Does the term “bearish” even begin to describe commodity prices anymore?

Oil prices are generating most of the headlines, but natural gas has it just as tough: spot prices for Henry Hub are trading at 16-year lows. The story remains the same, as the supply/demand imbalance remains tilted towards the former with headwinds applying additional downward pressure. The tightened margins are translating to dwindling company balance sheets, similar to the difficulties experienced by OPEC members dependent on oil revenue to fuel their social programs.

But there is no OPEC with natural gas. There is no incentive to take drastic measures intended to squeeze competition off the market. But still, companies continue to operate and add product to a market that already has more gas than it knows what to do with. It begs a simple but loaded question… why are you drilling?

The Natural Gas Headquarters

The Natural Gas Headquarters

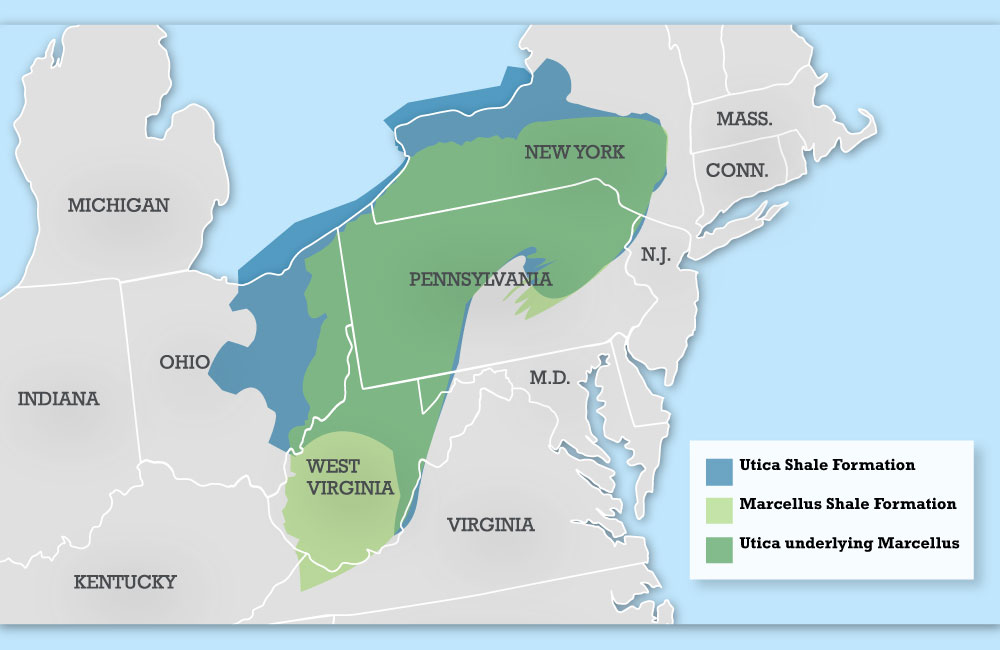

We wouldn’t be in this situation without the development of the Marcellus Shale, so we’ll focus our attention on the calling card of the Appalachia. The region’s production has increased eightfold compared to its 2010 output, and volumes have remained relatively steady even though its regional rig count has dropped by 50% in the past year.

The price of natural gas has fallen by more than 50% in the midst of that five year production boom, and now the producers responsible for the surge are watching their revenues shrink even though they’re churning out volumes at a near-record pace.

Profits when gas is above $4.00 is one thing. Profits when gas is at $1.80 (as it was in mid-December) is a whole different animal. In fact, many oil companies are not returning a profit at all, and have entered what many industry analysts are labeling “survival mode.” But how are companies faring in the Marcellus?

