Back in November 2014, Oil & Gas 360® asked an analysts who follows the MLP space closely if MLPs were a fad. He responded, “This is like asking me if Western Civilization is a fad.”

That exchange occurred on Nov. 18, 2014, nine days prior to last Thanksgiving Day’s OPEC announcement. The very one that sent the price of crude oil—along with the share prices of companies who drill, complete and operate wells, develop fields, build pipelines, and produce and ship petroleum—into what’s coming up on a year-long nosedive.

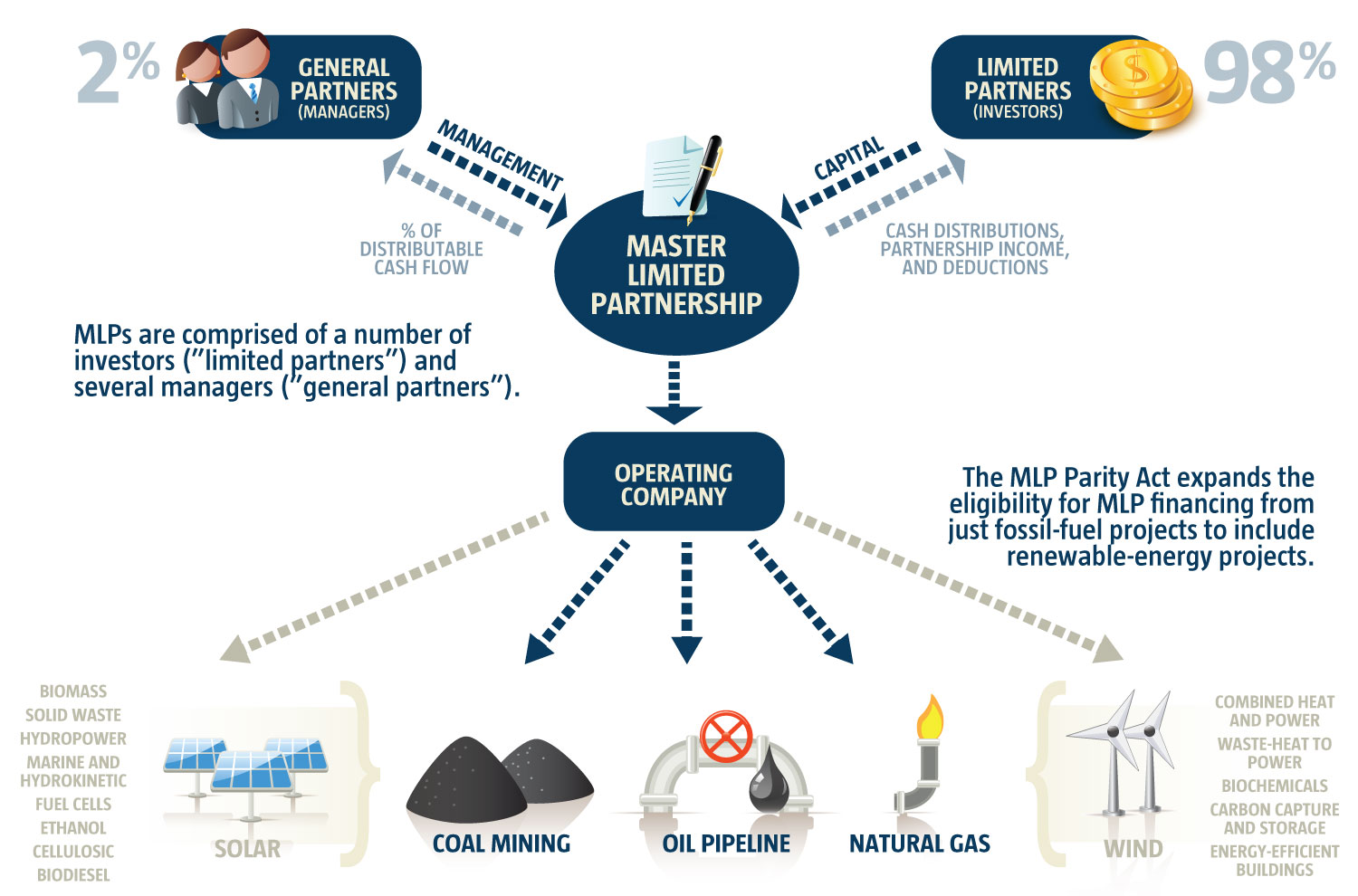

Master limited partnerships (MLPs) have historically been a popular publicly traded investment vehicle because of their track record of steady, higher than average dividends to the partnerships’ unitholders. This is true because the structure avoids a corporate tax, allowing the MLP to distribute more of its cash flow in dividends to its unitholders, compared to a traditional C-corp. structure.

Oil and gas MLPs became popular as a place to offer investors participation in fee-based, cash-generating midstream infrastructure assets. It’s a way for companies to maximize the payout from long-life assets. Some companies also form MLPs from E&P assets, but these MLPs tend to be much more oil price-sensitive. Unlike their E&P counterparts, midstream MLPs have generally said that being tied to fee-based revenue for energy transportation tends to leave them more insulated from commodity price. But is this really the case?

While no energy company, MLP or otherwise, has managed to exist in isolation from the decline in oil and natural gas prices, MLPs nonetheless have remained attractive to investors looking for higher dividend yields.

Dragged Down by Lower Commodities, are MLPs still Attracting Investors?

In the past year, wide fluctuations in the benchmark Alerian MLP Index (ticker: AMZ) have pushed some investors out of the MLP market. On October 16, the index was down 23% since the beginning of the year. Still, uncharacteristic large swings now have it up significantly from its low point on September 29, 2015, when the index was 38% below its starting point in January.

