OPEC Cuts Demand Forecast

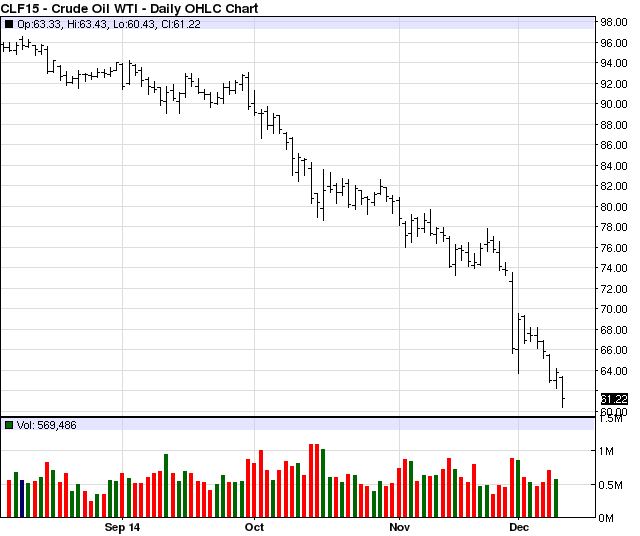

OPEC cut demand forecast for its crude oil to a 12-year low, sending oil prices, energy shares and the overall stock market into a dive on Wednesday. West Texas Intermediate (WTI) traded at a day low of $60.43. On top of the OPEC demand cut, U.S. inventories increased on a day when expectations were for a decrease. The TSX fell 342.78 with energy stocks leading the crush. The Dow Jones Industrials, which has been flirting with 18,000, dropped 268 on Wednesday.

OPEC reduced its projection for 2015 by about 300,000 barrels a day to 28.9 million in its monthly report today, Bloomberg reported. Inventories of U.S. crude oil rose to the highest seasonal level in weekly data that started in 1982, the Energy Information Administration reported.

“We are still searching for the bottom, and may not find it until OPEC changes policy or low prices begin to eat into production,” Eugen Weinberg, head of commodities research at Commerzbank AG, told Bloomberg.

Saudi oil minister Ali Al Naimi told reporters at a UN global warming conference, “Why should I cut production?” A number of analysts believe Saudi is testing the sustainability of the U.S. shale boom by not being willing to cut its production, even under pressure from fellow OPEC members. “They are willing to let this thing crash and see what it does to U.S. shale producers,” one analyst said about the Saudi minister’s statement. Many traders and energy analysts have expressed similar sentiment in recent weeks, saying OPEC has lost its power, with Saudi calling the shots.

In spite of falling prices, U.S. oil output is forecast at the highest level since 1972, EIA Administrator Adam Sieminski said in a statement.

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.