By Rob Isbitts for IRIS.xyz

Nineteen months ago, I declared the investment climate to be “Stormy.”

That simply means that bear market rules should be applied to your portfolio management efforts. Expect volatility, rallies and dives in stock prices which may amount to little change in prices over time. It also means being on guard for a transition from that type of waffling environment to one that feeds into the next major bear market for stocks.

We’ve had the dot-com bust, then the financial crisis and Great Recession. I don’t know what we will call the next big one.

August gave us several more pieces of evidence to support the case that the next major move for stocks will be down, not up. This is never assured until it actually happens. Thus, the key, as always, is to assess and manage the trade off between reward and potential for major downside risk.

Sure, the S&P 500 fell 2.7% for the month. But that’s merely a flesh wound at this late stage of a 10-year bull market. The bond market is throwing off more important signals. Yields plunged during August, with the benchmark 10-year U.S. Treasury moving from 2.02% to about 1.50%. It was 3.20% back in November of last year. We have not seen a move like that since back in 2011, when folks were panicked over the U.S. debt ceiling crisis.

Today, the worry is recession, trade war, a potential peak in corporate earnings, and a slowdown in global economic growth. Of those, only the recession is not already in progress. And as history shows, by the time it is declared, the market will have already reacted to it.

Still, this has been one stubborn bull, and anyone trying to bet against it with both hands had better think twice. Again, the balance has shifted toward risk-management. But that doesn’t mean there can’t be another leg higher in stocks.

The bigger concern to me is that the bond market is in the process of crushing a lot of investment plans for retirees and those approaching retirement. As I stated last month: …if history is any guide (Hint: it is), the Fed rate cut on July 31 is more likely to mark a point where investing became more dangerous. This is especially important if you are investing based on some type of very long-term strategy that blows off the threat of major market turbulence. It’s been a nice 10-year run, and it may well continue for a bit. But don’t wait until the bear is in your face to think about how you will confront it.

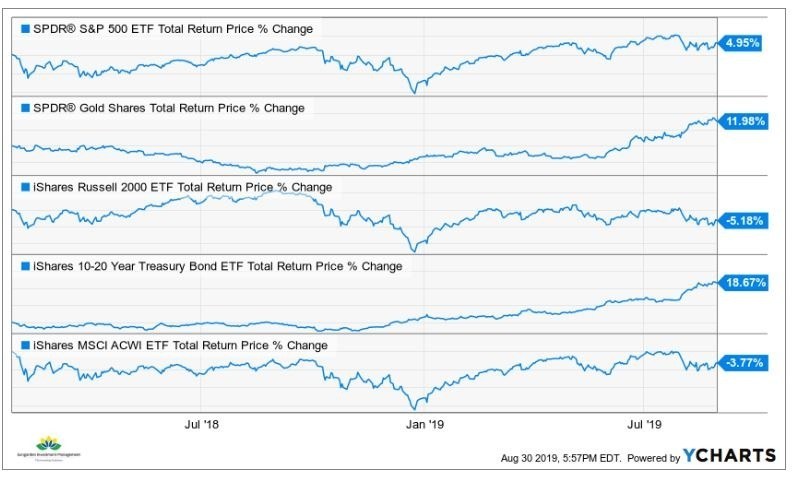

Here is a performance chart showing a variety of market segments since my “Stormy” call in January, 2018. The S&P 500 managed a gain of about 5% over those 19 months. Gold has surged recently, and so have Treasury securities. But small cap and global stocks have fallen in value. Generally speaking, it has been a difficult time to make money. At times, it looked as if the stock market was about to collapse. Welcome to Stormy.

Key Market Stress Points

- Fed rate decisions: The Federal Reserve is now front-page news. This is in part due to pressure from the White House. However, history tells us that lower interest rates probably will not prompt a surge in economic growth. That ship has sailed.

- Geopolitical: Regarding the tariff/trade war, China tends to think in decades. This could be the biggest risk to global markets: that nothing happens to repair the relationship, and global supply chains, in place for decades, start to get disrupted.

- Valuation: The Shiller CAPE version of the price/earnings ratio remains near its 1929 level. This is an impediment for significant additional gains.

- Index mania: S&P 500 index funds are very popular. That type of herd mentality will likely contribute to the next bear market panic.