Source: Alerian

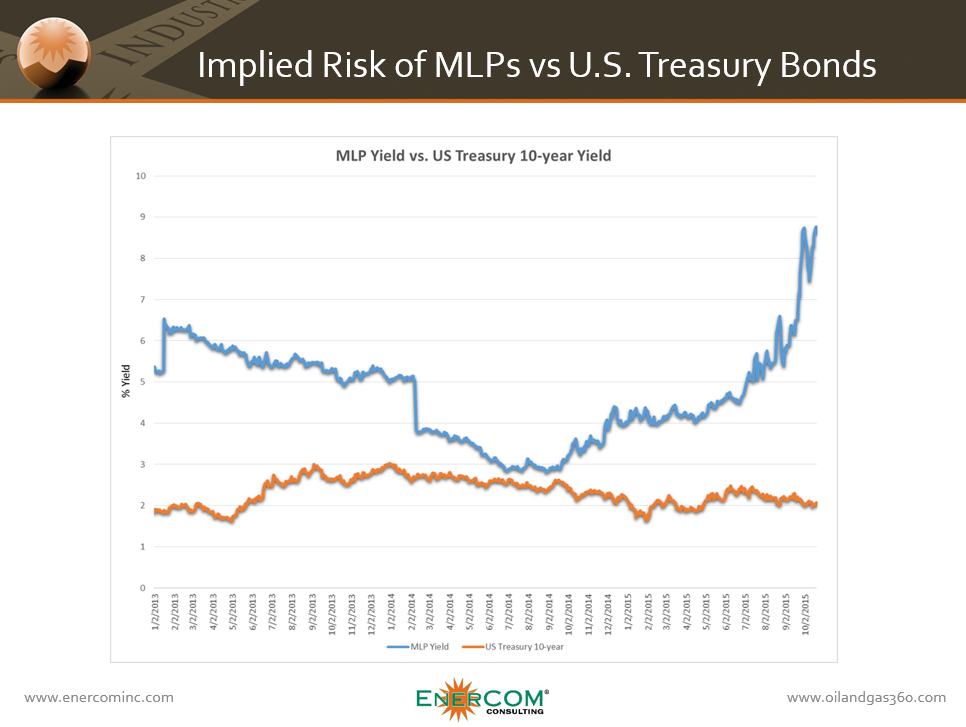

Treasuries are considered a risk-free investment, and where there is little risk there generally follows little reward. Returns generated from owning certain MLPs are several magnitudes higher than the risk-free 10-year U.S. Treasury bond. But when gambling on the success of any company or partnership trying to make a profit, there’s more reward to be found by investors willing to take on some risk and put cash into an MLP, rather than stick it under a mattress, buy Treasury bonds or earn less than one percent bank interest.

4 MLPs: How Have they Performed?

Information compiled by EnerCom Analytics looked at some of the strongest performing midstream MLPs in its database of 60 midstream MLP names. For its analysis, Oil & Gas 360® selected Boardwalk Pipeline Partners LP (ticker: BWP), EQT Midstream Partners LP (ticker: EQM), Inter Pipeline Ltd (ticker: IPL CN) and Magellan Midstream Partners LP (ticker: MMP). Taking the yield from those four companies compared against the yield of the U.S. 10-year Treasury bond.

