On November 1, 2017 Murphy Oil Corporation (Ticker: MUR) announced its entry into the Permian basin along with its financial and operating results for third quarter of 2017, included a net loss of $66 million, or $0.38 per diluted share.

Highlights

- Achieved decade-low lease operating expense of $7.58 per boe, surpassing second quarter 2017 record

- Disclosed low-cost onshore entry into Midland Basin, currently testing Lower Spraberry and Wolfcamp B zones

- Entered four exploration blocks in the Sergipe-Alagoas Basin Offshore Brazil

- Acquired Gulf of Mexico Clipper Field, producing into the company’s operated Front Runner facility

- Maintained $1.0 billion of cash on balance sheet while investing approximately $287 million of capital

- Issued $550 million of 5.75 percent senior notes due 2025 and repaid $550 million of notes that were to mature in December 2017

[contextly_sidebar id=”1i4CG2O9Hib8MzosStuzeBFtuABzAXKJ”]Financial Results

Murphy recorded a net loss from continuing operations of $66 million, or $0.38 per diluted share, for the third quarter 2017. The company reported an adjusted loss, which excludes both the results of discontinued operations and certain other items that affect comparability of results between periods, of $6 million, or $0.03 per diluted share. The net loss includes the following items: an after-tax foreign exchange loss of $44 million, which is primarily related to inter-company loans, and a loss of $12 million from mark-to-market of open crude oil hedge contracts.

Production in the third quarter 2017 averaged 154 thousand barrels of oil equivalent per day (Mboepd). Production was negatively affected by approximately 5,100 barrels of oil equivalent per day (boepd) by the following temporary factors:

- Eagle Ford Shale partial field shut-in and delayed completions in conjunction with mid-stream and refining issues associated with Hurricane Harvey – 2,700 boepd

- Canada Offshore (non-operated) extended turnaround time and unplanned downtime – 1,800 boepd

- Tupper Montney natural gas downstream curtailments from TransCanada Pipeline – 600 boepd

As of September 30, 2017, the company had $2.8 billion of fixed-rate notes and $1.0 billion in cash and cash equivalents. The fixed-rate notes have a weighted average maturity of 9.0 years and a weighted average coupon of 5.6 percent. During the quarter, Murphy issued $550 million of 5.75 percent senior notes due August 2025, the proceeds of which were used to redeem the company’s $550 million notes due December 2017. The next senior note maturity for the company is in 2022. There were no borrowings on the $1.1 billion senior credit facility at quarter end.

Operations by Region

Eagle Ford Shale

Production in the quarter averaged 45 MBOEPD, with 89 percent liquids. During the quarter, the company brought online 27 operated wells, of which 13 were in the Catarina area, which had an average IP30 rate of 1,050 BOEPD, and 14 were in the Karnes area, which had an average IP30 rate of 1,245 BOEPD. There was also one non-operated well brought online in the Catarina area. The company continued proving the play’s multi-stacked potential with 22 Lower Eagle Ford Shale wells, four Upper Eagle Ford Shale wells, and one Austin Chalk well. As a result of increased drilling and completion efficiencies, the company brought online three more wells than originally planned. However, due to the effects of Hurricane Harvey, several wells were brought online later in the third quarter than scheduled.

For the fourth quarter of 2017, the company expects to bring 15 wells online, of which 12 are in Catarina and three are in Karnes. This will bring the number of operated online wells to 74 in 2017. As a result of the new wells, Eagle Ford Shale production will increase to over 52 MBOEPD in the fourth quarter, with full year production averaging over 47 MBOEPD.