- Credit: Corporate credit is at a precarious point, and consumer credit growth is off the charts. As with a decade ago, this is a threat to markets.

- Bond market risks: Approximately 50% of bonds in investment grade bond funds are rated BBB, the lowest of the four possible rating categories. Many of those bonds are likely to be downgraded at some point, and there is a nasty potential ripple effect.

- Sentiment: Consumer confidence may have peaked. The next few monthly readings will tell us a lot.

The Plan

Sure, the old bull market could have one more run higher. We always need to account for that. But the better move for investors is to look for non-traditional ways to produce returns.

My portfolios continue to be positioned with above-average caution, while still allowing a portion to ride the bull, so to speak. I am neither bull nor a bear. I am a realist and a devout risk-manager. Be careful, understand what you own, and respect the laws of gravity.

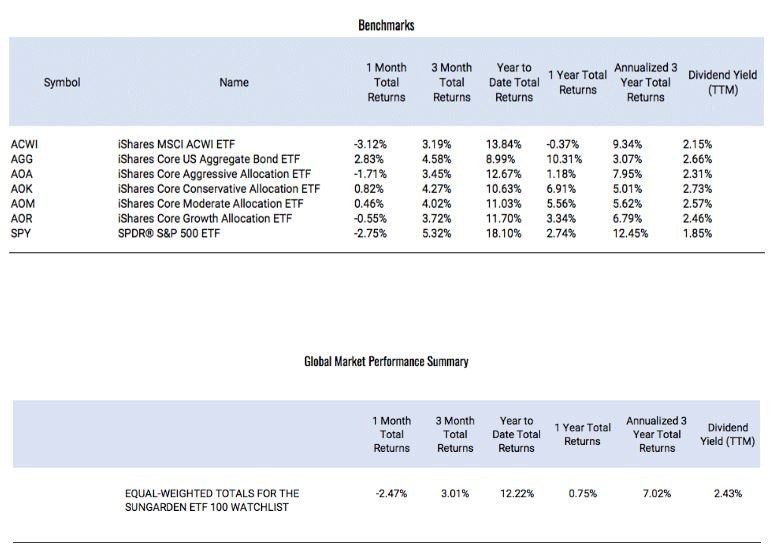

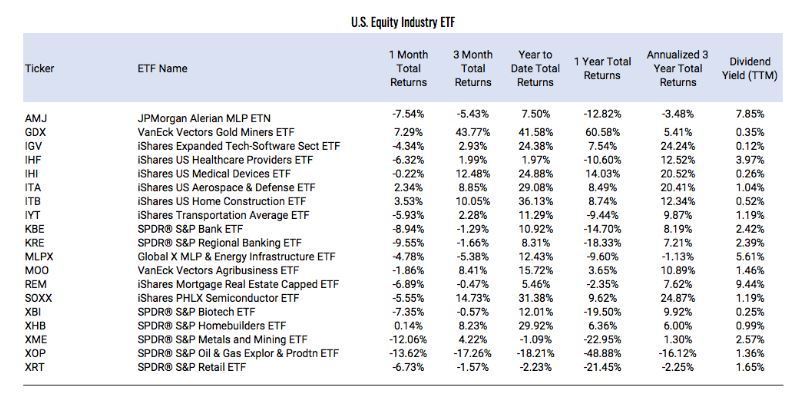

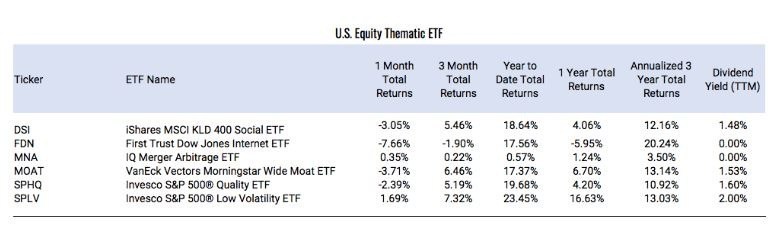

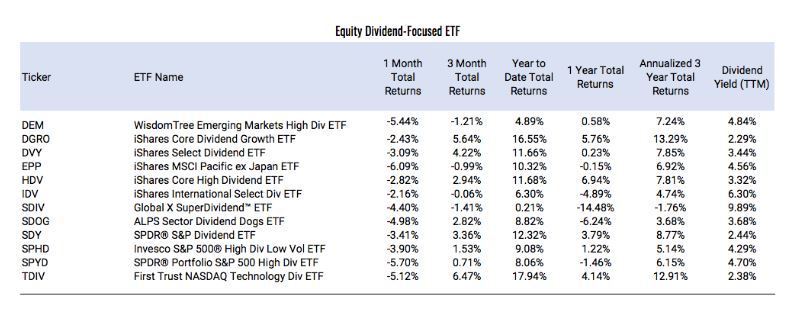

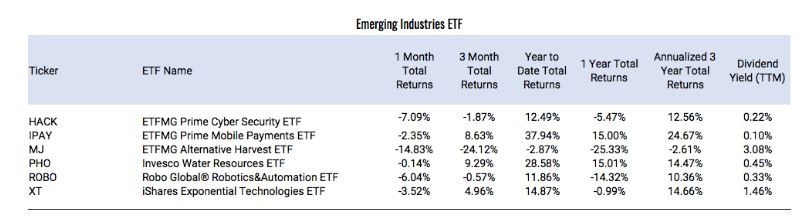

This is a group of 100 ETFs I track to get a general sense of global market conditions for investors, over the time period shown. You can see that the past 12 months has been tough sledding, only a 0.79% average advance. But as we see below, there have been plenty of winners and losers offsetting each other to produce that average.

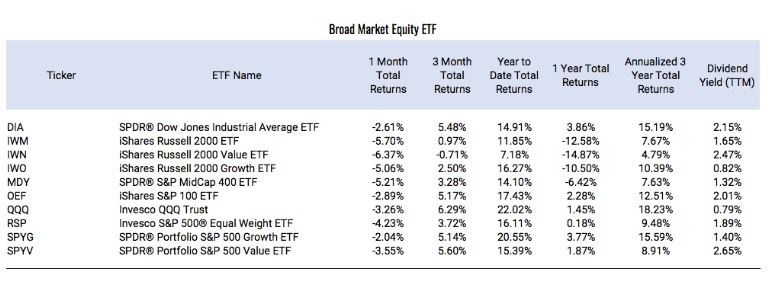

Yes, small cap stocks are down 10-15% across the board over the past 12 months. Generally, small-cap company profits are more driven by domestic business than larger companies. And, smaller companies rely more on debt to keep their businesses going. These are two very important items to watch this autumn. Are small caps a key harbinger of recession?