A Game of Addition (or Subtraction)

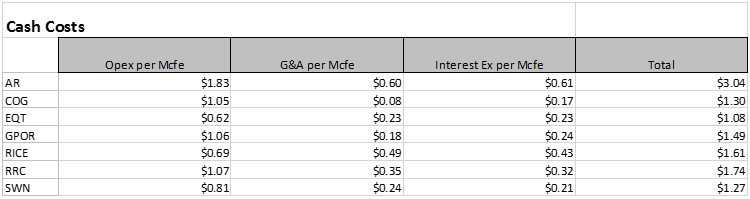

As you know, there’s more that goes into simply drilling a well. It costs cold hard cash to find and operate the well, and it costs more to pay the people and banks that are providing the manpower and the cash to run the ship. As part of our study, we’ll look at seven Marcellus companies who are among the best.

Comparatively, we’ll look at the four chief costs involved with balancing margins: operating, general and administrative, interest, and finding and development. There is certainly no questioning the resource potential of the Marcellus (per-well EURs on the seven listed companies are as high as 19 Bcfe), but making them economic in such a constrained environment is something else.

A unit per unit breakdown is listed below, based on information from Q3’15 quarterly reports and data compiled by EnerCom Analytics.

Excluding the realized value of hedges, producers are placed in a very tight spot. Antero Resources, for example, pays more in operating expenses alone than it generates from a sale of the product. Interest expenses also cut sharply into sale revenues, with the seven companies averaging a cost of about $0.32/Mcfe for the sole purpose of servicing its debt. That equates to nearly 18% of the sales price if the product were to be sold on the Henry Hub benchmark.

Excluding the realized value of hedges, producers are placed in a very tight spot. Antero Resources, for example, pays more in operating expenses alone than it generates from a sale of the product. Interest expenses also cut sharply into sale revenues, with the seven companies averaging a cost of about $0.32/Mcfe for the sole purpose of servicing its debt. That equates to nearly 18% of the sales price if the product were to be sold on the Henry Hub benchmark.

The above, by the way, only take into account the costs of operating the well. The finding and development costs add a fourth element to the scheme, with the results below.

F&D Estimates Based on Well Costs and EUR, Figures Derived from Corporate Presentations

AR $0.55

COG $0.43

EQT $0.46

GPOR $0.51

RICE $0.63

RRC $0.35

SWN $0.61

Factoring in the finding and development costs, we’re left with a table that looks like this:

| Cash and F&D Costs/Mcfe | |

| EQT | $1.54 |

| COG | $1.73 |

| SWN | $1.88 |

| GPOR | $2.00 |

| RRC | $2.09 |

| RICE | $2.23 |

| AR | $3.59 |

Considering a $1.80 Henry Hub price, only two out of the seven marquee Marcellus producers are returning a profit before considering any adjustments for a hedge book, pipeline contracts or any uplift from liquids prices which are also strained.

