Arabella Exploration, Inc. (ticker: AXPLF) is an independent oil and natural gas company focused on the acquisition, development and exploration of unconventional, long life, onshore oil and natural gas reserves in the southern Delaware Basin in Reagan and Pecos, Texas counties. The company is utilizing multi-lateral wells to develop the Wolfbone play, which is located in the Permian Basin. The Midland, Texas based E&P serves as the operator of its properties through its subsidiary, Arabella Petroleum Company, and was formed from an acquisition with Lone Oak Corporation in October 2013.

The Wolfbone play overlaps two shales and has estimated ultimate recovery of 240 MBOE (80% liquids) per well. Development of the play has just begun – the Fort Worth Petroleum Club reported only 31 horizontal wells had been drilled in the area in April 2013.

Wolfcamp Operations

Arabella is running one rig and is targeting five different levels of the Wolfcamp formation. The company has drilled and completed seven wells to date and is in the process of completing one additional well. Jason Hoisager, President and Chief Executive Officer of Arabella, told OAG360 at The Oil & Services Conference™ 12 that the company has used a multi-lateral horizontal method on all but one of its wells. The technique can also be used to re-enter old wells and Hoisager believes it will result in cost effective production.

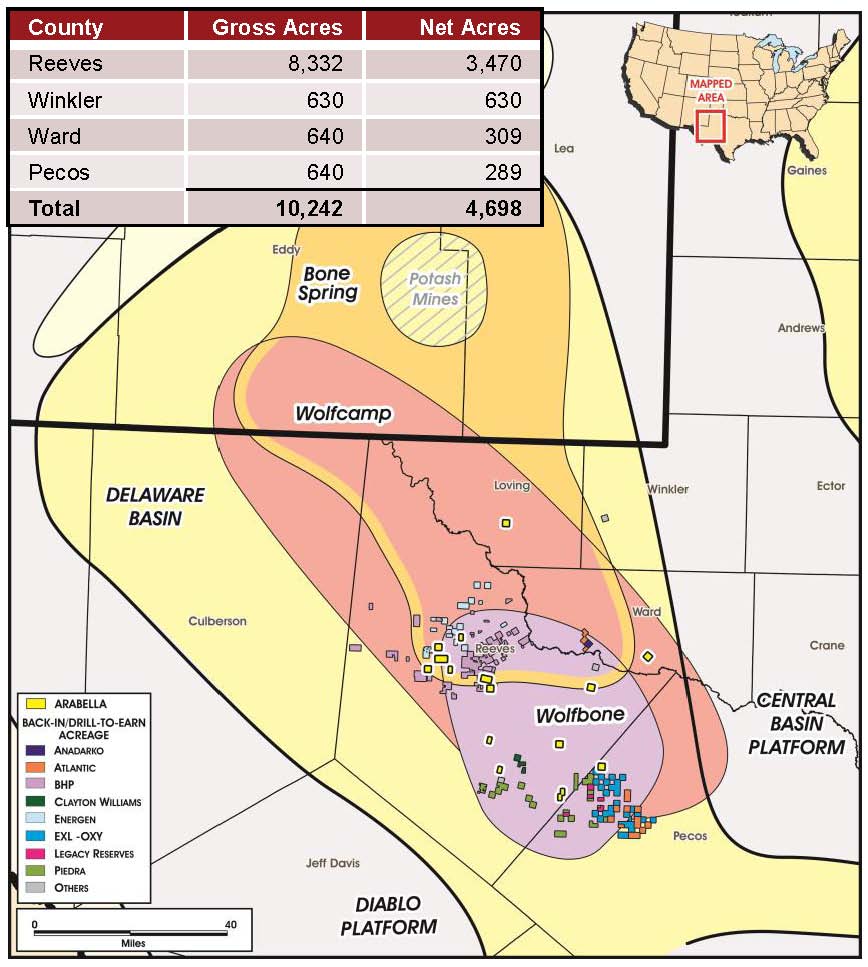

Source: Arabella April 2014 Presentation

“As a general rule of thumb, we hold about a 50% working interest in all of our properties,” said Hoisager in a conference call with analysts and investors on June 17, 2014.

2014 Update

On June 16, 2014, Arabella announced its Emily Bell #1H well returned a peak initial production rate of 1,100 BOEPD and naturally flowed back 600 BOEPD (85% oil) for the next 12 days after being placed online. The company plans on drilling three more wells in the Emily Bell tract and, based on early estimates, expect the wells to hold 600 MBOE of estimated ultimate recovery. In the conference call, Arabella management said other operators in the play, including Rosetta Resources (ticker: ROSE) and Concho Resources (ticker: CXO) have placed well estimates at the same number.

The Woods #2H (28.5 WI) reached total depth in May and is expected to be completed in June. The Woods #2 is an offset well to the Woods #1H, which returned a peak 24-hour rate of more than 1,200 BOEPD and is believed to hold 600 MBOE of estimated ultimate recovery.

The Emily Bell #1H and Woods #2H were drilled at an average cost of $4.4 million apiece – down roughly 25% from previous drilling costs of $5.9 million. Completion costs are consistently around $3 million, bringing total well expenditures to $7.4 million apiece. Arabella, along with its drilling consulting company, believe costs can be maintained for the long-term. Management said the Woods #2H was completed without a pilot hole and the company will take the same approach for the drilling of the Emily Bell #2H.

“Drilling in the southern Delaware basin is a headache, primarily because of the overpressured reservoir, but you also have some shallower problems up the hole you have to contend with,” said Hoisager. “The more wells we drill the better we’ll get overall. The drilling consultants are a great example of our approach; we brought in a fresh set of eyes and saw an opportunity to make some tweaks. I would look for the well costs to continue to come down as well as spudding times becoming closer together.”

