, do we really have too much oil on the market or is this just overreaction?

SIEMINSKI: Well EIA’s numbers, I’m not sure where you are you’re getting your data from and there’s obviously lots of different analysts who have forecasts for supply and demand globally, including the International Energy Agency, the OPEC Secretary General publishes numbers, along with lots of oil analytical firms around the world.

But the EIA publishes our numbers every month in the Short Term Energy Outlook and for 2015 we’re assuming that supply is a little over 94 MMBOPD and demand is a little over 93 MMBOPD. So we’ve got more supply than we have demand and that has inventories building and typically when inventories are building you tend to have somewhat weaker pricing structures.

We see that is starting to correct as you get out into 2016 when we expect that the effects of lower oil prices will result in slower production. In a sense, that is already happening. Lower prices also tend to encourage demand and so a combination of lower supply and more demand suggests that by 2016 markets are back in balance, more of the inventory overhang is being drawn, and that should give us prices that average closer to $70 rather than the $60 price average for Brent crude oil that we’re expecting this year.

OAG360: Mentioning the IEA (International Energy Agency), they said in a May report that U.S. Shale production has blinked and the price war is just beginning. What’s your take on that assessment?

Source: EIA Drilling Productivity Report – May 2015

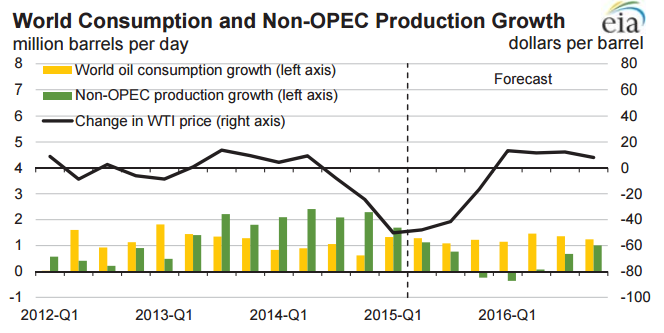

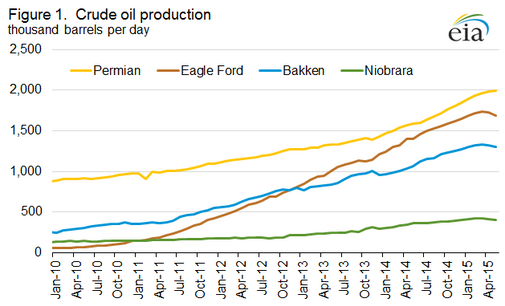

SIEMINSKI: The EIA has a document that we publish every month called the Drilling Productivity Report (link to report). If you trace the report back to the last two years, that growth in oil shale production is largely coming from four areas sort of in the central part of the U.S. and include the Eagle Ford, Permian Basin, Niobrara and Bakken formations. From those formations, we were having monthly change during 2012, 2013 into a good part of 2014, that was averaging 2.0% to 2.5% monthly gains, and that’s huge.

Oil production growth in the U.S. was up almost a 1.5 MMBOPD in 2014, and world oil demand was only growing about 1.0 MMBOPD total. So the U.S. alone was well exceeding that growth in demand, and you know with any kind of production coming from other countries around the world, whether it was in OPEC or outside of OPEC, that there were going to be balancing problems.

The Drilling Productivity Report now says that the growth from these four U.S. areas has fairly dramatically slowed. We might actually have, over the last three months, averaged a (-1%) month over a month growth figure. That’s shrinkage rather than growth, and that is exactly what we’ve been expecting – that the lower prices would lead to lower capital investment and lower drilling. We’ve seen the rig count come down and despite the likelihood of gains in productivity it’s being offset by these declines and that’s how the markets, in a sense, rebalance. Conventional oil is probably also going to be hit and there will probably be a little bit less stripper well production in the US.

Source: EIA Drilling Productivity Report – April 2015

This is a worldwide phenomenon. It’s not just that prices are lower in the United States, they’re lower everywhere in the world. A number of countries (Venezuela, for example) are going to struggle to maintain production and that’s going to lead to lower overall growth in oil production. But the lower prices will encourage demand and we’ve seen revisions recently upward in gasoline demand estimates in the EIA’s Short Term Energy Outlook. So, net result: markets start to balance. But nobody, not even the EIA with all the resources, analysts and data at our command, nobody exactly knows what the right balancing number is for oil.

I do think it’s fair to say that we had a three year experiment with $100 oil and we know that generated too much supply and not enough demand. We had prices drop below $50 and the reaction in the marketplace, combined with growth in the shale oil regions in the U.S. essentially stopping, is that the price might actually be a little bit too low. That’s one of the reasons why our forecasts for this year and next year are in the $60 to $70 range.

OAG360: The EIA was recently given approval by the White House to launch its own mandatory monthly survey of production; how does that differ from what you’ve done before and how will this impact your future reports?

