On June 2, 2014, the Environmental Protection Agency (EPA) moved to the second phase of its Clean Power Plan. According to the EPA, the Plan “cuts carbon pollution from existing power plants, the single largest source of carbon pollution in the United States. Today’s proposal will protect public health, move the United States toward a cleaner environment and fight climate change while supplying Americans with reliable and affordable power.”

The Plan, which calls for emissions to drop by 30% by 2030, marks the first time such an effort has occurred. As part of the ongoing process, the EPA will hold four public hearings in Denver, Atlanta, Washington, DC and Pittsburgh beginning July 28, 2014.

The United States Chamber of Commerce said the potential regulations would result in a “very slight” reduction in carbon emissions which would be overcome by global increases. Some scientists have said developed countries need to cut 80% of emissions by 2050 in order to slow climate change. In addition, research from the Chamber shows rises in electricity costs and a negative impact on the economy. “The cumulative impact to the economy could be $859 billion by 2030 (an average of over $50 billion every year),” the report reads.

Who Loses?

Coal. Despite accounting for 37% of all energy use in the United States, coal also consists of 75% of all CO2 emissions. The EPA estimates coal’s market share will drop to 30% of energy needs by 2030. By that time, natural gas is expected to have pulled even and account for 30% of energy use. By 2025, the estimated average age of coal power plants will be 49 years.

Kevin Crutchfield, CEO of Alpha Natural Resources, says modern technology simply cannot meet the standards set forth by the EPA. Emissions from new coal plants are not to exceed 1,100 lbs. of carbon monoxide per megawatt-hour (MWH), even though advanced coal facilities currently produce 1,800 lbs. of carbon monoxide per MWH.

Gas-fired plants are held to a higher standard due to its cleaner-burning resources. Gas plant emissions will be capped at 1,000 lbs. per MWH and the EPA reports current plants emit roughly 1,130 lbs per MWH – approximately half of the average coal-fired plant. On June 6, 2014, a gas plant in California reported emissions at 617 lbs. /MWH and completed the project several months ahead of the deadline. Combined-cycle gas plants are already in the 800 lb. range.

New coal plants will now be more expensive to develop. At least 100 coal-fired plants are scheduled to be shut down. The amount of coal-fired electricity the U.S. produces as a share of total generation is at its lowest level since the early 1970s.

“One of the reasons no one is building coal plants in the U.S. is that it’s too expensive,” said John Coequyt, director of the international climate program at the Sierra Club. “It’s also true that in developing countries, when you add that the international market for coal fluctuates a lot, that electricity from coal is very expensive even without pollution-control equipment.”

What about Natural Gas?

A nine-state project called the Regional Greenhouse Gas Initiative has depended on natural gas to cut back emissions, and the results are apparent. Four of the states (Maine, Massachusetts, New Hampshire and New York) slashed emissions by more than 40% from 2005 to 2012, and Maryland cut back by 39%. Overall, The New York Times points out at least 10 states reduced emissions by 30% from 2005 to 2012 (right). Analysts believe despite the drop, no states will be exempt from the additional 30% emission cuts moving forward, but recent data shows the EPA regulations can be achieved.

A handful of factors, including its cost-effectiveness and abundance in the US, has made natural gas the world’s fastest growing fossil fuel. Global consumption is expected to jump from 113.0 trillion cubic feet (Tcf) in 2010 to 185.0 Tcf in 2040. The United States, already believed to be the world’s leading natural gas producer, is at the forefront of supplying the anticipated 64% increase in global demand. The Energy Information Association (EIA) believes the U.S. will become a net exporter of the resource by 2020, and produce approximately 37.5 Tcf by 2040 (approximately 20% of the world’s consumption). The U.S. is predicted to consume 29.5 Tcf in the same year, amounting to approximately 80% of forecasted U.S. production.

Price Effects

Some critics claim the US is investing too heavily in natural gas and is doing so at the expense of other long-term energy sources. Others say the country will suffer financially once natural gas prices climb out of the sub-$5 per MMbtu range. However, Brad Plumer of the Washington Post says natural gas prices need to exceed $7 per MMbtu in order for coal plants to be competitive. That’s a tall ladder to climb, considering the EIA projects natural gas prices to stay below $6 per MMbtu until 2030 and beyond if its low price case is any indication. The Agency doesn’t expect a single coal plant to be built from 2018 to 2035.

