Concerned Shareholders of Eagle Energy Inc. Set the Record Straight

Calgary, Alberta--(Newsfile Corp. - May 29, 2017) - Daniel Gundersen and Kingsway Financial Services Inc. (together, the "Concerned Shareholders") announce today that their information circular (the "Circular") and BLUE form of proxy have been mailed to all shareholders of Eagle Energy Inc. ("Eagle" or the "Company"; TSX: EGL) in connection with Eagle's annual general meeting scheduled to be held at 10:00 a.m. (Calgary time) on Tuesday, June 27, 2017 (the "Meeting"). A copy of the Circular is available on SEDAR under Eagle's profile and at our website www.SaveEagle.ca.

The Concerned Shareholders urge Eagle shareholders to vote for change by voting FOR the Concerned Shareholder nominees on the BLUE form of proxy or voting instruction form in accordance with the instructions set out in the Concerned Shareholders' meeting materials.

In addition, the Concerned Shareholders have also issued today the following letter to Eagle shareholders:

May 29, 2017

Dear Fellow Shareholders,

You have or will soon receive an information circular from the current management of Eagle Energy Inc. ("Eagle" or the "Company"). We have just read it. IT IS AN INSULT TO ALL SHAREHOLDERS. Eagle's management wants you to believe that we are behind a hostile takeover with inexperienced oil & gas personnel and a financial partner with questionable motives and, if that were not enough, management has told you that if they lose, an immediate event of default will be triggered and the future of the Company will be at risk. These are lies made up by a management group desperate to pursue its high-risk business plan in an attempt to justify its excessive overhead levels so that Eagle can continue to pay exorbitant salaries to management. It's that simple.

Eagle is attacking us and making baseless allegations about our motives in an attempt to mislead the shareholders of the Company. Instead, Eagle should have answered the following important questions:

1. | Why is the stock down over 70% since 2015? |

2. | Why was the dividend cancelled in March 2017? |

3. | Why did CEO Richard Clark receive compensation of $778,646 in 2016? |

4. | What will management do to fix Eagle's unsustainable cost structure? |

5. | What will management do to fix Eagle's debt problems? |

6. | Why has Eagle been abandoned by the investment community? |

7. | Who approved the recent increase in severance payments to management? |

8. | Who approved directors and management receiving approximately 4% of Eagle for free? |

The existing board and management have betrayed the shareholders of Eagle.

We, Daniel Gundersen and Kingsway Financial Services Inc. ("Kingsway"), are Concerned Shareholders of Eagle Energy Inc. WE HAVE ONLY ONE MOTIVE AND ONE OBJECTIVE: MAXIMIZE SHAREHOLDER VALUE. We have no ulterior motives and no hidden agenda. We believe that the Company needs a plan that will benefit ALL shareholders, not just current management. We have that plan and we have the right people to execute it.

Eagle has high quality assets, but it also has three serious problems:

- Failed leadership

- Excessive overhead costs including management salaries

- Expensive and onerous debt

Failed Leadership

On March 17, 2017, the last brokerage firm in Calgary that is providing research coverage on Eagle wrote that it was concerned about "management's lack of alignment with shareholder interests". This is the consensus in the Calgary investment community. There is no trust. CEO Richard Clark, a former lawyer, is believed to have lost focus on Eagle and is pursuing other interests. However, this did not prevent him from receiving total compensation of $778,646 in 2016. We remind you that Eagle's market capitalization is less than $25 million. This is madness.

We also question the existing board's justification and authority for dramatically increased severance and other payments if there is a change of control. In 2015, the aggregate payments were $2.2 million. Eagle's current information circular indicates that change of control payments would now total $4.0 million. This number is excessive relative to Eagle's current market capitalization of less than $25 million. This is an absolute affront to shareholders. Eagle is completely out of touch with reasonable corporate governance practices. This is not acceptable.

Our director nominees offer leadership that will be wholly aligned with shareholders. It is a group that will terminate the practice of excessive management compensation. Our director nominees will be stewards of good governance and will hold management as well as themselves accountable.

