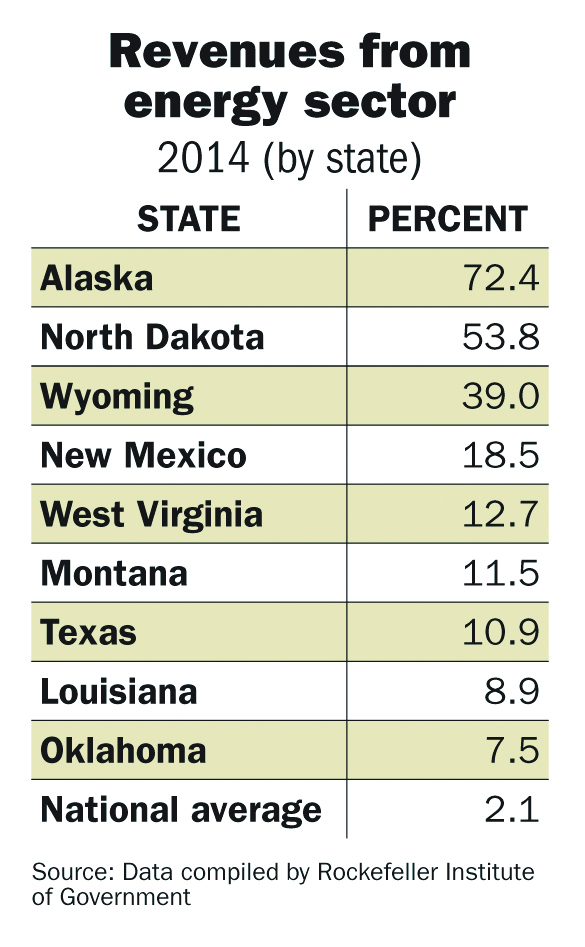

-

925 wells on backlog in North Dakota: 6-7 month inventory

-

North Dakota can still reach 2 MMBOPD

Photo Credit: Prairie Biz

By increasing its oil production to record levels, North Dakota’s economy has experienced a complete turnaround in the last handful of years, and the Williston Basin is due the majority of the credit.

The exploitation of one of the world’s premier shale plays has transformed North Dakota from one of America’s 10 poorest states in 2005 to pacing the country in standard of living and economic benefits in 2013. By February 2015, the state had set another production record at more than 1.2 MMBOPD.

Lynn Helms has witnessed the transformation firsthand since the shale boom was shifting into high gear. Helms is the director of North Dakota’s Department of Mineral Resources, and has held the position since the department’s inception in 2005. Prior to landing his first position with the state in 1998, Helms worked with oil industry giants like Hess Corp. (ticker: HES) and Texaco. He now serves as the oil and gas figurehead to a state that, if it were a country, would rank in the top-20 oil producing nations in the world.

Oil & Gas 360® spoke with Helms from his office in Bismarck, North Dakota, in this exclusive interview.

OAG360: Oil prices have stabilized in recent months and the drop in rig counts has slowed. Do you think we’ve done the trough as far as the rig count is concerned?

HELMS: Yeah that’s our sense, and feedback from operators is that we’re either at the bottom or very, very near it. We’ve seen a few more rigs idled than we expected, say a month ago, and operators are still experimenting a little bit with reducing rig counts by very small numbers to see if drilling efficiency for the remaining rigs will make up for it. But it’s very small numbers – ones and twos, out of 35 operators.

OAG360: About a year ago, Harold Hamm (CEO of Continental Resources) said North Dakota could reach production levels of 2 MMBOPD. If oil prices are disregarded, do you believe that output is realistic?

HELMS: Yes, we still have that as an expected peak production rate. The result of what’s going on right now of course pushes that further out into the future. But we still anticipate that we’ll be reaching that number.

OAG360: If oil prices stay in the $60 range, what can the state of North Dakota do to encourage more oil and gas development?

HELMS: Well, the three biggest factors in oil and gas development are, I should say this: price, price, and price!

But no, price is number one, obviously. Then tax policy is number two, and the state did reduce its extraction tax rate from 11.5% to 10% as long as oil is below $90.