The difference in yields between MLPs and Treasury bonds acts as a “risk premium” that unit-holders see with their investment. The yield spread between the MLPs and Treasuries narrowed from January 2013 to October of 2014. But following the OPEC Thanksgiving Day 2014 decision to maintain production, the yield on MLPs shot up as the energy industry went into a tailspin, taking market value of MLP units down with it and pushing yields up as long as distributions stayed steady.

Data: Bloomberg, compiled by EnerCom Analytics

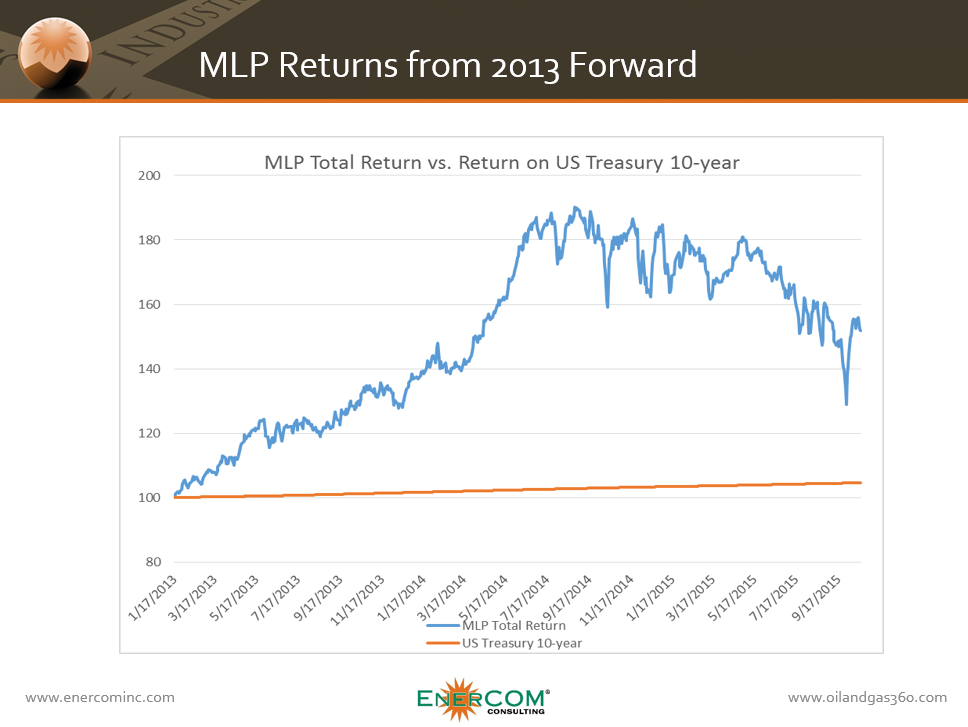

The total return from the MLP group, which was calculated as the sum of the four companies’ stock prices and dividends, was normalized against the total returns for Treasury Bonds from January 1, 2013, to October 17, 2015. For investors who owned those four MLPs, the total returns were 51.87% higher over the period than U.S. Treasury Bonds.