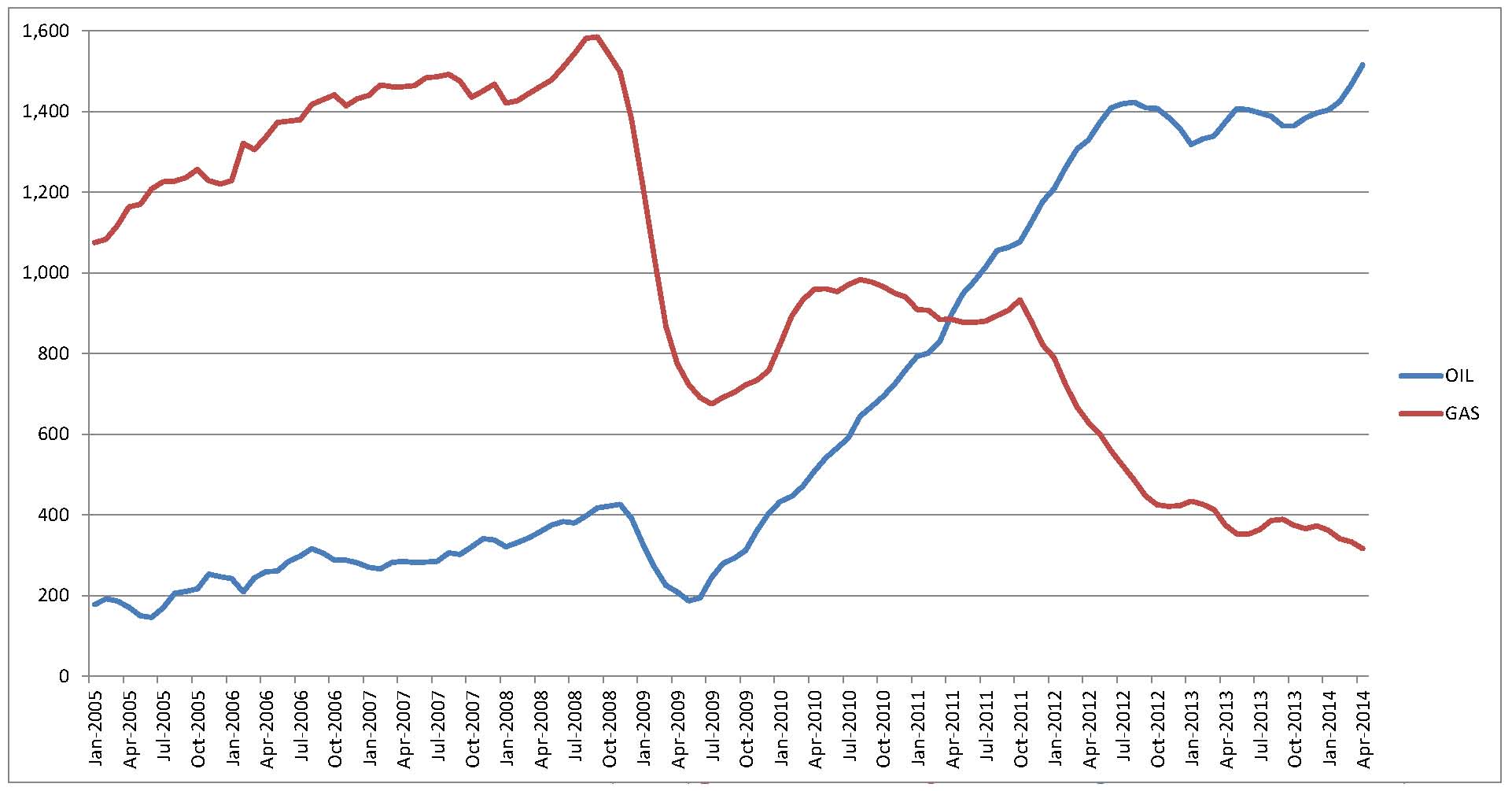

Rig Count

Consider this: United States E&Ps have been removing rigs from gas-heavy plays like the Haynesville and Barnett to focus more on oil based opportunities. Several large E&Ps have said they have long-term plans to exploit gas fields, but will not do so until the costs are more viable. The EIA reports the gas rig count in April 2014 is 340% lower than January 2005’s number of 1,075. Meanwhile, oil rigs have climbed to 1,515 from a measly 178 in the same time span (751% increase).

Baker Hughes reports historical gas plays like Barnett were running 17 gas rigs as of June 6, 2014, compared to 64 in February 2011. In the same time span, the Haynesville has dropped to 42 from 159 and the Woodford is running six rigs compared to 57 at the start of 2011. Massive plays like the Marcellus and Utica have also declined its gas rig count but not nearly to the extent of the previous three mentioned plays. Once E&Ps allocate more capital to the currently underutilized basins, the new production will only provide an extra safety net from gas prices climbing to the $7 per MMbtu coal level.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.