Delaware wells show IPs above 2,700 BOEPD

Anadarko Petroleum (ticker: APC) announced third quarter results today, showing a net loss of $699 million, or ($1.27) per share. After adjusting for special charges, Anadarko took a loss of $427 million, or ($0.77) per share.

The company produced an average of 626 MBOEPD in Q3, up slightly from the pro-forma 612 MBOEPD Anadarko produced in Q2. Oil sales volumes were below guidance on the effect of the hurricanes, but were still 8% above Q2 on a divestiture-adjusted basis.

Much of this oil volume growth was due to expansions in the company’s U.S. operations, particularly in the DJ and Delaware. Anadarko currently has 12 Delaware rigs running, and an additional six in the DJ. The company achieved record oil well production in the Delaware this quarter, producing 44.5 MBOPD, and is on target for its goal of 50 MBOPD at year-end. Anadarko reports that three Delaware Basin wells had very high production, with 30-day IPs above 2,700 BOEPD, 60% of which is oil.

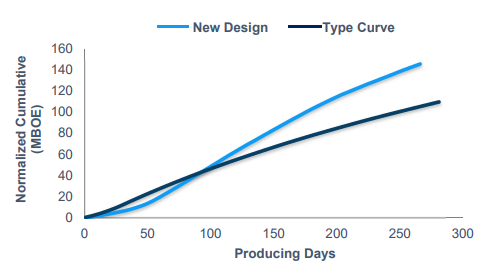

New completion design provides 40% oil production uplift

Production in the DJ is also rising quickly, and is on schedule to hit 100 BOPD by year-end. Anadarko reports that preliminary results from its new completion design show cumulative oil uplift of more than 40%. This represents a to-date NPV update of about $240,000 per well, compared to the original design. This uplift will add up, as the company turned 79 wells to sales in the quarter.

Legacy Wyoming gas sold

In addition, Anadarko announced the sale of its Moxa asset in southwest Wyoming today. This asset is a legacy gas play, which produced 72 MMcf/d in Q3. Anadarko reported that it would receive $350 million for the assets, but declined to state the buyer.

Mozambique LNG making progress

Anadarko reports that it is making progress on its Mozambique LNG project, and finalized the marine concession agreements with Mozambique’s government in Q3. In the last month, the company reached a 20-year purchase agreement with a Thai company for 2.6 MTPA of LNG.

Q&A from today’s Q3 earnings call

Q: You discussed your approach to capital allocation and discipline in your opening comments and you elected to return more cash to shareholders recently with the buyback. Given the shift, what are your thoughts on tempering the 15% longer-term growth rate in favor of returning a greater portion of cash flow to investors?

Al Walker: Well, that’s an understandable question. The 15% CAGR, I think you’re referring to that we put out earlier, as you well know, is driven off of a five-year assumption at $50 for WTI. We also have been particularly focused, as we looked at that, on returns and capital discipline is a part of it. And when we announce our capital plan once our board approves that plan, I think you can understand a little more at that time the details around it.

Consequently, I don’t think at this juncture talking about the compounded annual growth is as important as making sure that we give you the type of returns in a $50 world that this budget, we believe, if ratified will provide. So growth at this point is really going to be, as I said earlier, an output, not an input.

Q: So when you’re kind of approaching potentially addressing that number, you’re starting off with a cash return threshold or a percentage amount on a commodity price and that kind of building up from there. Is that at least the process we should think of?

Al Walker: We’re not using cash return per se. It’s certainly one of the variables. Think of it as a multi-variable equation, of which that would be one of the components.

Q: Could you just talk about debt levels? Because those remain somewhat relatively elevated if we look at the biggest names, whether or not how hard was it to decide whether to pay down debt or to buy back stock?

Robert Gwin: It wasn’t very difficult at this stage to decide between stock and debt, because we’d buying back debt at a premium, and we felt that we’re buying back stock at a significant discount. I think though it’s fair to say that as we move forward, we’ve got to consider the entire capital structure as a potential use of proceeds for free cash flow. Because certainly, we understand that the debt structure of the company has an impact beyond benefiting shareholders from a return on equity standpoint, it certainly has an impact sometimes on the way you trade across cycles.

And so it’s — debt reductions are certainly on the table at free cash flow in the future, but leverage is not a concern to us in an absolute sense, because of our liquidity position and the fact that we have very few near-term maturities.

We’ve got a $900 million slug coming up in 2019, and that’s about it over the course of the next several years. So it’s an area that we consider, but it’s not something that we’d say is on the shortlist today. But we’ve still got a material cash position after the share buyback is completed. And as I mentioned, we expect to be inside of cash flow. And hopefully, with any improvement in the commodity, which I think is a certainly a possibility with some recent changes we’ve seen in the market and with what sounds like a sector that’s much more focused on capital discipline, we might see some free cash flow, and then we can focus more significantly on returns to shareholders. And obviously, if we pay down debt, that benefits the shareholders directly from an economic standpoint buying back some of their company form.