By Tim Rezvan-EnerCom, Inc.

3Q earnings season is about to begin for the E&Ps, with large cap diversified operator Hess (NYSE: HES) and mid cap Permian pure play Matador (NYSE: MTDR) both on the docket for next week with calls on Wed 10/27.

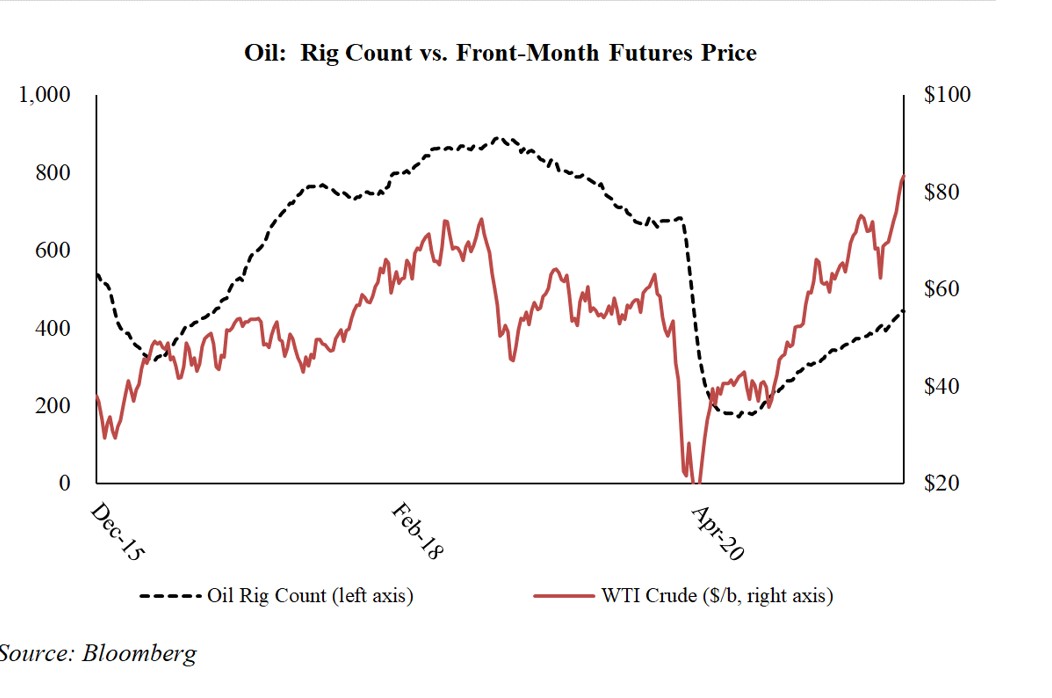

Heading into earnings, commodity prices remain a much-appreciated tailwind to fund balance sheet healing and capital return initiatives. But service cost inflation looms as a big 2022 headwind, especially as the oil rig count continues to climb. The big three OFS players – Baker Hughes (NYSE: BKR), Halliburton (NYSE: HAL) and Schlumberger (NYSE: SLB) – all mentioned efforts to increase prices for upstream services in their earnings calls this week. We all expect the correlation between commodity prices and service costs to hold, but how high and how pervasive will that R-squared be?

