360 Feed Wire

Q2 upstream deals totaled $2.6 billion, more than a 200% increase over Q1

Austin, Texas (July 1, 2020) – Enverus, the leading oil & gas SaaS and data analytics company, has released its summary of Q2 2020 U.S. upstream M&A. The update shows upstream deals staged a small recovery to $2.6 billion from only $770 million during Q1. However, Q2 still ranks as the third lowest quarterly value since 2009.

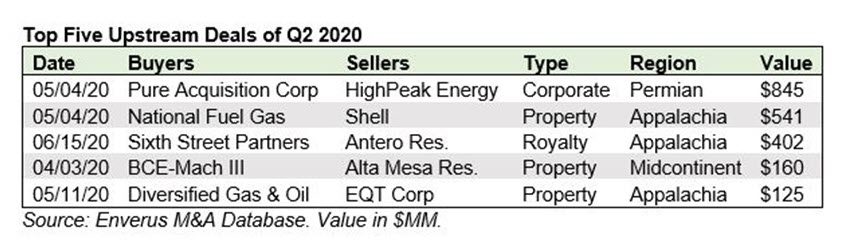

The largest deal of Q2 targeted the oily Midland Basin, but Pure Acquisition Corporation’s $845 million combination with HighPeak Energy was the second iteration of a deal initially announced in late 2019 and then restructured after oil prices declined sharply. Otherwise, the majority of the biggest transactions during Q2 targeted gas-producing Appalachian assets.

“With the uncertainty around oil, the limited buyers largely targeted low-cost natural gas assets during Q2,” said Andrew Dittmar, senior M&A analyst at Enverus. “Broadly, the market for new deals remains highly challenged, particularly in oil plays.”

![]() The largest of the gas deals was Shell’s $541 million sale of its upstream and midstream business in Appalachia to National Fuel Gas. The next largest deal consisted of the sale of an overriding royalty interest by Appalachian producer Antero Resources to private investor Sixth Street Partners for $402 million. Overall, gas increased its share of M&A from 5% in 2019 to 30% year-to-date.

The largest of the gas deals was Shell’s $541 million sale of its upstream and midstream business in Appalachia to National Fuel Gas. The next largest deal consisted of the sale of an overriding royalty interest by Appalachian producer Antero Resources to private investor Sixth Street Partners for $402 million. Overall, gas increased its share of M&A from 5% in 2019 to 30% year-to-date.

“Relatively strong future pricing is likely driving demand for gas assets,” said Dittmar. “While the spot market for natural gas is still suffering from low prices, the future curve 12 or 24 months out is significantly higher. That is permitting buyers to hedge future production at levels that support deal economics.”

The Antero Resources sale also checks the box on one of 2020’s other relatively positive stories, royalty and mineral deals. After a strong showing in the second half of 2019, royalty deals accounted for more than 20% of Q2’s total value. Institutional capital bought the main royalty deals in the quarter, including Sixth Street Partners and a $100 million acquisition by EnCap-sponsored Pegasus Resources in the Permian Basin. “Royalty and mineral interests remain a popular way to gain exposure to oil and gas upside while limiting the financial risks inherent with participating in working interests in a volatile market,” added John Spears, director of Market Research at Enverus.

Another byproduct of the uncertain market is the use of contingent payments, mostly linked to commodity prices, to distribute risk between buyers and sellers along with helping overcome a wide bid-ask spread. Most of the largest deals in the quarter, including the National Fuel Gas acquisition plus a pair of Appalachian asset deals by Diversified Gas & Oil, included a contingent payment portion linked to prices. The Antero deal linked its contingent payment to volume thresholds along with including a reversion in interests once certain return thresholds are reached for the buyer.

A number of Chapter 11 bankruptcy processes were announced during Q2, including Chesapeake Energy, a pioneer in the emergence of shale. While Chesapeake is pursuing a reorganization, recent filings especially among private companies appear to be resulting in more proposed 363 sales relative to past downturns. Bankruptcy sales processes include Gavilan Resources (Blackstone), Templar Energy (Cohesive Capital), and Sable Permian (The Energy and Minerals Group). The rise in proposed sales may indicate fewer debtholders are willing to work a restructuring deal to take equity and would prefer an exit, even if that involves a sale into a challenging market.

For the remainder of 2020, gas assets are likely to continue to transact as long as future pricing supports deals and possibly spread to other areas of low-cost supply like the Haynesville in Louisiana and Texas. Additionally, there seems to be continued support for royalty acquisitions like the Sixth Street deal with Antero.

However, the market for assets in major oil shale plays, which were the key driver of M&A values for quite a few years, is likely to remain challenged barring a rally in crude prices. Public companies of all sizes are facing significant financial headwinds, making it difficult to convince skeptical investors on the value of M&A. In the past, private equity has deployed opportunistically in these types of markets but is currently facing its own struggles. Eventually, a fresh infusion of capital from either public, institutional, private investors, or international markets will likely be needed to restart oil-focused deals.

Enverus is the leading data, software, and insights company focused on the energy industry. Through its SaaS platform, Enverus provides innovative technologies and predictive/prescriptive analytics, empowering customers to navigate the future. Enverus’ solutions deliver value across upstream, midstream and downstream sectors, enabling the industry to be more collaborative, efficient and competitive. With more than 1,300 employees across the globe, the Company’s solutions are sold to more than 6,000 customers across 50 countries. Enverus is a portfolio company of Genstar Capital and brings together the technology of Drillinginfo, RS Energy Group, PLS, 1Derrick, MineralSoft, Midland Map Co., Oil-Law Records, MarketView, DataGenic Group, PRT, Oildex, Cortex, Red Dog Systems, and RigData as one company. Creating the future of energy together. Learn more at www.enverus.com.

Jon Haubert | 303.396.5996