Cabot continues beating estimates amid global glut

Many oil and gas companies are struggling to stay afloat as the global oil supply glut continues, pressuring crude oil prices near historic lows. More bankruptcies are expected to come in the next six months as bank redeterminations take their toll on companies with fewer reserves to use as collateral for their credit facilities.

Cabot Oil & Gas (ticker: COG, CabotOG.com) is not only weathering the storm, but also posting double-digit growth for a sixth consecutive year despite the current commodity market.

As spring borrowing redeterminations loom around the corner, 79% of borrowers expected to see their borrowing bases decreased by 38%, on average. The price deck at which companies determine their reserves decreased 48% in 2016, meaning most companies have fewer proved reserves to lend against, and potentially seeing some companies going bankrupt in the near future as banks lower the money available to companies. In North Dakota alone, the Director of the Department of Mineral Resources Lynn Helms anticipates five or six companies to announce bankruptcy following bank redeterminations.

Despite the cloudy outlook for the wider industry, Cabot has managed to continue growing its reserves. In the company’s fourth quarter and year-end release, COG announced that its 2015 year-end proved reserves increased by 11% to 8.2 Tcfe.

Low debt and strong assets

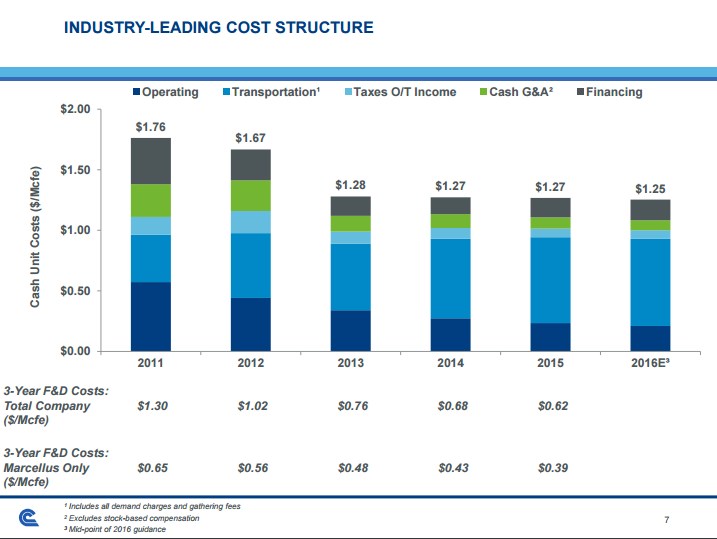

In addition to posting an 11% increase in its reserves, Cabot has a strong balance sheet, continuing to set the company apart in the current market. According to the company’s release, COG currently holds $2.0 billion in debt, with $20 million due in 2016 and $312 million due in 2018. The amount outstanding on the company’s revolver – currently $413 million – along with an additional $100 million will be due in 2020.

Cabot’s debt metrics compare very favorably to other E&Ps in EnerCom’s E&P Weekly. COG’s debt-to-market cap is just 25%, compared to a group median of 165%, with a net debt-to-TTM EBITDA ratio of just 2.1x, compared to 2.9x median for the wider group. Cabot has also focused on low-cost asset base, which has allowed it to keep its asset intensity at just 47% compared to a group median of 103%.

COG’s production is 96% gas-weighted with fourth-quarter and full-year production coming in at 151.0 Bcfe and 602.5 Bcfe, respectively. Cabot said its production remained “roughly flat” from third-quarter, but that the full-year results represented at 13% increase over 2014.

Cabot downspacing Marcellus wells ups location count and EURs

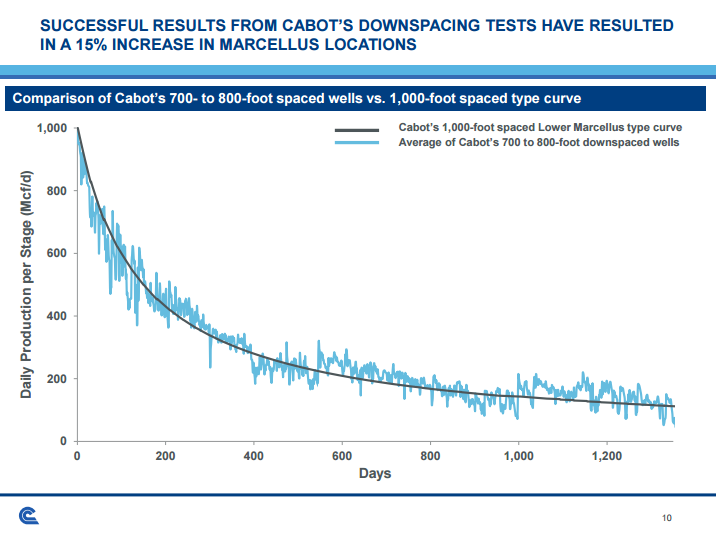

In the company’s press release today, COG also announced that it has improved EURs and increased its location count by downspacing its laterals in the Marcellus. Cabot has decreased the spacing on its laterals from 1,000 feet to 700-800 feet, resulting in an increase in location count from approximately 3,000 to 3,450. COG also said that the EUR per 1,000 lateral feet for its Lower Marcellus wells increased 6% to 3.8 Bcf, implying an EUR increase to 22 Bcf from 18 Bcf per well, according to analysts at UBS.

Along with the increased recovery on its wells, Cabot said it was able to lower its F&D costs in the Marcellus 7% to $0.31 per Mcf, mirroring the company-wide 7% decline in F&D costs.

Production expected to increase with one-rig program in 2016

The company did not update its 2016 guidance from its previous release, leaving its capex budget at $325 million for the year, down about 58% from last year. Roughly 70% of the company’s budget will go towards drilling and completions in the Marcellus as COG continues targeting its low-cost, high-EUR gas assets.

Cabot reduced its company-wide rig count to just one well, which is running in the Marcellus, with plans to drill/complete 25/40 wells in the play. The company said that it is targeting 2%-7% production growth in 2016, meaning this year could potentially break the chain in Cabot’s typically double-digit growth.

The company also has about 15% of 2016 production hedged. “The company has natural gas swap positions and approximately 194 mmcpfd hedged at $2.25 (price index is NYMEX) for the second and third quarters,” said a note from Barclays today. “COG has roughly 49 mmcfpd hedged at $2.35 (pricing index is TCO) for the second and third quarters,” as well.

A pipeline update

According to the company’s press release, COG plans to spend $80-$150 million in 2016 on its Constitution and Atlantic Sunrise Pipelines. During Cabot’s earnings call today, company Chairman, President and CEO Dan Dinges said the process of clearing trees for the Constitution was underway in Pennsylvania, but still awaiting approval in New York.

“As of today, approximately 60% of the trees in Pennsylvania on the Constitution right-of-way are down,” said Dinges. Additionally, “[The FERC] thoroughly considered and firmly rejected all arguments and ultimately declined all requests for rehearing [regarding FERC approval], another positive step for Constitution.”

The 124-mile pipeline is expected to transport 650,000 dekatherms of natural gas per day, according to the partners involved in the project.

Dinges went on to say that the Atlantic Sunrise project, which will transport 850,000 dekatherms to the mid-Atlantic, remains on schedule with initial pipe shipments already on location and the draft environmental impact statement expected to shortly from the FERC.