Excessive Overhead Costs Including Management Salaries and Free Shares

Eagle's overhead costs including management salaries are triple those of comparable companies. This level of costs is unsustainable. The same brokerage firm that was worried about shareholder alignment wrote that they "struggle with EGL's cost structure". In its current information circular, management fails to even acknowledge this problem. We believe Eagle's plan is designed to justify these excessive overhead costs. This is a prescription for failure. This is not acceptable.

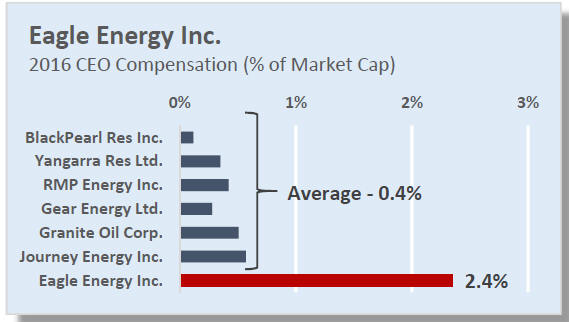

From Y/E public filings & December 31, 2016 closing share prices.

Eagle Energy Inc. CEO Compensation Comparison Table

To view an enhanced version of this graphic, please visit:

http://orders.newsfilecorp.com/files/5280/27039_eagle2.jpg

CEO Richard Clark's 2016 compensation of $778,646 is a significant part and representative of Eagle's cost problems. The chart to the left illustrates his compensation as a percentage of Eagle's market capitalization. Shockingly, on this basis, his compensation is six times the average of other CEOs at comparable companies.

This is not acceptable.

The existing board granted 1.66 million shares (in the form of Restricted Share Units and Performance Share Units) to the management group and themselves in 2016. To put that in perspective, Eagle's board gave themselves and management the equivalent of approximately 4% of the company — for free — while YOU, the true owners of Eagle, suffered losses. This is not acceptable.

Expensive and Onerous Debt

In its information circular, management continues to highlight its satisfaction with the White Oak term loan. We find it shocking that any company could be satisfied with a debt that is three times its market capitalization and with interest rates that are more than double those of a conventional bank facility. Management describes the benefit of a 4 year loan, but not surprisingly fails to mention that after only one month, the financial covenants contained in the agreement were amended without explanation to shareholders, leaving us to conclude there were in fact, serious concerns about a potential breach. Management states that "The covenants under the new loan are not materially different than they were under the old loan." However, they fail to acknowledge that interest payments under the new loan will nearly triple to about $7 million annually. The loss of this cash flow affects the covenants significantly. We are worried that the financial covenants within the loan agreement may become problematic as soon as August 2017. This is not acceptable.

We are shocked that Eagle is hiding behind a standard financial covenant in the White Oak loan agreement as a reason to entrench the current board. Citing this change of control covenant as a reason to discourage shareholders from supporting our director nominees is completely irresponsible and evidence of Eagle's failed leadership. We have carefully reviewed the loan agreement, including the change of control definition, with our legal counsel. We would expect that, in the event that the Concerned Shareholder director nominees are successful, the current Eagle board would work cooperatively with us to ensure a smooth transition that would result in ongoing compliance with the loan agreement. However, in the event the current Eagle board disregards its fiduciary responsibilities, we have numerous options available to us to effectively manage the White Oak term loan. Citing the change of control provision in its information circular is simply fear mongering by Eagle and is only evidence of their desperation. This is not acceptable.

Concerned Shareholders' Plan

On March 4, the Concerned Shareholders announced a plan that will fix Eagle's overhead and debt problems. Our plan is intended to fix problems in the short term and maximize value in the long term. This long-term objective cannot be accomplished if Eagle has an unsustainable overhead burden and a crushing level of expensive debt. The oil & gas business today requires efficiency in all aspects of the business, especially cost structure.

Unlike Eagle's plan, our plan will fix Eagle's overhead and debt problems. In order to achieve this critical objective, assets will have to be sold, but certainly not at fire sale prices as suggested in Eagle's information circular. Eagle has high quality assets. We have been in contact with the most reputable acquisition and divestiture firms in Canada and the US. We believe any one of Eagle's main assets could be sold for a premium to Ea gle's current corporate valuation.