Data: Bloomberg, compiled by EnerCom Analytics

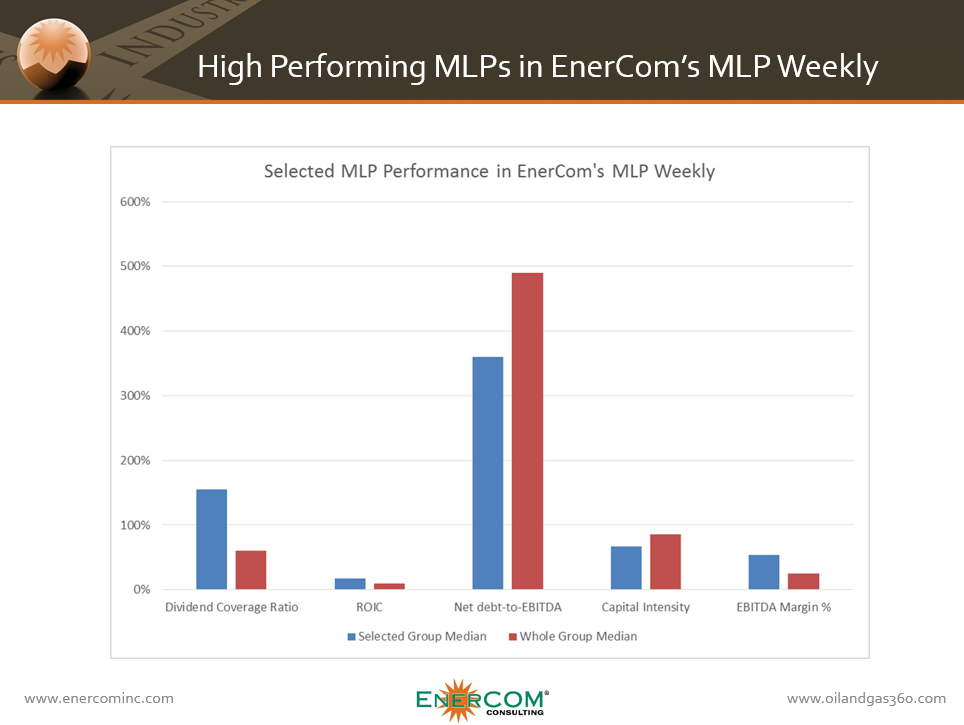

The four MLPs have performed well relative to their peers during the current commodity price down-cycle. EQM, for example, has the second-highest dividend coverage ratio in its peer group at 1.9x and a net debt-to-EBITDA of 2.3x, well below the group median of 4.9x, and an EBITDA margin of 80%, the highest among its peers.

The other three MLPs highlighted by EnerCom also have favorable metrics compared to the group of 60 MLP peers tracked by EnerCom, with Magellen Midstream’s capital intensity (the percentage of every dollar the company spends to maintain its current operations) of just 45% is well below the group median. Its ROIC of 21.3% and EBITDA margin of 50% are both twice the group medians of 9.8% and 25%, respectively. Magellen’s net debt-to-EBITDA of 3.0x and dividend coverage ratio of 1.3x also compare favorably to the rest of the group.

Inter Pipeline’s dividend coverage ratio is 1.2x, with a capital intensity of 78%, 6% below the group median of 84%. The company’s ROIC is 12.8%, while the IPL CN’s EBITDA margin is 53%.

While BWP has a debt-to-EBITDA of 5.2x, slightly higher than the group median of 4.9x, the company’s dividend coverage ratio is 1.8x, and Boardwalk has a capital intensity of just 56%, well below the group median of 84%. The company’s EBITDA margin of 55% is above the group median as well.

