Record cold temperatures persist across the United States, shutting in schools and cancelling flights. Snow is making unusual appearances among the Gulf Coast and Southeast states, crippling commutes and slowing the economy. Oil and gas producers have also felt the chilling effects from this winter. Companies like Pioneer Natural Resources (ticker: PXD) and Apache Corporation (ticker: APA) admitted the severe weather directly hampered operations in the most recent quarter.

Record cold temperatures persist across the United States, shutting in schools and cancelling flights. Snow is making unusual appearances among the Gulf Coast and Southeast states, crippling commutes and slowing the economy. Oil and gas producers have also felt the chilling effects from this winter. Companies like Pioneer Natural Resources (ticker: PXD) and Apache Corporation (ticker: APA) admitted the severe weather directly hampered operations in the most recent quarter.

Forecast Indicates Cold Streak to Continue

As depicted by the map on the right from the National Oceanic and Atmospheric Association (NOAA), the cold snap is expected to continue for as long as two more weeks. Widespread effects from the cold can be seen heavily in the Williston Basin and even extends to Texas operations and the Marcellus in the northeast. The trend  is expected to continue, particularly for the Midwest, up until April 2014. In the meantime, those particular areas are enduring wind chills of up to 30 below zero. Operators are hamstrung with icy roads, frozen equipment and power outages.

is expected to continue, particularly for the Midwest, up until April 2014. In the meantime, those particular areas are enduring wind chills of up to 30 below zero. Operators are hamstrung with icy roads, frozen equipment and power outages.

Market Feeling the Heat (or Lack Thereof)

The extreme cold has put the strain on the heating market. According to the Energy Information Association’s (EIA) Short-Term Energy Outlook released in January 2014, estimates for the winter of 2013-14 predict this season to be the coldest in three years. The current winter represents a significant rebound from the unseasonable warmth of 2011-12 – this winter’s heating oil consumption is roughly 20% higher. In turn, the spiked residential consumption rates of heating oil resulted in a 12 cent price increase in the EIA’s latest Heating Oil and Propane update. Its current price of $4.17 is the second-highest on record.

Additionally, it’s safe to speculate consumption and outlook numbers would be much higher if the cold were to stay consistent. The majority of U.S. states enjoyed warmer than average weather through the early winter months of October, November and December. Amazingly, the average temperature in the Lower 48 states is still 8.3 degrees warmer than the normal 30-year temperature and 2.6 degrees warmer than January 2013 levels, clearly showing the current climate disparity amongst eastern and western states.