Once Eagle's overhead and debt problems are fixed, the new board will quickly focus on the long-term. No alternative will be ignored. A more efficient cost structure and a repaired balance sheet will support both organic growth and corporate development. It may be possible to achieve the most value by merging with another company. Any cost savings achieved by efficiency gains and cheaper access to capital would effectively flow to shareholders in this scenario. Daniel Gundersen and the new board will be agents of positive change for shareholders. OUR PLAN IS A LOW-RISK PLAN THAT IS IN THE BEST INTERESTS OF ALL EAGLE SHAREHOLDERS. IT IS A PLAN DEVELOPED TO MAXIMIZE SHAREHOLDER VALUE.

Concerned Shareholders' Board Nominees

Contrary to the claims made by Eagle management, our board nominees are highly qualified. Dan Gundersen, Gerry Gilewicz and Brad Porter have significant oil & gas experience, including the management, operation, and acquisition and divestiture of assets in Canada and the United States. Rob Fong has significant financial, regulatory and governance experience with public oil & gas companies in Canada. As a group, they are committed to shareholders. They are also a more conservative group. Unlike Eagle's current board that is comfortable with a highly-leveraged company reliant on a high-risk drilling program, this group believes a low risk plan to sell assets, reduce overhead and pay down debt is the right plan. Remember, David Fitzpatrick and Warren Steckley have histories of involvement with companies that have undergone bankruptcies and formal insolvencies (see page 10 of Eagle's information circular). We have no such appetite for risk. It is not in the best interests of shareholders.

Concerned Shareholders' Motives

Eagle's information circular wrongly questions the experience, talent, and motives of the Concerned Shareholders. Regarding Daniel Gundersen, we highlight director nominee Bradley Porter's recent comments: "Having worked directly with Mr. Gundersen as management for three successful publicly-traded oil & gas exploration and production companies in the period of 2002 through 2010, I can personally vouch for his integrity, competence, and work ethic. All shareholders will be well-served and reap the benefit of his dedication." Eagle has described Mr. Gundersen as an opportunist. This is absurd. In early 2016, Mr. Gundersen and his fellow Maple Leaf Royalties Corp. shareholders received 7.7 million Eagle shares. These shares have since lost substantial value. Mr. Gundersen has every right to be a very disappointed and a very concerned shareholder of Eagle.

Kingsway is a publicly listed merchant bank with offices in Toronto and Itasca, Illinois. The market capitalization of Kingsway is approximately $200 million. Its shares are listed on the TSX and NYSE under the symbol KFS. Larry Swets is the Chief Executive Officer and owns 9% of Kingsway. Before joining Kingsway, Mr. Swets founded Itasca Financial LLC, an advisory and investment firm specializing in the insurance industry. He is a Chartered Financial Analyst (CFA) charterholder.

Kingsway is a value investor in the tradition of Benjamin Graham. It strongly believes that the best investments arise at the extremes of market cycles. Because of low oil prices, Kingsway has identified energy as a very positive investment opportunity. In early 2016, it acquired certain oil & gas operating assets in Texas. In late 2016, Mr. Swets was introduced to Mr. Gundersen and his opinions regarding the potential of Eagle. Kingsway later made its initial investment in Eagle and could increase that investment if it had confidence in the direction of the Company.

Eagle has described Kingsway as a short-term investor. This is an incorrect and misleading conclusion. Larry Swets' 2016 letter to Kingsway shareholders highlights this issue. He wrote, "Kingsway focuses on building long-term value by compounding capital with investments/acquisition/financings that offer asymmetric risk/reward potential with a margin of safety supported by private market values using a merchant banking approach".

Eagle has said Kingsway has suspect motives. Like Benjamin Graham, Kingsway is also an investor that will not tolerate mismanagement or a lack of shareholder alignment. Kingsway does not back down from this. It is proud of this fact. After ignoring its shareholders for years, it must be difficult for existing Eagle management to accept a shareholder demand for competent management, shareholder alignment, and reasonable governance practices.