Data: Bloomberg, compiled by EnerCom Analytics

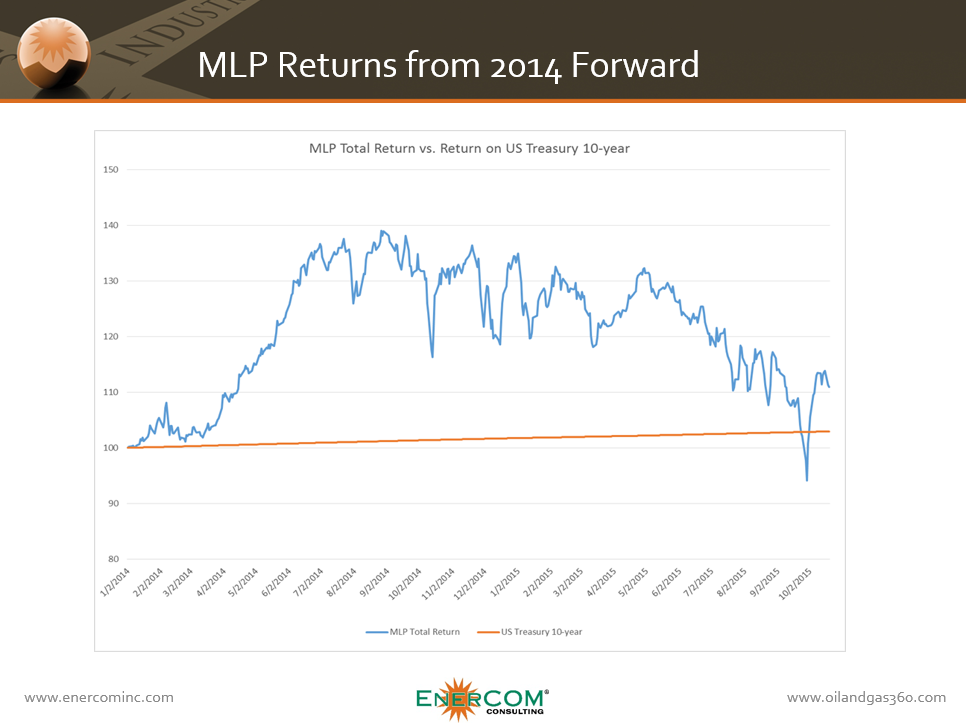

Timing Can Make or Break Returns in a Volatile Market

There is more to realizing high total returns from MLP investments than just investing in companies with strong fundamentals, however. Timing played a key role in the performance of the group’s total returns compared to 10-year Treasury bonds. Investing in the same group of four companies starting on the first day of 2014 rather than 2013 resulted in gains of just 10.97%, 40.9% less than if the investment had been made a year earlier.

Data: Bloomberg, compiled by EnerCom Analytics

It is interesting to note that IPL CN maintained distributions during the 2008 commodity cycle, while BWP and MMP both raised their distributions during the economic crisis. Commodities are a cyclical business, and these three names already have experience in dealing with lower price environments and surviving.

The return on 10-year Treasury bonds is also being kept at artificially low levels by Federal Reserve policy. Continued concerns over low inflation and weak job growth have kept the U.S. Federal Reserve at a standstill on raising rates. The last time the Fed raised interest rates was in June 2006. For a reality check, in 2006 Facebook was mainly for college students and had one-tenth the users of Myspace, according to the New York Times. Does anybody remember Myspace?

While the Fed waits for signs that the economy is growing at a more robust rate, in the October meeting, it once again delayed an interest hike on its benchmark rate, which will in effect keep rates on Treasuries at or near their current rates of return. The Fed did state that a December raise was still an option.

Is there a Right way to Own an MLP?

Shareholders in a corporation usually face being taxed on the company’s profits twice – once at the corporate level when the company pays the federal government at the corporate tax rate, and again at the personal level when those earnings that are paid out as dividends.