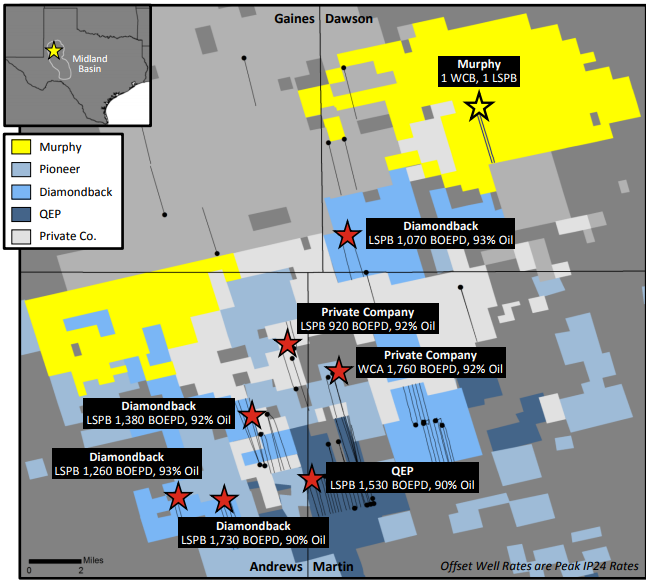

Midland Basin

During the third quarter, Murphy was the high bidder in two tracts in the University Lands Lease Sale 128, at a 75 percent working interest with a private partner. These tracts are located in Andrews and Gaines Counties, Texas, in the Northern Midland Basin. Over the past several quarters, Murphy organically leased approximately 22,000 acres at 100 percent working interest in the adjacent Dawson County. Currently, the company has leased a total of approximately 30,800 net acres at an average cost of $1,700 per acre. The acreage position is prospective in the Spraberry and Wolfcamp benches, as demonstrated by recent offset peer company well tests.

In the third quarter, Murphy drilled, cored, and cased two wells in Dawson County and is in the process of completing these wells, which are expected to be online by year end 2017. One of the wells targets the Lower Spraberry and the other targets the Wolfcamp B.

Source: Murphy Oil Corporation

Kaybob Duvernay

Production in the quarter averaged over 3,700 BOEPD, an increase of 32 percent from first quarter 2017, with 65 percent liquids. During the third quarter, three wells were brought online at the 11-18 pad in the oil window with peak rates over 1,000 BOEPD and 75 percent liquids. The company will continue to optimize completion designs and test well placement, lateral length, frac design, and flow-back strategy.

Currently, Murphy has three drilling rigs and one frac crew executing the company’s appraisal plans in the Duvernay. For the remainder of 2017, the company expects to drill six wells and bring three wells online, consistent with the previously disclosed 2017 plan. The three online wells will test the oil window as part of the ongoing appraisal and de-risking of the play. This will bring the full year wells drilled to 16 with 11 wells online.

Gulf of Mexico Exploration

During the third quarter, Murphy was the high bidder in the recent Gulf of Mexico Lease Sale for Block MC 556, which contains the Leibniz prospect. Murphy will operate the block with a 50 percent working interest.

Murphy is progressing through the permitting process for the first exploration well in Mexico Deepwater Block 5, while continuing to review the latest reprocessed wide azimuth seismic data across the acreage.

Source: Murphy Oil Corporation

Brazil Exploration

During the third quarter, Murphy entered into a farm-in agreement with Queiroz Galvão Exploração e Produção S.A. (QGEP) to acquire a 20 percent working interest in Blocks SEAL-M-351 and SEAL-M-428, located in the deepwater Sergipe-Alagoas Basin, offshore Brazil. QGEP will retain a 30 percent working interest in the blocks and, in a separate but related transaction, ExxonMobil Exploração Brasil Ltda. (an affiliate of ExxonMobil Corporation) has farmed into the remaining 50 percent working interest as the operator.

In addition, Murphy and its co-venturers were the high bidder in Brazil’s Round 14 lease sale for Blocks SEAL-M-501 and SEAL-M-503, which are adjacent to SEAL-M-351 and SEAL-M-428. ExxonMobil will operate and each company will maintain the same working interest in each of these blocks.

Murphy’s total acreage position in Brazil is 750,000 gross (150,000 net) acres over the four highly prospective blocks, offsetting several major Petrobras discoveries, with no well commitments. The company’s total commitment is approximately $18 million, including signature bonuses and seismic costs, which will be paid over 2017 and 2018.