The Proxy to Vote is BLUE

Time is of the essence. Your Company is at a crucial juncture and your vote is important, regardless of how many shares you own.

We urge you to save your investment and vote for change by voting FOR the Concerned Shareholder nominees on the BLUE Proxy today. Ensure that your vote is FOR Daniel Gundersen, Robert Fong, Gerald Gilewicz, and Bradley Porter.

Voting is a quick and simple process. Your BLUE proxy must be received well in advance of the deadline of 9:00 a.m. (Calgary time) on June 23, 2017. Due to the limited time available, we recommend voting by internet, telephone or fax today or no later than 24 hours before the deadline. Visit our website www.SaveEagle.ca where you can vote. Shareholders with questions or who require any assistance in executing their proxy or voting instruction form, please call D.F. King Canada at: North American Toll Free Number: 1-800-398-2816 Outside North America, Banks, Brokers and Collect Calls: 1-201-806-7301. Email: inquiries@dfking.com

Your vote is extremely important. Every share counts to ensure change is implemented to save your Company. Eagle shareholders should disregard any materials received from management and vote only the BLUE proxy today.

Sincerely,

Signed "Daniel Gundersen"

Concerned Shareholder

Signed "Larry Swets"

CEO, Kingsway Financial Services Inc.

Concerned Shareholder

Contacts

Daniel Gundersen

403-852-4423

dan@SaveEagle.ca

Larry G. Swets Jr.

630-290-2432

Jack Muir

jackmuir@cogencygroup.ca

604-836-8782

DF King

1-800-398-2816 (toll free within North America)

Email: inquiries@dfking.com

The Concerned Shareholders have hired Norton Rose Fulbright Canada LLP as their legal counsel, Cogency Group Partners Inc. as their financial advisor and D.F. King as its proxy advisor and proxy solicitation agent.

ADDITIONAL INFORMATION

The Concerned Shareholders have filed the Circular containing the information required by Form 51-102F5 — Information Circular in respect of the nominees of the Concerned Shareholders, which is available on Eagle's profile on SEDAR at www.sedar.com.

This solicitation is being made by the Concerned Shareholders, and not by or on behalf of the management of Eagle. Solicitations may be made by or on behalf of the Concerned Shareholders, by mail, telephone, fax, email or other electronic means, and in person by directors, officers and employees of the Concerned Shareholders or their proxy advisor D.F. King or by the nominees of the Concerned Shareholders. All costs incurred for any solicitation will be borne by the Concerned Shareholders, provided that, subject to applicable law, the Concerned Shareholders may seek reimbursement from Eagle of the Concerned Shareholders' out-of-pocket expenses, including proxy solicitation expenses and legal fees, incurred in connection with a successful reconstitution of the board of directors. Pursuant to the agreement with D.F. King, for its solicitation services, D.F.King would receive approximately $170,000 plus standard per call fees and out of pocket disbursements.

If you are the registered holder of your Common Shares, you may revoke a proxy previously given: (a) by completing and signing a valid form of proxy bearing a later date and returning it in accordance with the instructions contained in the accompanying BLUE form of proxy or as otherwise provided in the Circular; (b) by depositing an instrument in writing executed by a registered holder of Common Shares or by a registered holder's attorney authorized in writing (or, if the registered holder of Common Shares is a corporation, by a duly authorized officer or attorney) and deposited either at the principal business office of the Eagle (2710, 500 - 4th Avenue S.W., Calgary, Alberta T2P 2V6) at any time up to and including 5:00 p.m. (Calgary Time) on the last business day preceding the day of the Meeting; (c) by attending the Meeting and reporting to the desk of Computershare Investor Services Inc. to sign in and revoke any proxy previously given; or (d) in any other manner permitted by law.

Eagle's principal business office is 2710, 500 - 4th Avenue S.W., Calgary, Alberta T2P 2V6. A copy of this press release may be obtained on Eagle's SEDAR profile at www.sedar.com.

copyright (c) newsfile corp. 2017

{kind=link}