Source: EIA 914 Expansion Proposal

Presentation by Mr. Sieminski conducted on 7/1/14

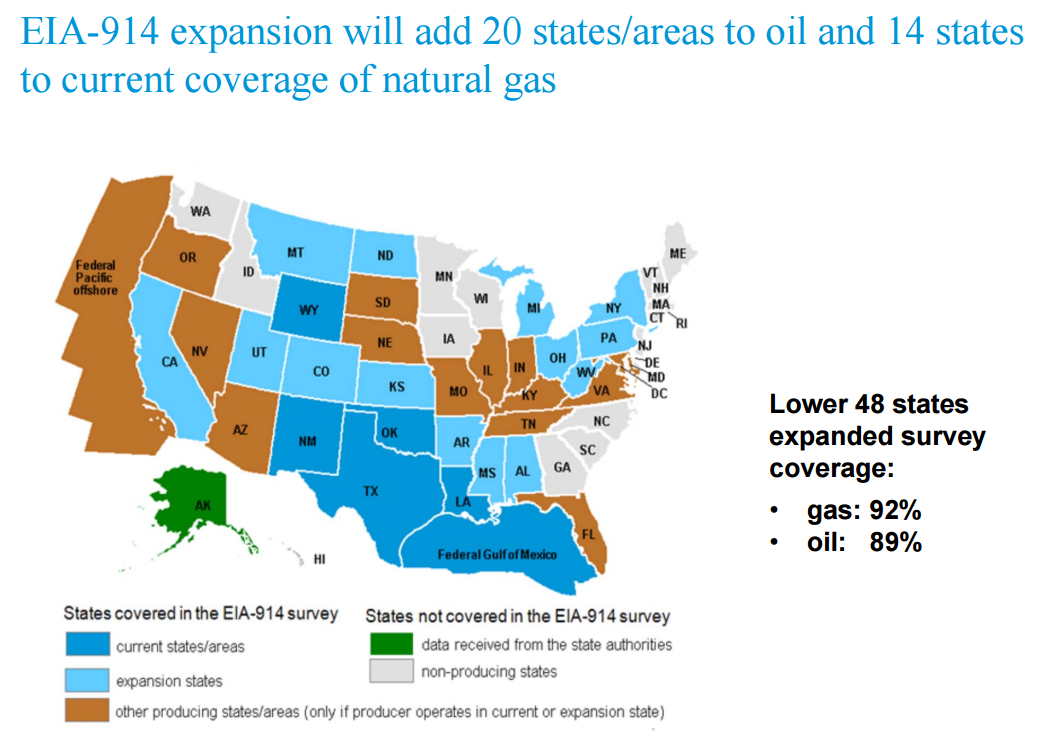

SIEMINSKI: About a decade ago, the EIA initiated a monthly survey of natural gas production (called the 914). It’s a sample of operators and it was across five states in the Gulf of Mexico. We realized several years ago that we were missing a number of very important natural gas producing states, including Pennsylvania, in this direct operator survey. We also felt that it was important, given the rapid growth that was taking place in these oil shale regions, that EIA had a direct survey sample of production on the oil side.

We also go back to this issue of how much light oil vs. heavy oil and the ability of refiners to handle it, and we wanted to know what production was by A.P.I. gravity.

So we began working a year and a half ago with the Office of Management and Budget and others to receive the permission that EIA needs to initiate new surveys. We now have that and we started to collect data on a preliminary basis. We’ll probably have some data to report on natural gas later this summer and by early fall we should be able to publish the oil data. It’s going to cover 15 states rather than five, and it will cover oil and oil by gravity as well as natural gas.

It’ll be a monthly sample of operators in these key oil and gas producing states so we will know a lot more on a more timely basis, on what’s going on with the oil and gas production figures. All along, we have made estimates of weekly oil and gas production but those estimates are not as good as actual data collections and so we’re going to improve in that area.

OAG360: How will that be complementary to the export studies the E.I.A. is currently working on?

Source: EIA’s “Today in Energy” 6/6/14

Sources of Light Sweet Crude

SIEMINSKI: Well, the export studies what we’re doing are related to the crude oil export issue and we will have really good data on how much light tight oil production is coming from these new oil shale fields. When we combine that with our data on refining capacity and utilization figures that will help answer the question of whether or not bottlenecks and refining capacity will lead to lower prices or shut-ins of domestic crude oil.

OAG360: Just one last question: so you’ve researched the energy industry for decades in several different capacities, if you had a chance to take the helm of your own energy company, what kind would you want to manage? Whether it be E&P, refining, coal, renewables, power generation – any of those stand out to you more than the others?

SIEMINSKI: Well, you know, I’ve got my hands full just running the Energy Information Administration. I’ve committed to the president that I’m going to stay through his term so I’ve got a couple more years’ worth of work to do here at the EIA and we aren’t done yet.

We have some of our program objectives and there are a few more surveys that we’d love to get out.

We’re looking at things like hourly data on electricity generation and although that is not directly an oil issue it certainly ties back into other fuels used in electricity generation like natural gas, coal, renewables and nuclear.

It will be, as far as I know, the first time that any federal statistical agency has collected hourly data on anything, so I’m pretty excited by that and I’ll worry more about what I’m going to do after I leave EIA when I get closer to making that decision or have it made for me by the President since I serve at his discretion.

OAG360: Alright, very good Adam. I really appreciate the time. It was a pleasure.

SIEMINSKI: Thank you very much.

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.