Q&A from MUR Q3 conference call

Q: Regarding Midland, how should we think of the activity in 2018? Is it just going to be kind of a move across asset base, kind of delineate similar to how you did this year in the Duvernay? I’m just trying to get a sense of maybe what that activity could look like next year?

President and CEO Roger W. Jenkins: It’s real critical of what we’re seeing in these two wells here in one part of the play. Of course, you look at our slide in our release today, we have two acreage blocks. The one in the Northeast and one Southwest, that’s the two big large accumulations. So bringing those wells on would be very interesting to us. And the way to think about, Murphy is a $1 billion CapEx company, $1 billion to $1.2 billion over several years, with the onshore business achieving around 70% of the capital, in the State of Texas today, probably of that $700 million, probably $400 million of capital. And we consider this an extension of our Eagle Ford business, driving that from Catarina, it’s about a seven-hour drive, run by the same people, same type of execution.

We’re hoping to find a way to enhance more top-tier locations, of course, we have 600 and more of these locations at $40 oil, and probably another 700 at $45 oil breakeven, if that’s a way of tiering, which I think is appropriate. So it’s about low-cost entry, finding new places to allocate capital if these wells were to work out or allocate more capital into some tiering in Eagle Ford to this area. And then we can drill wells in the other portion of the play and see how it goes. And it’s going to be probably into January, February, before we tie off just how much capital we have into this play. And that optionality of what we plan to spend in Eagle Ford, and may allocate more capital here as we see fit.

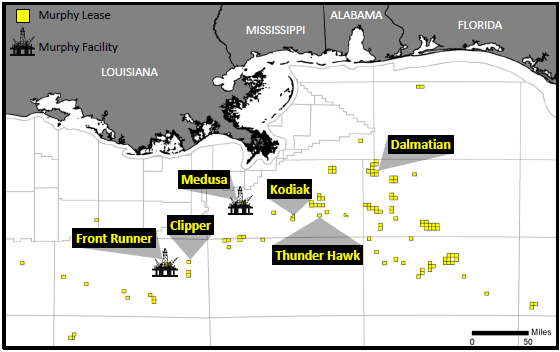

Q: Regarding the Clipper, it feels like that could be some low-hanging fruit there to bridge production. Just curious what about the opportunities look like there? And then if you could just give us a sense of what these wells looks like when you purchase and then the uplift you guys are seeing after some maintenance?

Roger W. Jenkins: There are unique – as part of our strategy, we’re in different places and we have our ear to the ground and work across spectrum in the Gulf for 60 years. We have wells that flow to our facilities. Some of those operators are looking possibly to exit or have some financial distress or they may need to exit. We’re able to help them do that, and we have all the data from the wells as it flows through our facility. So it allows us to take a look at wells, how they perform and assess the reserves of the well because we know the production levels from the well, we know the pressures from the well.

When these opportunities arise, we execute on that and add to our production that flows into our operating facilities. I believe there will be more of these things to come, it’s hard to quantify how many and when and how. But if you’re in the game, you’re able to pick up opportunities that pay out in six months and have 150% rate of return. And when people want to move their capital from some of these things to an onshore business, somewhere we may help them do that. And so we’re always out for these things. We do operate, and have been a long-time operator, with key facilities that allow us the unique ability to bringing in wells that we understand into our situation, take on their band liabilities, in some cases. And for a small amount of cost, we can pick these wells up and make a lot of money.

Q: Moving to the Permian, a pretty good explanation, as usual, of what you’re doing in the Eagle Ford and up in Canada. Thinking about 70% spinning off on the onshore out of the relatively stable CapEx number, what is the Permian spending coming at the expense of? Should I think of maybe $1.2 billion versus $1 billion, that’s my improvement or that’s my incremental dollar in 2018, maybe 2019?