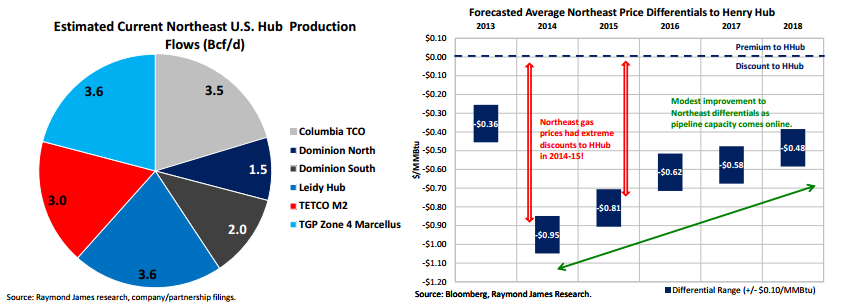

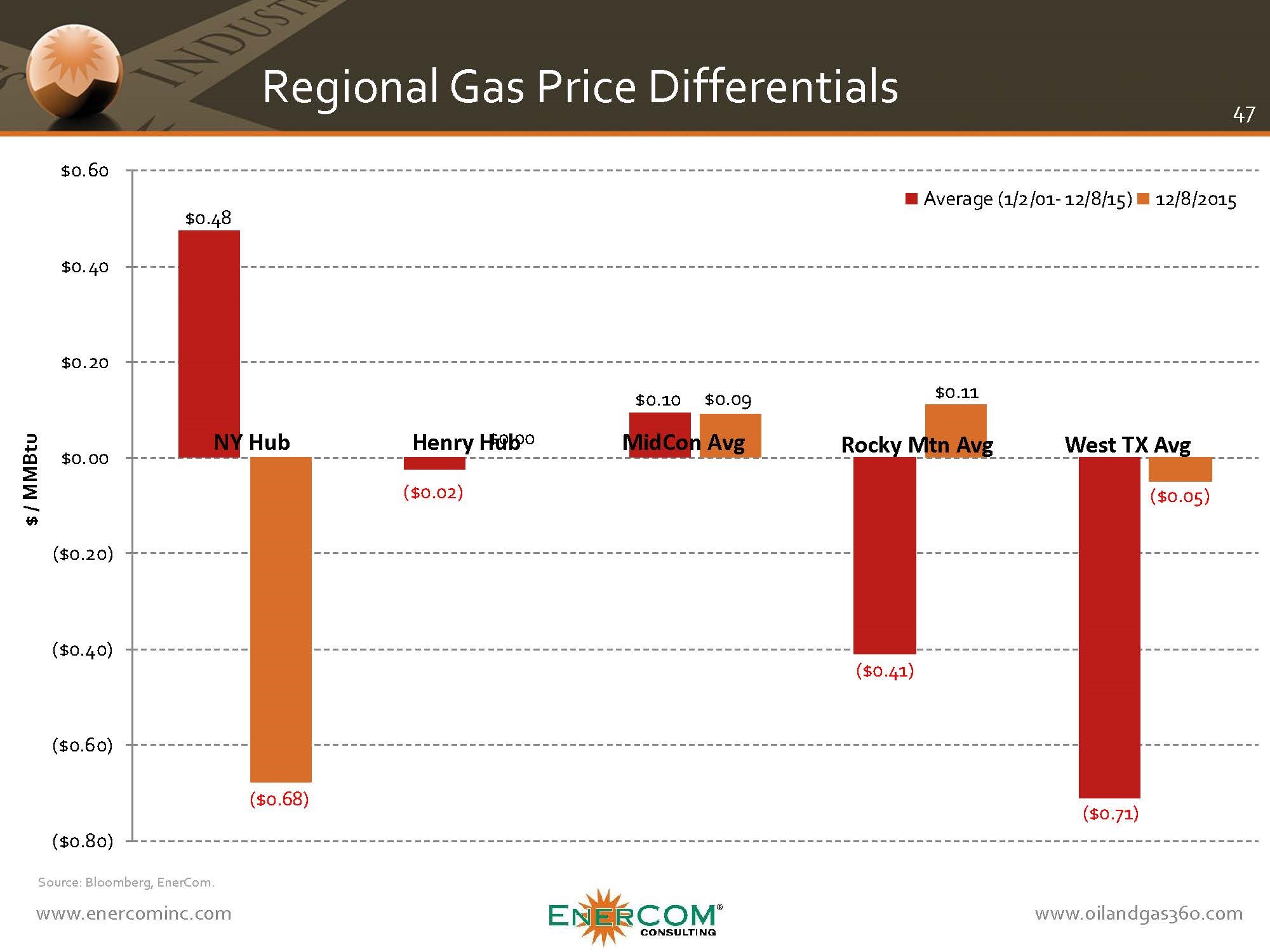

But there is another problem. Drilling activity in the Marcellus accelerated so quickly that it left infrastructure in the dust, and the need for pipelines and associated midstream utilities is paramount even though the rate of production has leveled off. Keith Burdette, Secretary of Commerce for West Virginia, repeatedly stressed the importance of infrastructure in a recent interview with Oil & Gas 360®. The significant amount of product and the limited amount of takeaway capacity has created an obvious bottleneck in the northeast, as evidenced by differentials compiled in EnerCom’s Monthly Report.