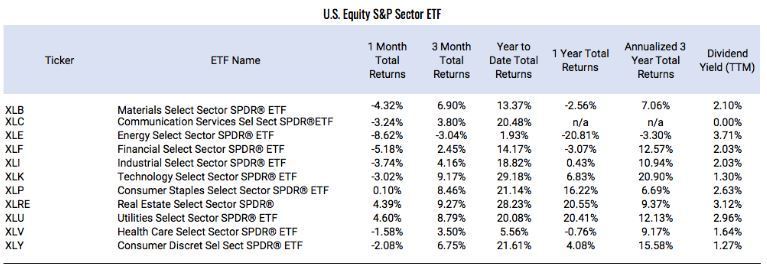

REITs, utilities and consumer staples sectors are all up nicely the past year. However, they collectively make up a small portion of the S&P 500. That’s why the S&P’s overall return is only slightly positive. The key going forward: Will these sectors continue to be treated like safe havens by investors? Or, will they just be the last to break down in a full-on downturn?

Talk about variety! Over the past year, the best sector (gold miners) is up 60%. But oil & gas exploration stocks are down nearly 50%. Everything else is in between. Only seven of 19 industries we track are up over the past 12 months. That could be a signal of fading leadership. But it will take more movement in that (downward) direction to solidify the bear case.

Low-volatility stocks are the clear winners over the past 12 months. Not surprisingly, utilities and REITs play a big role in that investment style. The question is, is it sustainable?

There is much chatter these days about dividends being higher than bond yields. The S&P 500’s yield is now higher than that of the 10-year U.S. Treasury Bond. As someone who focuses lots of attention on dividend investing, all I can say is — remember that dividend stocks are still stocks. That means they will be volatile, even if they don’t feel the impact when lower-yield stocks are getting sold off.

Cannabis stocks may be a viable industry over the long-term, but they apparently ran up too far, too fast. That little bubble popped, and they are off 25% over the past 12 months. This is partly due to investors shunning small-cap stocks, as there are no cannabis blue-chips yet.