Roger W. Jenkins: Well, I mean, we have situations we’ve entered into our onshore business. We’re going to have capital allocated to the Duvernay next year due to an agreement we have there, and the wells are all performing above with the curve there, and we want to invest capital there, and we are. It kind of backs into what we have in Eagle Ford. And of course, in Eagle Ford, we’ve done very well there at maintaining production there for a low level of CapEx for a couple of years, but there could be opportunities where eight wells or two pads of wells are drilled in an area to protect acreage, they may not be our top tier, and we want to move those eight wells into Permian.

After we get these wells results, we’re very pleased with nearby results after we started leasing. And you know we start leasing in mid-2016. And since all the issues with better clusters, better entry points, better core results, better sand proppant loading, different mesh on the sand, those results have gotten better and better. And so it will be a matter of testing, then we’ll move out of some acreage in Eagle Ford and put it into that area is how we’re going to handle that at this time. Until we get further into our required completions – drilling and completion spend in the Duvernay, and we’ll assess among these three plays in the next two years or so, what is the absolute best place to allocate all the capital, we’re going to do very well when we do that.

Q: With a news of a potential corporate tax rate policy, and I know energy taxes are a lot different, a lot of other taxes, is there any expectation that there could be an impact on kind of the overall deferred tax here or any sort of a tax asset that might not have of value going forward in a lower corporate tax rate environment?

Executive Vice President and CEO John W. Eckart: As you probably know, we do have deferred tax assets, net deferred tax assets in the United States. We have assets and liabilities and, overall, we have net deferred tax assets. So on day one, should the tax rates go down to 20%, let’s say, you’d have an impact on our deferred tax asset that would have to be reduced for the incremental change in the tax rate. So that would impact us and it creates a lower future value of those deferred, net deferred tax assets in the United States. So we would have an impact there, but I think many of our peers would have similar impacts. And then going forward, with prices continuing to be better, we would over time, pay, allegedly, as they have been talking about, lower tax cash taxes later on at lower tax rate.

Q: So after the Midland Basin announcement yesterday, are there any plans to increase acreage in the basin in the future? And would you guys consider expanding into the Delaware at the central platform in the future?

Roger W. Jenkins: I guess you never say never; a year and a half ago, I didn’t think I’ll be here. So we’re happy of what we have, at $2,000 an acre in the Eagle Ford, $2,000 an acre in Montney and Duvernay, and now, sub-$2,000 acres again, we go in with a different trade perspective, it’s documented in our long-term strategy, take a look at these plays, can we improve what we see, we started leasing in there and happy of what we have there today.

We worked a lot on knowledge by attending a lot of data rooms, do this for the last 30 years, but the incredible bid-ask spread was never appropriate and when you have Murphy have a differentiated view of how we can get in and prosper the way we like to work. We came up with this entry and executing on that. But today, we’re now into the high $1 per foot entry into these plays that require probably $55 oil to breakeven, at least, on a full cycle basis.

Q: So moving down to South America. Similar question, any plans to participate in the A&P auctions that are planned over the next two years? Or any plans to pursue further farm-in agreements, like you had this quarter?

Roger W. Jenkins: We will be looking to do so, but only at these working interests with the appropriate partners that have the appropriate experience and appropriate ability. One of our key co-venturers here was into the country in a very, very big way, in the last couple of months, massive on capital allocation into Brazil. If there’s an opportunity at this working level with super-majors, we’d be doing that on an exploration basis. And we do look at discovered resource opportunities there, which we can add value due to our expertise in operating offshore. That is still our primary focus.

However, that has gone slower in the Petrobras approval cycle than what we desire. And then we have been focused on working with Petrobras on the very successful fields next to these blocks and it became an opportunity to farm-in to the blocks to tie very near, we’re only 10 miles away from my five major fields discovered by Petrobras there, with very similar geological setting, pressures, depth, and oil sourcing. So we decided to enter in there again because it’s very inexpensive bang for the buck situation with a very successful partner group, and that’s our focus, and that’s why we executed on it.