The New York Hub price is currently trading at a discount of nearly $0.70 to Henry Hub, meaning a regional Mcfe would fetch only $1.10 in the current market. You’ll be hard pressed to find a company who can profit from such a market.

So Again… Why are You Drilling?

Although the revenues are (much) lower than a year before, the operating companies are, in fact, major corporations that cannot exactly afford to shut off its production and therefore, its cash flow. The high decline curves of shale production requires drillers to keep on drilling or watch its product stream tail off. Revenues are a mandatory element of paying interest on borrowed debt, keeping the lights on at the company headquarters and distributing dividends (if any) to shareholders.

Other companies are obligated to certain contracts or commitments with rig or pipeline companies. Rather than cancel the contracts and pay a fine (along with not receiving revenue from the lack of volumes), producers choose to respect the obligations and deal with the low commodity prices.

“You might as well keep the rig operating and plow the capital into the ground than pay a penalty to the rig owner,” said Jeb Armstrong, Vice President of Energy Research for the Marwood Group, in a previous interview with Oil & Gas 360®.

It’s worth mentioning that not all wells are completed in the current environment, and some companies are building up a backlog of drilled but uncompleted wells as somewhat of a war chest for when prices rebound.

The Saving Grace

The Saving Grace

Of course, the previous cost estimates illustrated in this piece are made on an apples to apples basis and do not include beneficial factors like attractive hedges, enticing takeaway agreements and further improvements on the efficiency side. Let’s take a look at the game plan of our focus companies for 2016:

Antero Resources

There’s a reason Antero has higher costs than its peers: the company spent the last few years building up its position to roughly 565,000 net acres, and is running more rigs than any other Marcellus/Utica operator. Its business model through 2017 is titled “The Bridge to Better Oil & Gas Prices” in a company presentation, and is backed by some of the strongest hedge positions in the business. Its 2016 production estimate of nearly 1.8 Bcf/d is 100% hedged at $3.94/MMBtu, even though gas volumes are projected to increase by 25% to 30% on a year-over-year basis.

Increasing volumes so drastically in such a difficult market can cause questions at first glance, but Antero benefits from a midstream subsidiary that was spun off in November 2014. AR holds 67% of its interest today.

Its takeaway capacity, meanwhile, will increase by nearly 50% to 3.5 Bcf/d overall, and an estimated 85% of commitments will be sold to favorable markets. Capacity is expected to climb to 4.85 Bcf/d by 2018. The security stems from its midstream subsidiary, which was spun off in November 2014. Altogether, AR listed its average gas price holds a $1.22 premium to Nymex prices.

Entering 2016, Antero expects its DUC backlog to consist of about 50 wells and will complete said wells once a new gathering system is commissioned in late 2016. The company has not released 2016 guidance at the moment, but its expenditures for the current year are nearly half of the amount from 2014.

Entering 2016, Antero expects its DUC backlog to consist of about 50 wells and will complete said wells once a new gathering system is commissioned in late 2016. The company has not released 2016 guidance at the moment, but its expenditures for the current year are nearly half of the amount from 2014.

Cabot Oil & Gas

Cabot has the second-lowest cost structure in our analysis, and the company is opting for a more conservative growth plan than Antero, for comparison. According to a COG presentation, its 2016 plan focuses on increasing efficiency at the wellhead, meeting all drilling requirements and spending an “adequate level of growth capital to allow for acceleration of production to more favorably priced markets in 2017.” The Marcellus program requires just $175 million of annual maintenance capital to hold production levels.

Its internal rate of return on Marcellus wells is greater than 70% at $2.00/MMBtu realized prices, and the company plans on completing its 20 DUC backlog within the upcoming year. As with some of its peers, COG says it is waiting for new takeaway capacity to come online before boosting its volumes. Constitution Pipeline, scheduled for an in-service date in late 2016, will move 650 MMcfe/d.

Dan Dinges, Chief Executive Officer of Cabot, summed up the company’s near-term plans in its Q3’15 conference call, saying, “Our preliminary 2016 budget was built from the bottom up with focus on spending within cash flow at recent strip prices, while still providing measured growth in 2016 and still investing the appropriate amount of growth capital for 2017 that allows us to accelerate our production growth into better price points upon in-service of Constitution and Atlantic Sunrise.”