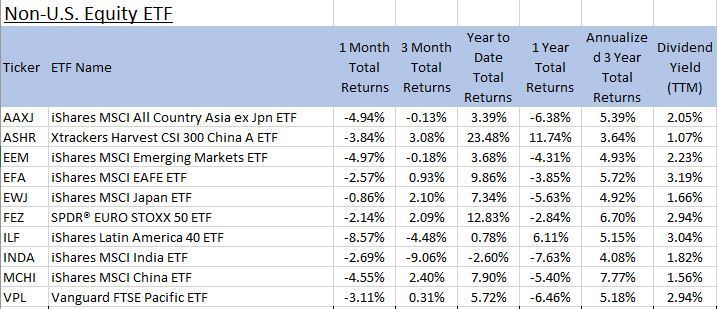

The 3-year return column says a lot about what has been going on in diversified portfolios. Non-U.S. stocks have generally produced returns in the 4% to 7% range. The S&P 500 is up 12.45% annualized over that same 3-year period. This has been a sore point for some, and one source of FOMO (fear of missing out). Diversification has its benefits, as well as its opportunity costs.

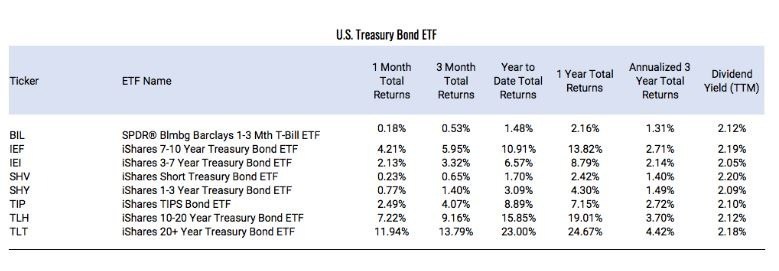

Treasury securities have produced very large gains this year, relative to what investors would expect. However, that has also driven yields down. This is a good news/bad news situation. When that trade has run its course, we’ll be left with a bond market that offers little yield and even less price appreciation potential. But I don’t think we are there yet.

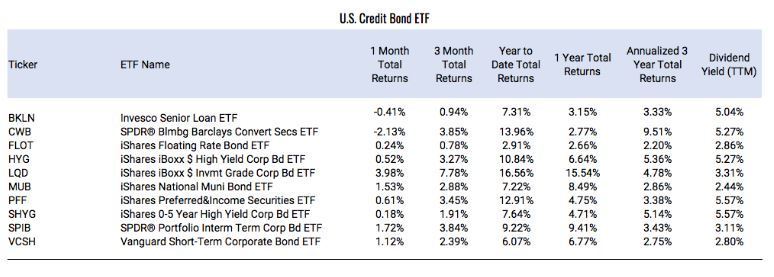

Mark these words: you will know that the threat of the next bear market is turning to reality when this category starts to show negative numbers. Right now, yield-reaching is still a popular sport. But at some point, the rubber band of declining corporate creditworthiness breaks. For now, though, it is working.

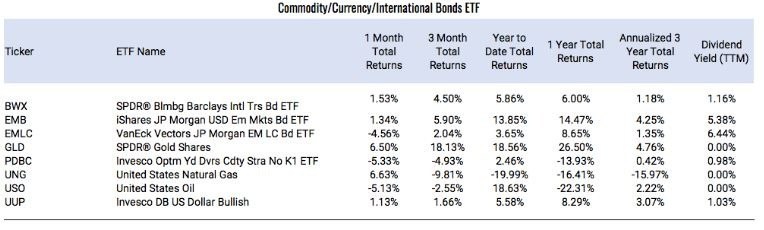

Recession-mongers can point to commodity price weakness as a case in point. Gold continues to shine, and natural gas took a break from being on the worst-performers list, with a surge in August.

Source for all ETF data: Ycharts.com

Original article at IRIS.xyz

___

Equities Contributor: IRIS.xyz

Source: Equities News

DISCLOSURE:

The views and opinions expressed in this article are those of the authors, and do not represent the views of equities.com. Readers should not consider statements made by the author as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please go to: http://www.equities.com/disclaimer. The author of this article, or a firm that employs the author, is a holder of the following securities mentioned in this article : None

Comments