Regulatory policy is probably the third big factor. I believe the state is looking at a much more stable regulatory paradigm, at least going forward in the near term, than what we did in 2012 and 2014. Those were our two biggest rule change years ever; we had 26 new rules in 2012 and 47 in 2014. And so I think part of helping out the industry is to reduce that activity at this point in time.

OAG360: Aside from regulations within the state, you now have to deal with the federal fracing rule that’s coming into view. What are the disadvantages in North Dakota involving that rule?

HELMS: They’re pretty enormous, and I spent a very long day in Casper, Wyoming, on June 23 talking about them.

HELMS: They’re pretty enormous, and I spent a very long day in Casper, Wyoming, on June 23 talking about them.

That is one of the things that that don’t seem to be recognized by the federal government, is how much of a difference the regulatory policy makes. So all of these duplicative rule-making moves and policy changes impact the industry, whether the state steps back or not. We put quite a bit of work into quantifying what those impacts because we needed to try to convince Judge Scott Skavdahl.

Our work showed that the potential cost was 1,900 jobs, ten operators basically idling their near-term drilling investments in North Dakota and a revenue cost to the state of $300 million per year. Overall, this translates into an industry economic impact reduction of around $3 billion per year.

OAG360: The general lack of infrastructure in the Williston is a common topic among operators. Has the drilling slowdown allowed infrastructure to catch up, or are midstream providers gun shy about making investments?

HELMS: No, we’ve observed that infrastructure investments are continuing at the same pace. This obviously includes the caveat that right-of-way problems are slowing the build out of pipeline infrastructure and approval problems. But I’ve had conversations with folks from the Williston, for example, in the last week and all of them say that the housing, highways and all that kind of infrastructure is continuing to build out, so it’s certainly catching up.

We’ve had meetings with the midstream, gathering and gas processing guys, and they’ve indicated that they’re going to continue their investments at the same pace as last year.

OAG360: Has it also helped with your initiatives to cut back on flaring?

HELMS: Oh very definitely. We have charted some pretty aggressive goals in terms of gas capture. If we had continued to operate 180 rigs, that would have been extremely challenging. But based on data we’re already seeing in the April data; industry is approaching the year-end goal for gas capture. So the reduced drilling in fracture activity is really allowing gas capture to catch up and that shows in the numbers. Our goal is to have 85% captured by January 1.

OAG360: Have you see many companies experimenting with gas using it on existing operations?

HELMS: There were some projects testing hydrocarbon floods, but they were suspended in this economic scenario.

What we’ve seen a huge part of expansion of is the well pad gas processing. I think there’s three times as many wells on these units compared to where we were about 1.5 years ago. And we’ve seen a lot of investment in compression in order to debottleneck the gas gathering systems.

OAG360: In March, you mentioned there were a lot of wells on backlog and they needed to be turned in line to reach drilling requirements. Do you know how many wells you have on backlog right now and how quickly those can be turned in line?

HELMS: Our current estimate is 925 and that’s pretty much a high. I mean, that’s right at the highest it’s ever been.

Going into June, we knew there were roughly 125 wells that needed to be completed within that month. By mid-June, that number was down to just 18. So it’s clearly possible for the operators to work 100 to 150 of those wells out of the backlog every month. It also means that the 925 wells is a six or seven month inventory.

OAG360: Is the quick June turnaround reflective of oil prices being at yearly highs?

HELMS: I think so – I think it was a combination of major midstream investments that allowed the gas to be captured, so that boosted the economics. A West Texas Intermediate (WTI) price above $60 was certainly beneficial. We’re also starting to see the WTI/Bakken differential collapse and we’re not seeing near the discounting, so that’s helping a lot too.

Additionally, last week the Flint Hills refinery in St. Paul, Minnesota, announced that they’re going to do a major expansion of light sweet refining. That’s probably our closest refinery, except for Mandan, North Dakota, which has always been a 100% light sweet, so that’s going to be very beneficial. All of that is working together to reduce the WTI/Bakken differential and that’s certainly helping our operators.