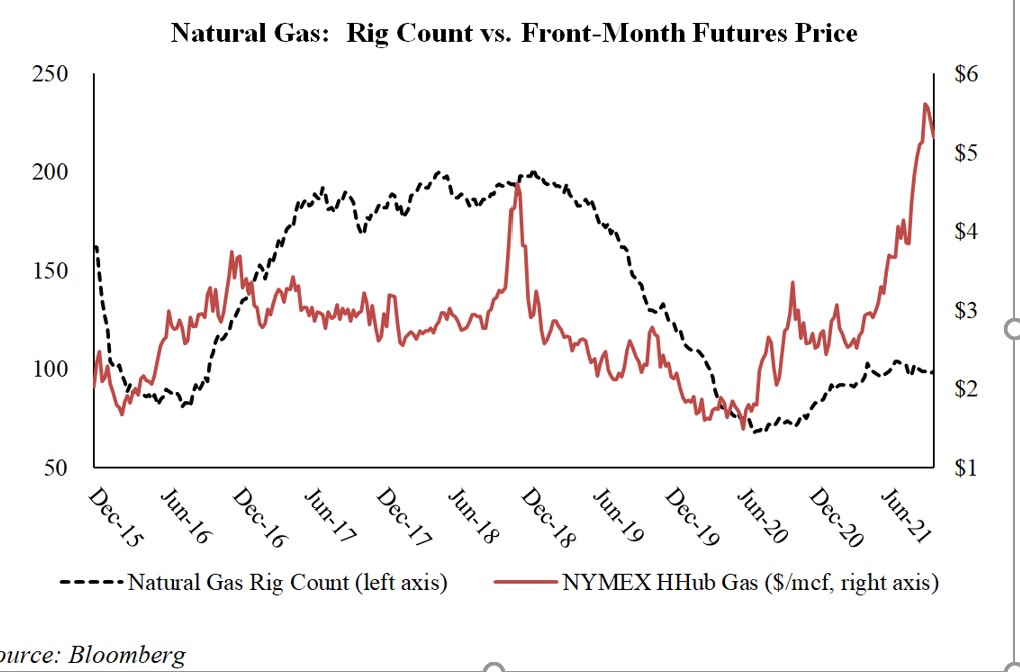

Breaking down the increase in oil rig count. The natural gas rig count has been remarkably flat since the end of 2Q21 (range of 98-104 rigs). Operators have shown tremendous restraint, reflecting: i) their view on the fragility of the rally, and ii) limited upside to CF generation from highly hedged production streams. But the oil rig count has increased 19% (+71) to 443 over that time. Almost half of that increase has come from the Permian (+31 to 267), with the rest being spread across the Eagle Ford (+7 to 38), Williston (+6 to 23), Cana Woodford (+5 to 22) and other basins.

The oil rig increase – it’s about excess cash flow, not lost capital discipline. We at EnerCom are firmly not in the camp that the increase in rigs shows waning capital discipline in the industry. We believe that activity increases on the margin reflect the windfall in cash flows from unhedged production, not a return of last decade’s irrational exuberance. In 2H21, WTI has averaged $72.50/b and Henry Hub has averaged $4.45/mcf (bid-week pricing to date), a far cry from the $45/$3 price deck used to underwrite 2021 budgets. We point to operators like Magnolia (NYSE: MGY), who were able to increase activity and still stay within their “capex to equal ~60% of EBITDA” mantra, due to an unhedged production stream.

Cost inflation – what to make of the chatter? Anecdotal chatter with operators suggests that inflation is real, but we are hearing widely disparate views on the severity. Operators in shale areas outside of the Permian Basin highlighted more stable work forces, mitigating the largest potential driver of inflation, as well as a desire to maintain current levels of activity and continue to generate FCF. And most of these steady-state operators have seasoned procurement teams with supply chain time horizons extending out up to two years, offsetting spot pricing increases. These areas did not “boom” like the Permian did since 2016, so they did not have as much of a “bust,” in terms of a skilled labor exodus.

Will Permian be more acutely impacted? The incremental rig additions into the Permian (267 rigs today, +92 YTD, +31 in 2H21) bring the basin’s rig count back to an 18-month high. We expect the ramp to strain existing headcount and equipment limitations. As such, we will listen intently for Permian operators’ comments on the topic of service cost inflation. We await comments from Conoco (earnings call on 11/2), Diamondback (11/2), Pioneer (11/4) and Occidental (11/5) to get the large cap view. In addition to Matador, we will look for comments from Laredo Petroleum (11/3), Callon (11/4) and Centennial (TBD) to get the small/mid cap Permian pure play view.

Other topics to listen for this quarter:

- Efficiencies: Same story, different quarter. Operators continue to find ways to drill and complete horizontal wells more efficiently, especially with activity concentrated in well understood core areas with existing infrastructure. Most E&Ps have left 2021 drilling plans relatively unchanged, despite stronger pricing. We hope to understand how changes in 2022 activity could aid or inhibit the ability of efficiency to offset service cost inflation.

- Hedge losses: There will be blood. Lots of it. But it is an output of the commodity price recovery. And smaller operators with weaker balance sheets were forced into robust hedge positions from lending banks. But there will be companies who outperform/underperform peers, in terms of hedge impact. It will be an opportunity for some management teams to flex and highlight the relative attractiveness of their hedge books.

- Borrowing base redeterminations: We have already seen some material increases to borrowing bases being announced. The resurgent strip, along with organic FCF generation across the industry, is improving liquidity. Increases in bank lines could be a precursor to another round of high yield debt issuances, as companies seek to get refinancings done ahead of a subsequent move up in rates.

Balance sheet improvement will vary across companies: Many of the highly levered names are substantially hedged at prices well below the strip. Don’t be surprised to see balance sheets of levered names show less organic improvement than less leveraged peers.

Tim Rezvan, CFA is a Director at the energy consulting firm EnerCom, Inc. He has experience in sell-side equity research, asset management, corporate strategy, investor relations and ESG. Mr. Rezvan’s sell-side equity research experience in the E&P industry focused on leverage trends, full-cycle costs, emerging unconventional resource plays, M&A analysis and corporate governance.

EnerCom, Inc. is the energy industry’s leading communication experts. We can help you with corporate strategy, ESG, media and government and stakeholder relations to effectively communicate your company’s story. Contact: services@enercominc.com

[contextly_sidebar id=”XImfb0mrrJOq0eyxk3mkg8iCZxsye6rR”]