360 News Wire

Third-quarter value soars to $21 billion as E&Ps eye further consolidation

Austin, Texas (October 5, 2020) – Enverus, the leading oil and gas SaaS and data analytics company, is releasing its summary of 3Q20 U.S. upstream M&A. While the third quarter’s tempo of 28 deals with a disclosed value is tied with 1Q20 for the worst showing in 10 years, a couple of big corporate acquisitions pushed total transaction value to $21 billion. That is a strong quarterly deal total by historical standards.

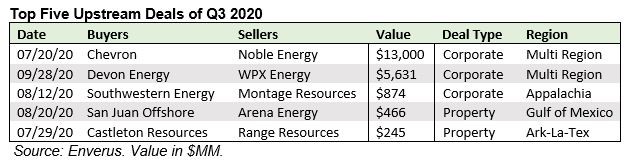

The largest deal of the third quarter was Chevron’s $13 billion acquisition of Noble Energy, which targeted assets in the DJ and Permian basins, as well as Eastern Mediterranean gas production. While a fraction of the cost of Chevron’s attempted Anadarko acquisition last year, its purchase of Noble is still tied for the fourth largest global upstream deal since 2014.

The largest pure U.S. shale consolidation move came at the end of the quarter, when Devon Energy and WPX Energy announced a merger that creates a combined company with a $12 billion enterprise value and a concentration in the Delaware Basin. Both Chevron’s acquisition of Noble, and Devon’s merger with WPX, are structured with little premium and all-stock consideration.

“There is a broad consensus that consolidation is a net positive for the industry,” commented Enverus Senior M&A Analyst Andrew Dittmar. “Including the corporate deals from 2019, that process looks to be well underway. There is room for further mergers, but it can be a challenge to find the right asset and balance sheet fits for accretive deals. It may take several more years for consolidation to play out.”

With a deep roster of economic well locations, the Permian Basin is likely to be the epicenter of shale consolidation. However, companies focused on other regions will also benefit from repositioning into fewer, larger producers. There was some modest consolidation in Appalachia recently with Southwestern acquiring Montage Resources for $874 million. Like the deals listed above, that transaction is also structured with little premium and all-stock consideration.

“Regardless of the targeted play, mergers have so far focused on companies with reasonable debt loads,” added Dittmar. “Companies with impaired balance sheets are being left to find their own way, resulting in a spate of Chapter 11 filings.”

During the third quarter, notable Chapter 11 filings included California Resources Corp. ($5.2 billion in debt), Oasis Petroleum ($2.8 billion in debt), and Denbury Resources ($2.5 billion in debt). Nearly all public companies filing Chapter 11 are pursuing a reorganization, while a substantial number of private E&Ps that file Chapter 11 are choosing to exit via sales. The list of selling private companies includes Gulf of Mexico producer Arena Energy ($466 million sale) and Midcontinent-focused Templar Energy ($91 million sale).

For the remainder of 2020, there is the potential for additional corporate deals; however, the market for asset deals is likely to remain sluggish. Gas plays seem poised to draw more attention for asset acquisitions than their oilier counterparts as there is more optimism around the outlook for gas pricing.

A pickup in deal flow likely requires an uplift in commodity prices that boosts cash flow for existing participants, plus an inflow of new capital. Often private equity has deployed capital during down markets but looks less willing to step in currently. One potential source of capital are Special Purpose Acquisitions Companies or SPACs. This model has been used before in oil and gas, most recently by Pure Acquisition Corp. which completed its previously announced deal during 3Q20 to form HighPeak Energy. SPACs currently seem to be gaining broader acceptance in the investment community with rising use across industries.

Members of the media can contact Jon Haubert to request a copy of the full report or to schedule an interview with one of Enverus’ expert analysts.