A publicly traded partnership must generate at least 90% of its gross income each year from qualifying activities. These include certain natural resource activities such as exploration, development, mining or production, processing, refining, transportation, or the marketing of any [depletable] mineral or natural resource. This is according to Section 7704(d)(1)(E) of the Internal Revenue Code.

The substantial tax benefits of an MLP can be lost in some circumstances, however. MLP mutual funds and exchange traded funds (ETFs) can negate the tax advantages of owning the partnership directly if they hold 25% or more of their assets in MLPs. Once a mutual fund, closed-end fund or ETF has 25% or more of its assets in MLPs they typically must put aside 35% of their income and unrealized gains as a “deferred tax liability,” largely canceling out the financial advantage of avoiding the corporate level taxes.

Popular ETFs like the Yorkville High Income MLP ETF (YMLP) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX) lose the tax benefit from MLPs since more than 25% of their assets are made up of MLPs. These kinds of funds do buffer some of the negative returns as well, leading the typical MLP fund to underperform the market on the way up, but outperform on the way down.

Owning units of an MLP directly does not offer the same buffer to losses that mutual funds and ETFs offer with a more diverse portfolio in exchange for the deferred tax liability.

Regulatory Issues

Questions about the regulation of MLPs have also caused some issues with the formation of new MLPs over the past year. The IRS put a pause on private letter rulings (PLRs) in April 2014, which acted as a kind of confirmation for companies about whether or not their businesses met the qualifying income standards to form MLPs.

After the IRS saw a spike in requests from 2011-2013, the agency decided to put a pause on all PLRs, which was lifted in May 2015. Under the proposed rules released after the pause from the IRS, qualifying activates for forming an MLP include the same activities as those set out in Section 7704(d)(1)(E) of the Internal Revenue Code, but also includes activities that are “intrinsic” to the operation of the MLP.

Experts who spoke with Oil & Gas 360® differed on whether or not the rule was good news. Managing Director at RW Baird & Co. Ethan Bellamy said the proposed ruling had requirements that made little sense. “The water rules, in particular, are illogical,” he said. “From a risk management standpoint, no MLP can afford to avoid spending time and resources trying to help the IRS clarify this guidance… The only thing [the proposed ruling] clarifies is that billable hours at law firms handling MLP qualification issues are headed up,” he told OAG360®.

Maria Halmo, director of research of Alerian, the company responsible for the Alerian MLP Index (AMZ), said that the rules “absolutely” offered clarity that was lacking when the IRS initiated the PLR pause in April. “Previously, the only guidance available was the law itself in combination with [PLRs]. As PLRs are specific to certain companies and often contained redacted sections, they can be difficult to interpret and generalize,” she said.

A similar corporate structure in Canada, called a specified investment flow-through (SIFT) trust income, was restructured in 2011 by legislation put in place in 2006 in such a way that it was no longer able to offer an MLP-like tax incentive to unitholders. Instead, the Canadian government began taxing SIFTs like corporations.

