CEO Kubik: An independent COS offers more upside to shareholders

(Editor’s note: all figures in Canadian dollars)

On December 1, 2015, Canadian Oil Sands (ticker: COS) issued a press release with an accompanying conference call detailing its 2016 budget and what it described as a “new era of lower cost operations.”

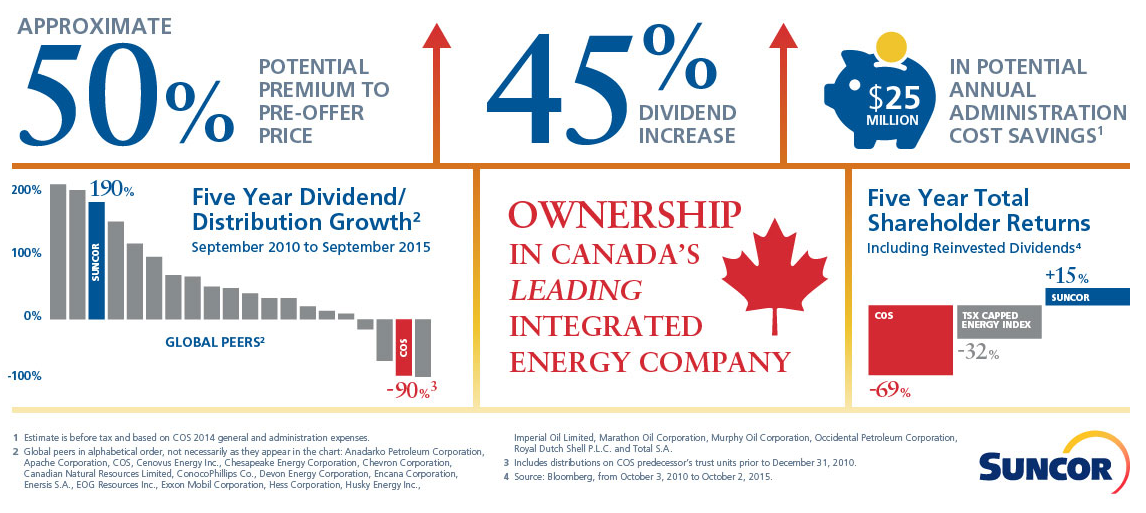

The timing comes as no coincidence, as Suncor’s $6.6 billion (including debt) hostile takeover bid is scheduled to expire at the end of the week. Suncor owns 12% of the Syncrude oil sands consortium project in Alberta, while Canadian Oil Sands (whose operations focus exclusively on the project) owns 37% interest – the most of the any of the seven companies. COS adopted a “poison pill” to fend off SU’s bid and has issued a handful of news releases criticizing what they feel to be a low-ball offer.

Suncor has sent letters to COS shareholders, and any visitors to its web site are greeted by a pop-up notification for more information on the potential COS buyout.

COS Defense Claims

In a nutshell, the management of Canadian Oil Sands said Suncor’s offer is undervalued because of:

- Increased cost efficiencies. All-in expenses are listed at $44.78/barrel, which gives COS enough cash flow to fully fund its dividend and capital expenditures if oil prices are at $45/barrel. At $50/barrel, COS generates $633 million in annual cash flow from operations, equating to $1.31 per share. According to the company, an additional $300 million in estimated cash flow is generated if oil prices increase to $60/barrel.

- Stable expenditure costs. As part of its near-term plan, COS has no large-scale projects in need of funding and expects to spend about $300 million annually for the next four years. The company is “prioritizing” on reducing its debt level to the lower end of its $1 to $2 billion range.

- Undeveloped leases, including one that was being actively marketed to Suncor prior to the takeover bid. COS Management said the SU offer “doesn’t recognize the value” of its undeveloped properties, which border existing projects.

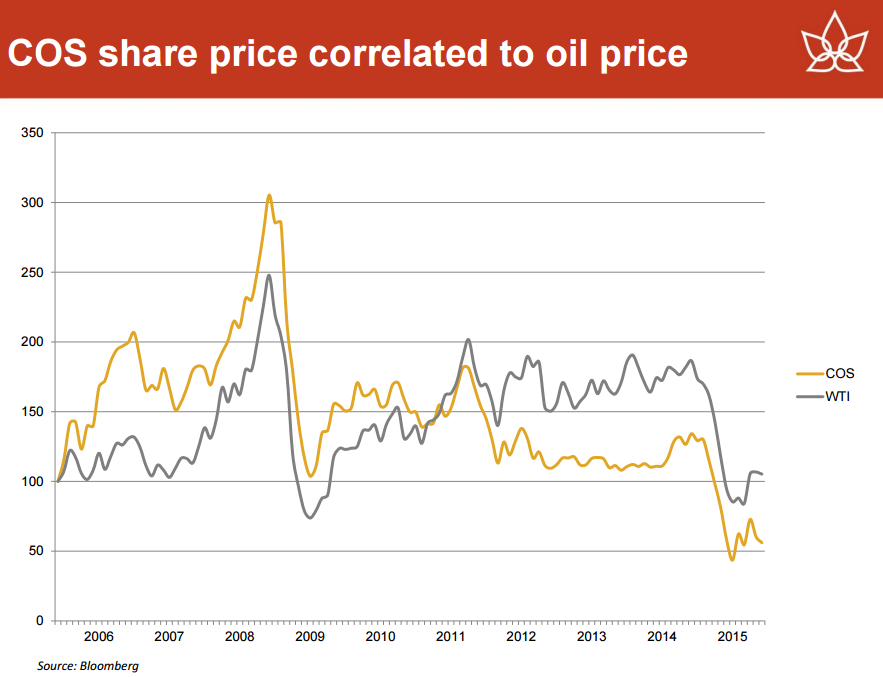

- COS and its link to commodity prices. COS shares historically have a 98% correlation with commodity prices, which COS management believes points to significant upside when oil prices recover. “We tend to move up twice as much as Suncor when those oil prices rise,” said Ryan Kubik, President and Chief Executive Officer of COS.

- Potential synergies realized by Suncor, stemming from becoming the largest interest holder in the project.

- Estimated operating costs of $37/barrel in 2016, which is below SU’s preliminary estimated operating costs of $38 to $45 per barrel.

While management refuted SU’s offer, they did, however, say they were “exploring alternatives that offer our shareholders full and fair value for assets.”

The Elephant in the Room

The outliers were not enough to deter criticism in the conference call. The latest offer follows a pitch that was made in April, which was above the latest official offer. In the midst of the commodity downturn, COS slashed its dividend by 85% to salvage some cash flow while Suncor has boosted its dividends by 23% over the last five years.

Kubik defended the decision to defy SU’s bid a second time, saying: “We were approached in the spring with a non-binding expression of interest. I won’t even call it a proposal. It was a letter that was brought to us, and it represented a discount to where Canadian Oil Sands shareholders could sell their shares in the market. So, you could have gone to the market and sold your shares at a price above what they were offering to buy the entire company at. So, clearly, there was no basis for further discussions. We did not hear from Suncor until they came back in October with this latest hostile offer.”

The correlation of COS shares with WTI prices have weighed more heavily on COS stock than Suncor, but Kubik and his fellow executives encouraged shareholders to think carefully in their merger decision. “Canadian Oil Sands shareholders will own less than 8% of the combined company, significantly diluting any upside for Canadian Oil Sands shareholders,” said Kubik, adding that SU shareholders would receive the benefits from COS’ groundwork. “Our shareholders know the value of the assets they own and they deserve full and fair value, not distressed value, for their irreplaceable assets.”

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.