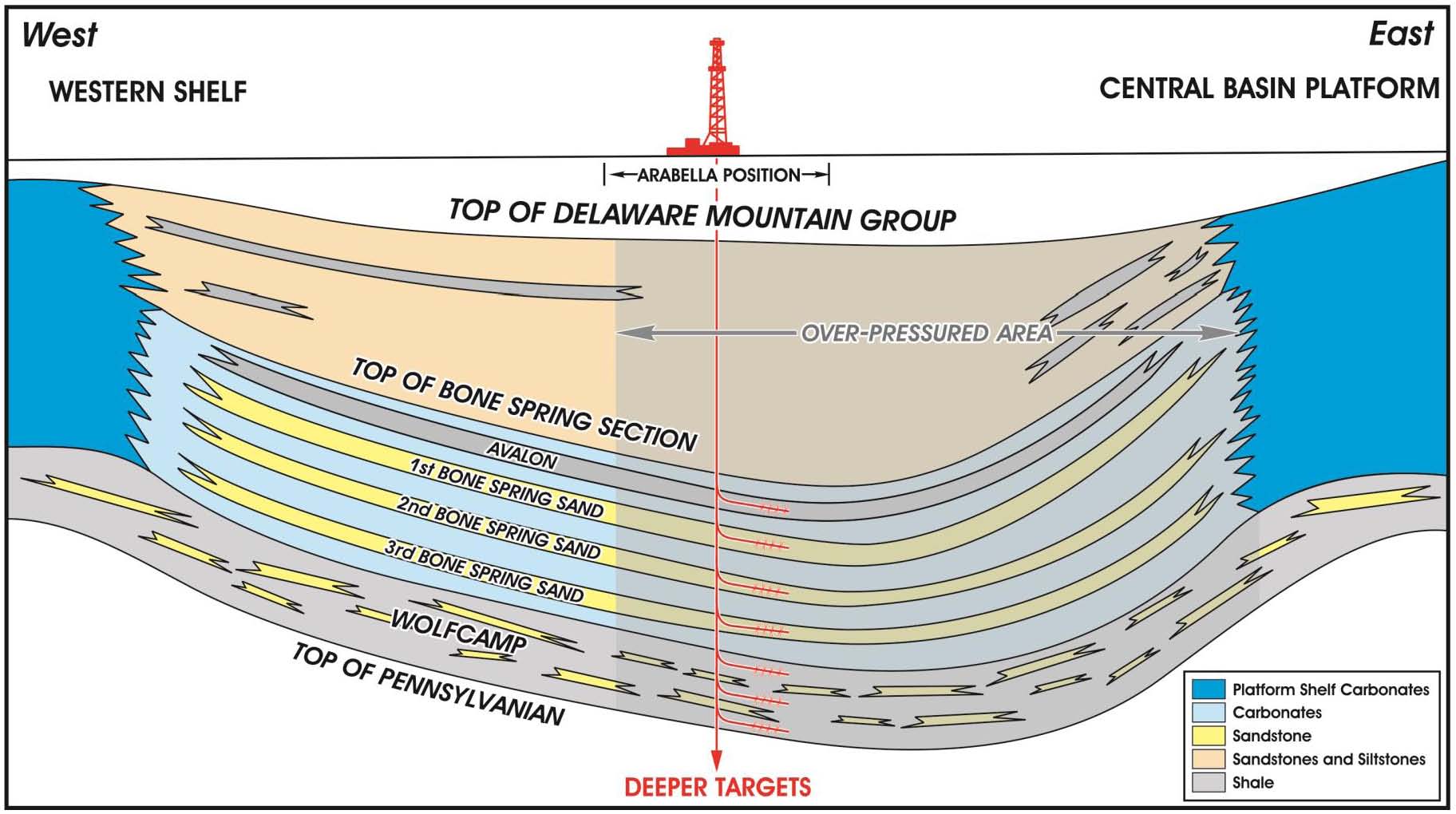

Source: Arabella April 2014 Presentation

Gas Lifts Boosting Returns

In an operations update on May 22, 2014, Arabella announced its Graham #1H well was reworked and is on a gas lift. Production was in the range of 100 BOEPD to 125 BOEPD for the month of May. Its Jackson #1H well, whose initial production reached 875 BOEPD in January, flowed back naturally at 125 BOEPD to 175 BOEPD until April. The well has also been placed on a gas lift and was producing 150 BOEPD to 250 BOEPD at the time of the update. The Graham #1 was re-worked with the same method and is producing 100 BOEPD – in line with the company’s type curve.

The company divested 1,280 gross non-producing acres (666 net) in March and April of the current year generating a total of approximately $2.8 million. The properties had originally been purchased for approximately $1.4 million, equaling roughly double the return on the original purchase price. Arabella said the properties were sold in order to focus on its core properties in the Wolfbone.

Year-End Forecast

In the conference call, Arabella management said net production was roughly 1,000 BOEPD. The company expects laterals to increase production rates as the exploitation process continues. Management said laterals are generally 4,000 feet to 4,200 feet in length, which is sufficient for one full section. An additional eight wells have been identified and the company expects production to reach 2,000 BOEPD once all are completed. Management has instilled a goal to double reserves by the end of 2014.

“Some of these wells may extend to 2015, but we’re working like mad men to get them completed in 2014,” said Hoisager.

A third party reserve report for the period ended December 31, 2013, revealed 2.1 MMBOE of proved reserves for a PV10 value of $32.8 million. Management has established a goal of doubling those reserves by the end of the calendar year.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.