The Power of the Commodity Market

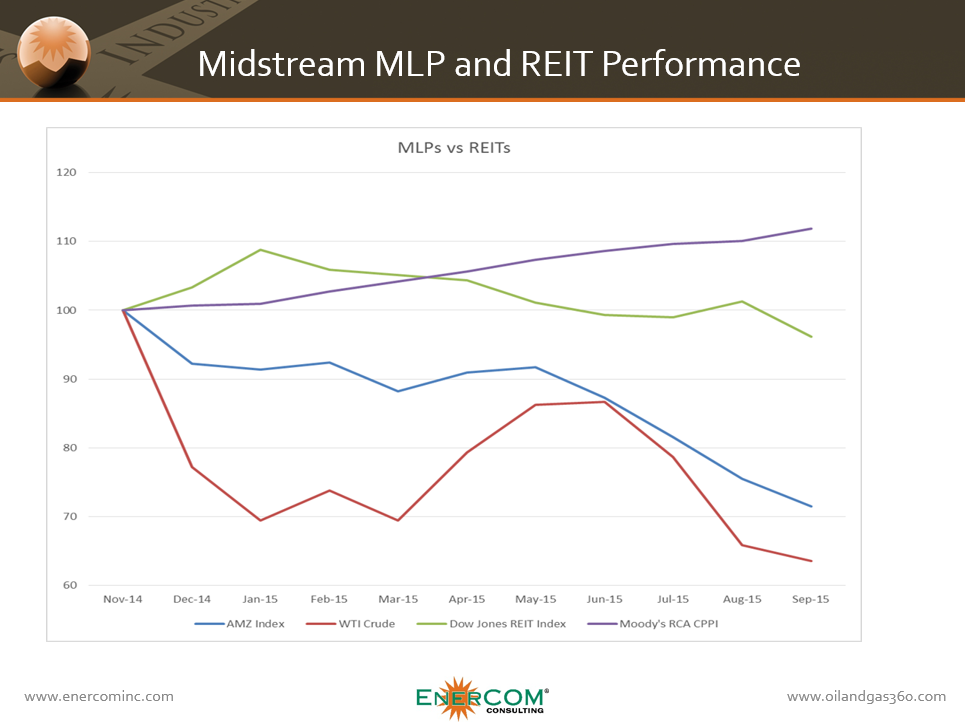

Despite the fact that midstream MLPs are often billed as being insulated from oil prices compared to other energy stocks, they could not escape the downturn. From November 2014 to September of this year, the Alerian MLP Index fell 29%, following a 36% decline in the price of WTI crude oil over the same period.

MLPs are a strongly commodity-driven structure. Looking at real estate investment trusts (REITs) which operate like mid-stream MLPs in that they offer a tax incentive to investors, the influence of a stronger underlying commodity driving the MLP market can be seen. In the case of REITs, the trust is usually fueled by the commercial real estate, as opposed to oil prices.

Data: Bloomberg, compiled by EnerCom Analytics

As illustrated in the graph above, the Alerian Index (of MLPs) has largely followed the price of oil since November of last year while the Dow Jones REIT Index has followed the commercial real estate market (illustrated by the Moody’s RCA Commercial Property Price Index).

The risk associated with MLPs is higher than some other forms of investments, but the dividends are generally higher too. Owning midstream MLPs directly, rather than through an ETF, can enhance the potential returns, but also leaves an investor more exposed to the downside risk. Like REITs, the performance of midstream MLPs is strongly influenced by the commodity it is tied to, even though the fee-based structure does offer some buffering from commodities volatility, in theory.

If and when the price of oil comes back in line with price levels before the OPEC 2014 Thanksgiving Day decision, the midstream MLPs will be brought along with the E&Ps and the oil service sector in a sustained recovery.

Are MLPs a Fad or is Western Civilization here to Stay?

They are probably here to stay as long as the tax structure remains unchanged, they are able to pay attractive rates of dividends, as long as demand for fossil fuels continues and the need for midstream infrastructure to process and transport hydrocarbons remains as robust as it is today.

Matter of fact, a group of U.S. senators wants to expand MLPs to include more than fossil fuel energy. In 2011/2012, U.S. Senator Christopher Coons (Delaware) introduced a bill called The Master Limited Partnerships Parity Act that aims to expand the adoption of the MLP structure to the renewable energy sector.

The Coons bill would change the law to allow wind and solar project developers, biomass and ethanol producers also take advantage of the MLP structure. In June 2015, Coons and other senators reintroduced the bill. If that bill becomes law, MLPs attached to wind and solar projects might be paying dividends long after global supplies of crude oil and natural gas come to an end.

Source: Office of U.S. Senator Christopher Coons

Editor’s Note: Western Civilization is still plugging along as of October 30, 2015.