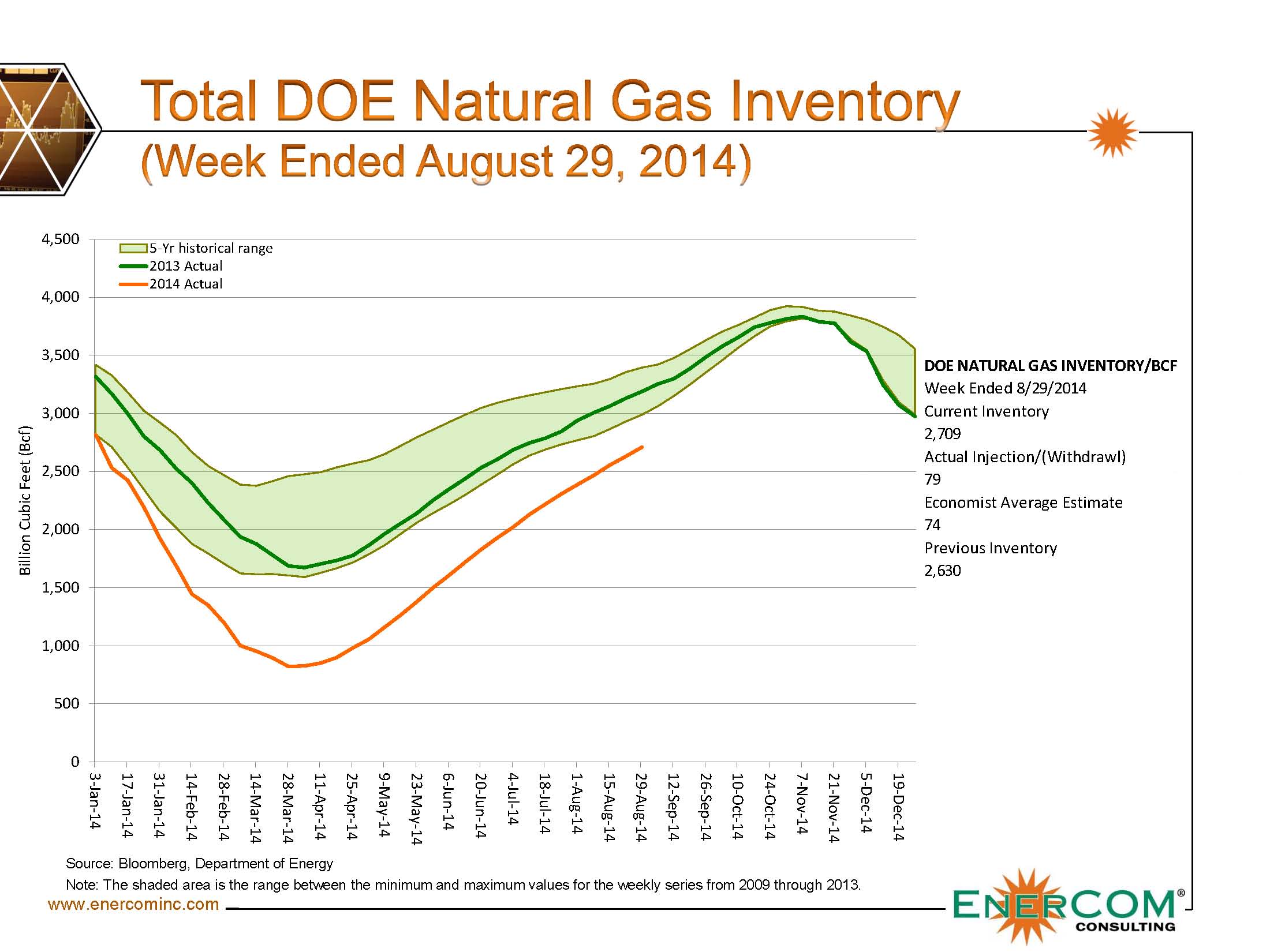

The Energy Information Administration reported a build of 79 Bcf for the week ended August 29, 2014, in its latest Weekly Storage Report. The new inventory total of 2,709 Bcf is 471 Bcf less than 2013 and 495 Bcf below the five-year average (approximately a 15% difference).

The build marks the 18th straight week of gains greater than 74 Bcf, equaling an average of 96 Bcf per week. Inventories are currently on pace for a record build (roughly 2,600 Bcf, projected). Total storage has climbed a total of 1,728 Bcf since April 25, 2014, which is 23% greater than 2013 (1,411 Bcf) and 28% greater than the five year average (1,239 Bcf).

Expect the Steep Climb to Continue

In July, Weather Services International (WSI) forecasted natural gas inventories to “largely recover” due to a cooler than normal summer season. Temperatures in the Central United States, in particular, are expected to remain below-average through at least November, according to WSI’s August forecast. Dr. Todd Crawford, Chief Meteorologist for WSI, said, “The early indications suggest that a colder winter is favored across much of the central and eastern US.”

Despite the forecast, the EIA projects this winter will have fewer heating degree days on average in its August 2014 Short-Term Energy Outlook. The report believes total natural gas inventory will be 3,463 Bcf by the end of October. In July, ESAI Power LLC, a company who collaborates with WSI, projected inventories to reach 3,700 Bcf by the end of the same time frame, which would be 4% below the five year average. The EIA’s forecast is roughly 10% below the five year average.

Prices Take a Hit

Paul Flemming, Director of Power & Gas at ESAI, said: “With low seasonal demand, natural-gas prices in the Northeast and Mid-Atlantic region will be soft relative to Henry Hub. Lower demand from the power sector and negligible demand from heating should allow further builds in natural-gas inventories.”

Storage levels are highly unlikely to return to the averages of previous years, but that doesn’t matter, according to analyst groups like BMO Capital Markets.

“The market is plainly comfortable with anticipated storage levels of 3,400 to 3,500 Bcf by the start of the winter heating season given the continued growth in the Marcellus and associated gas,” says a report released in accordance with the inventory build. “Winter weather will now be the key determinant of prices over the next six months.”

Gas prices dropped nearly $0.08 immediately after the EIA release this morning and traded below $3.80 for a portion of the day. The EIA projects spot prices to remain below $4.00/MMbtu through October and end 2014 with an average yearly price of $4.46/MMBtu. Prices for 2015, however, are expected to hover around the $4.00/MMBtu mark.

UBS Investment Research places prices at more of a premium, with a 2014 average of $4.75/MMBtu and a 2015 average of $4.50/MMBtu. “We would note gas has typically lost demand to coal when it exceeds $4.50/MMBtu, but the low storage exit [from 2013] required sustained fuel switching from gas-to-coal throughout this spring and summer to rapidly boost inventories,” reads the report, dated September 4, 2014. “These lower prices have enabled the weather adjusted supply/demand balance to tighten in August and moderate the pace of injections.”

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.