Dan Dinges, Chief Executive Officer of Cabot, summed up the company’s near-term plans in its Q3’15 conference call, saying, “Our preliminary 2016 budget was built from the bottom up with focus on spending within cash flow at recent strip prices, while still providing measured growth in 2016 and still investing the appropriate amount of growth capital for 2017 that allows us to accelerate our production growth into better price points upon in-service of Constitution and Atlantic Sunrise.”

The two projects will increase takeaway capacity by 1.35 Bcf/d by 2017. COG currently realizes a NYMEX discount of ($0.90) to ($1.00), but believes it can eventually realize a premium by 2018 as new takeaway projects are commissioned. The company is unhedged for 2016 and 2017.

EQT Corporation

The leader in cost structure according to our models, EQT Corp. will fund its $1 billion capital expenditure plan in 2016 entirely from cash on hand, cash from operations and proceeds from asset sales realized from a midstream drop-down. The company has developed a reputation for pre-funding the next year’s outspend. As discussed with Antero earlier, EQT is supported by a midstream subsidiary that provides easier access to higher priced markets. Production is expected to climb by 17.5% on a year over year basis despite a capital cut of roughly 40%.

Source: EQT Corp. December 2015 Presentation

EQT is somewhat going against the grain, allocating part of its budget to drill at least five capital-intensive Utica wells in the upcoming year. However, Steven Schlotterbeck, President of Exploration and Production, assured investors of the returns in the company’s Q3’15 conference call. “Using the lowest EUR of our range and assuming the high end of our cost per well target of between $12.5 million and $14 million per well we estimate returns at a $2 wellhead gas price to be north of 20% for a 5,400 foot lateral well,” he said.

A total of 72 wells are forecasted for 2016, and David Porges, CEO of EQT Corp., said the company is aimed at exploiting its lowest cost opportunities in the near term rather than what he described as “investing opportunities.” Approximately 80% of the company’s 600,000 net acres are held by production.

Gulfport Energy

Gulfport has loaded up on Appalachia acreage in the past few years, closing on three separate acquisitions for a total of nearly $900 million. Two of the deals were made after the commodity downturn, with the announcements coming in April and June of this year. Gulfport’s affinity for the region comes through loud and clear on its home web site page, as it declares the Utica Shale the “Hottest Play in North America.”

Its takeaway capacity for 2016 represents a year over year increase of 37%, boosting its total transportation to more than 1.2 Bcf/d. The company also believes about 90% of its sales are benefiting from premium pricing points, partially offsetting anticipated discounts of ($0.70) relative to Henry Hub. The company aims to hedge anywhere from 50% to 70% of its expected twelve-month production run rate.

To combat the difficult environment, Gulfport established a strategic joint venture with Rice Energy to build out its position. The arrangement, finalized in October, consists of Rice constructing and operating 77,000 leasehold acres owned by GPOR. It is the second such agreement between the two E&Ps. Rice also has a midstream subsidiary, adding to Gulfport’s takeaway ability.

While the company has grown dramatically in the last few years, management is taking its foot off the pedal in the new environment. It has decided against adding a fifth rig and is holding off on completions in Q1’16. “In today’s market, I believe what our industry needs is a more measured pace of growth,” said Mike Moore, President and Chief Executive Officer, in the company’s Q3’15 conference call. “We think it’s the sensible thing to do. Our hope is that our peers, some by choice rather than by necessity, will do the same.”

The company does have a strong balance sheet at its disposal, with a net debt to trailing twelve month EBITDA multiple of just 1.4x. However, it is not rushing to develop its position. “We’re okay paying renewals instead of drilling, and we’ll do that,” said Moore. There were 15 DUCs in its inventory as of November 5.