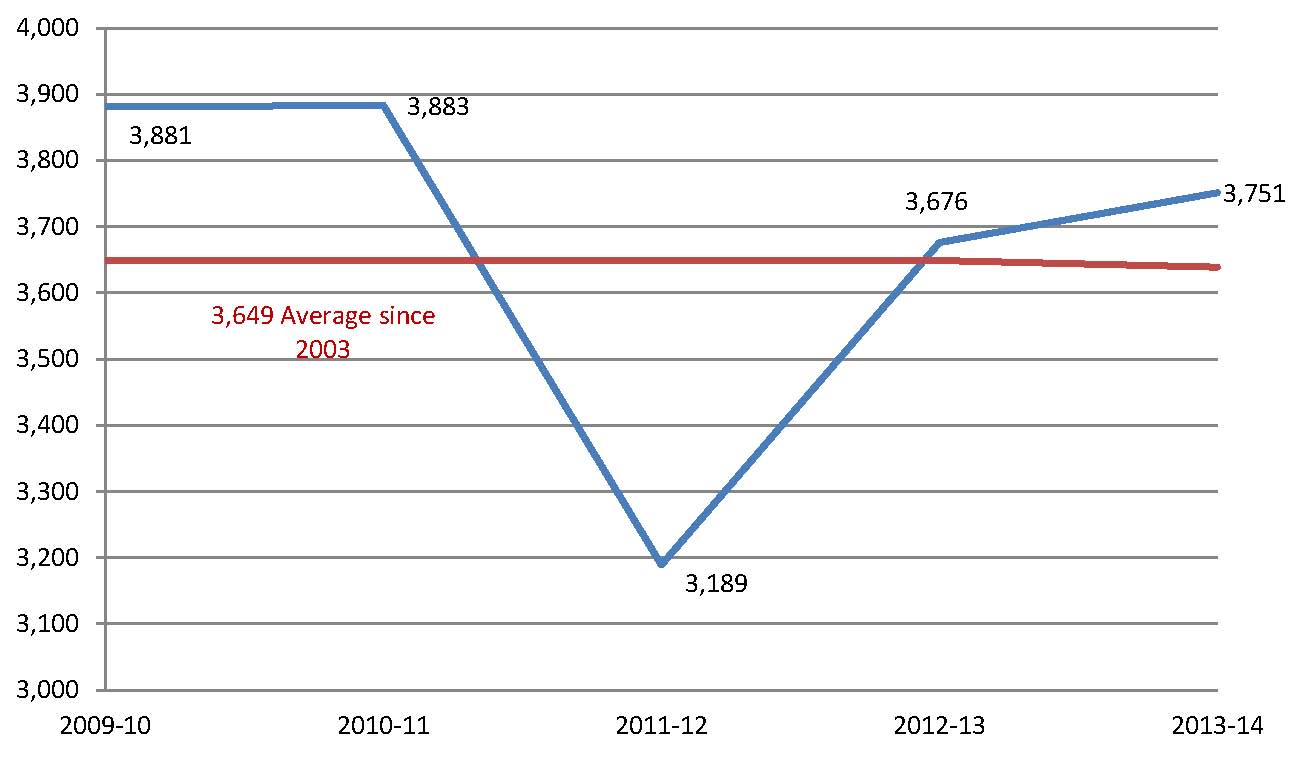

The EIA forecasted colder weather in October 2013, expecting the Northeast to be about 3% colder than “normal” temperatures. The chart below lists heating degree days and is reflective of the temperature drop. The number of heating degree days projected for the current year are 18% greater than the final number in 2011-12.

Natural Gas Setting Records

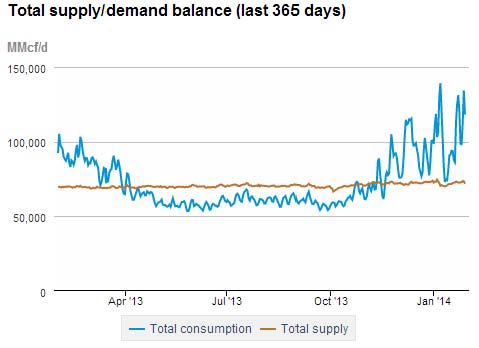

Natural gas, on the other hand, is proving to be more indicative of widespread temperatures among the coldest in decades. Frozen pipelines and slowed production resulted in the greatest withdrawal of gas storage since the EIA began recording the data 20 years ago. The storage was already experiencing higher-than-average withdrawals prior to the record decrease of 287 Bcf for the week ended January 10. The effect spilled over into the natural gas market of the Midwest and Northeast, where the resource fuels between 50% and 68% of all homes. Gas, along with electricity, continues to gain popularity on a national level due to their cost effectiveness in comparison to more traditional resources like heating oil and propane.