Rice Energy

Rice Energy has a lot of running room: in its combined 147,000 net acres, less than 10% is developed. Management also believes it can generate a 10% rate of return at a realized price of $1.99/Mcf, which was interesting in the fact that Rice is one of the few companies to truly acknowledge the regional depressed natural gas prices.

Rice is heavily hedged: 95% of Q4’15 production has a weighted average floor of $3.78/MMBtu and nearly 500 MMcf/d of 2016’s volumes have a weighted average fixed floor price of $3.51/MMBtu. Management targets hedging roughly 65% of its forecasted production up to two years out.

Rice braved the commodity environment by spinning off its midstream division about one year ago, and just announced an equity investment of up to $500 million for additional development. “Our firm transportation portfolio has been properly sized to meet, but never exceed, our production growth,” said Daniel Rice, Chief Executive Officer of Rice Energy, in the company’s Q3’15 conference call.

The company will have 21 wells on backlog entering 2016, and Gray Lisenby, Chief Financial Officer of Rice, says the hedge position, combined with the takeaway agreements, have the company in a favorable position entering 2016. “Based on the way the market looks today, our planned D&C investments in 2016 have a 20% to 30% IRR at current strip prices and will drive cash flow in 2017 through 2019,” he said.

Management says near-term leasehold expirations are still a couple years away and described the drilling requirements as a “non-issue.” 2016 plans have not been released just yet, but Rice is currently running a five rig program.

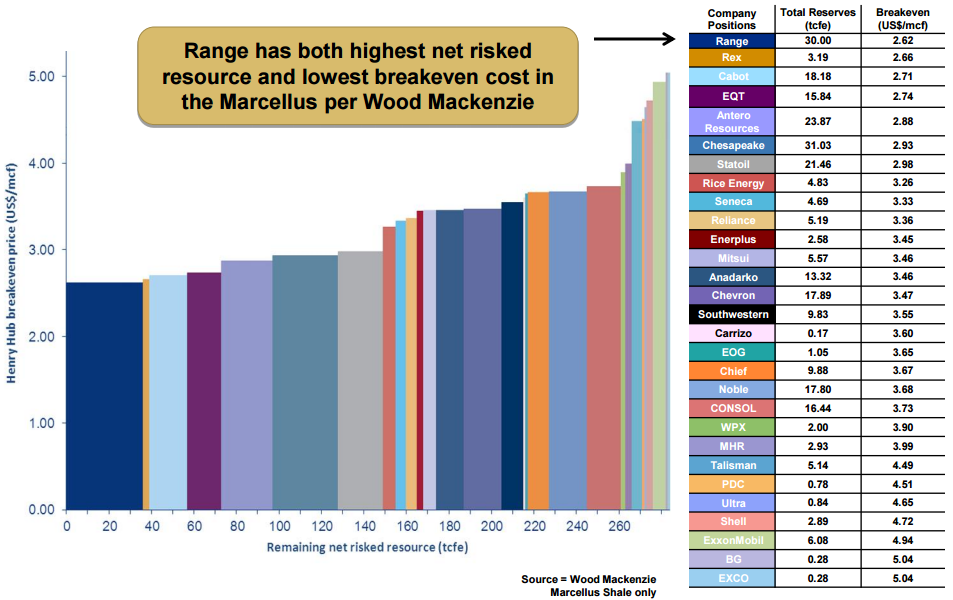

Range Resources

Range Resources

The founding fathers of the Marcellus Shale, Range Resources has forecasted line-of-sight growth of at least 20% based on economical wells and enviable midstream commitments. Range was one of the early movers in the play – an instrumental factor that has led to the company posting the lowest finding and development costs of any of its competitors. Analysis from Wood Mackenzie shows Range has both the highest net risked resource and lowest breakeven price when considering only the Marcellus region.

The aimed production increase is puzzling at first glance, considering the logistics that are involved. However, Range benefits from the startup of the Mariner East pipeline – a vital takeaway option for propane and ethane. RRC already has a 15-year contract to ship 40,000 barrels of ethane and propane per day to the Marcus Hook refinery in Pennsylvania, and is the only producer with firm capacity.