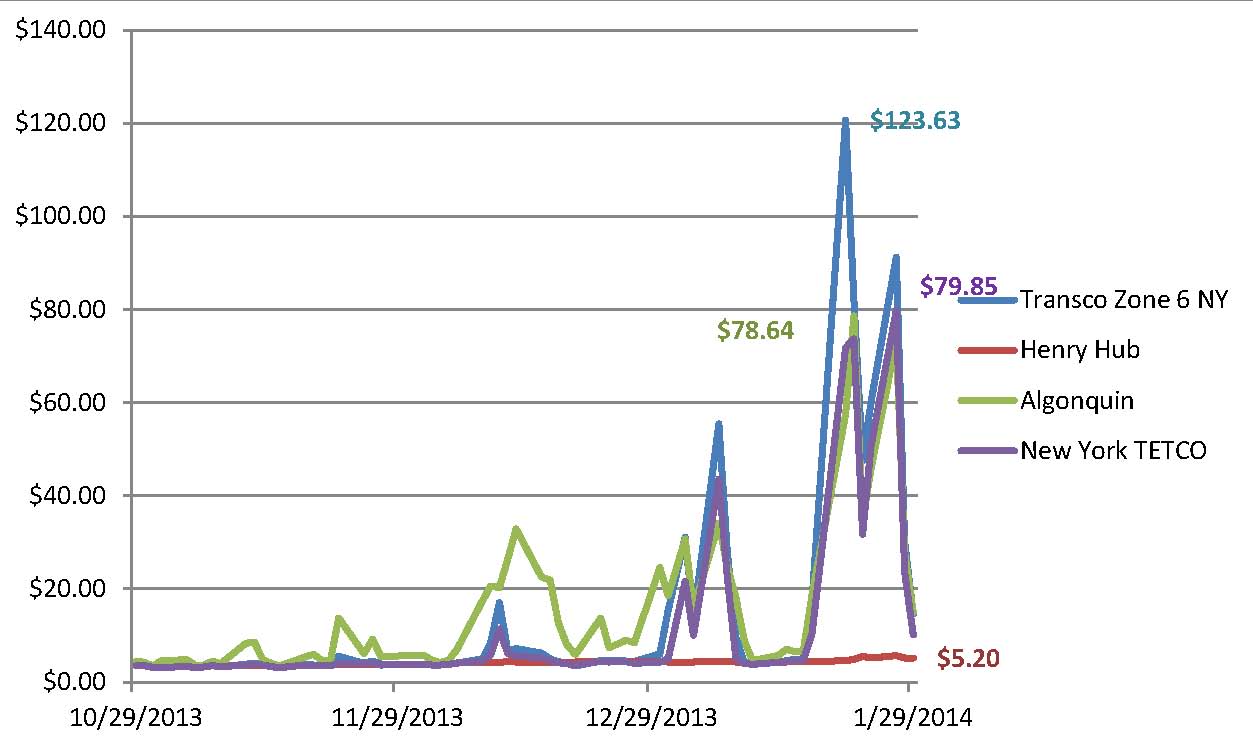

The Northeast markets are already somewhat constrained due to a lack in infrastructure. The need for the resource reached staggering levels in the recent cold snap, and prices shattered previous records by skyrocketing to more than 20 times times the Henry Hub price. The spot price at the Transco 6 Pipeline to New York closed at $123.63/MMBtu on January 21, 2014, following the weekend and Martin Luther King Day. The spot price for the previous three-month period averaged $13.84 per MMBtu.

The Northeast markets are already somewhat constrained due to a lack in infrastructure. The need for the resource reached staggering levels in the recent cold snap, and prices shattered previous records by skyrocketing to more than 20 times times the Henry Hub price. The spot price at the Transco 6 Pipeline to New York closed at $123.63/MMBtu on January 21, 2014, following the weekend and Martin Luther King Day. The spot price for the previous three-month period averaged $13.84 per MMBtu.

Natural gas futures also rose to the highest level since February 2010. February 2014 futures rose 36 cents to end at $4.69/MMBtu, a rise of roughly 8% compared to the previous week. The 12-month strip also climbed 20 cents to reach $4.37, a 5% rise. However, the strip is below the near-month futures price, indicating expectations that the elevated winter prices are a short-term occurrence.

The latest inventory report by the EIA announced a withdrawal of 230 Bcf, leaving a current natural gas storage of 2,193 Bcf. Current inventory is 22.5% below January  2013 levels and 16.6% below the five-year average. The report said the top five daily natural gas consumption rates of natural gas January 2014 exceed all dates reaching back to 2005.

2013 levels and 16.6% below the five-year average. The report said the top five daily natural gas consumption rates of natural gas January 2014 exceed all dates reaching back to 2005.

Consumption is still exceeding demand, but natural gas prices are quickly returning to normal. Gas dropped 8.3% on January 30, 2014. “There are shops that have interpreted the slight warmer revisions to the forecasts as proof that the end of winter is in sight,” said Teri Viswanath, director of commodities strategy at BNP Paribas SA in New York. “The market is retracing the fact that it became slightly more overbought.”

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.