Range anticipates the propane transport market, regarding international buyers, will increase by 50% in 2016 – significantly opening up the demand window. RRC holds access to 800,000 barrels of propane storage (80% of capacity) to manage its inventory on a less restricted basis and provide upside in an expanded export market. It believes it can realize a $90 million uplift in annual net cash flow if combining the net effects from its pipeline contracts.

“We think the worst is behind us for priority NGL realized prices, in especially propane,” said Chad Stephens, Senior Vice President of Range, in the company’s Q3’15 call. “Mariner East give us a lot of optionality to work around seasonality demand.”

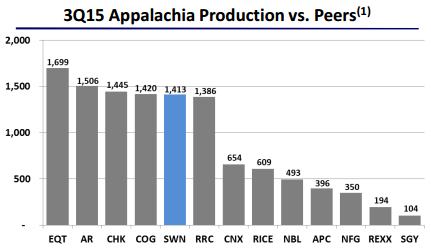

Southwestern Energy

Southwestern’s exploitation of the Appalachia has catapulted it to the third largest natural gas producer among the lower 48 states, with 2015 guidance representing growth of 27% on a year over year basis. SWN also has a very large position in the Fayetteville, another prominent gas play. A big production jump is coming in Q4’15, as the company has 40% of its 2015 wells coming online due to previous deferrals.

Management was imperative that the company would not take on any more debt or issue equity in the current environment. Production, however, will not falter as long as the company is adequately funded. “Historically what we’ve said is if it works in today’s environment, whatever today’s environment is, and it ranks out high on our list of the wells that we have, we would probably drill it if we have the capital to do so,” said Bill Way, President and Chief Operating Officer for Southwestern.

Management was imperative that the company would not take on any more debt or issue equity in the current environment. Production, however, will not falter as long as the company is adequately funded. “Historically what we’ve said is if it works in today’s environment, whatever today’s environment is, and it ranks out high on our list of the wells that we have, we would probably drill it if we have the capital to do so,” said Bill Way, President and Chief Operating Officer for Southwestern.

In the company’s Q3’15 conference call, management stressed that the rate of production growth is not a concern, but spending within cash flow is of utmost importance. A total of seven rigs are running in the Appalachia. SWN has opted to go light on the hedges, with 27% of 2015 volumes at an average price of $4.40.

“We have over 80% of our firm takeaway needs already committed for 2016 and 2017, if this asset grows by 35% in each year,” said Bill Way, President and Chief Operating Officer for Southwestern. “We’ll continue to monitor rig count and pipeline builds, but we continue to believe pipeline capacity will not be a constraint.”

Bottom line – The Best Cure for Low Prices are Low Prices

Though companies are still drilling, production growth is slowing. Cabot is talking about a budget to grow production by 2% to 10%, and the majority of the companies above have not yet released their 2016 guidance. Removing more rigs is a very real possibility, and agencies and industry veterans alike are already expecting 2016 to essentially be a repeat of 2015.

Claudio Descalzi, Chief Executive Officer of Eni SpA (ticker: E), believes the spending cuts can become so great that they would create an imbalance between supply and demand in the mid-term. Core Laboratories, a reservoir description and production enhancement company, has held a “V-shaped recovery” view ever since prices went south. Richard Bergmark, Chief Financial Officer of Core Lab, told OAG360® by email that their views have not changed even though inventories are near record highs.

Regardless of the prices in the near-term, incoming takeaway capacity in the northeast will help alleviate the sharp price differentials. A note from Raymond James Equity Research says pipeline capacity in the northeast could triple by 2019 if all projects materialize on schedule. The firms says that incoming takeaway availability, combined with drilling efficiencies and the ever-growing resource estimates of the Appalachia, provide a bearish outlook for Henry Hub and its associated spot prices. “The bottom line,” Raymond James says, “is that we think readily available Marcellus and Utica gas supply will keep a lid on overall U.S. natural gas prices for the next several years.”