Goodrich Petroleum (ticker: GDP) is an independent oil and gas exploration and production company with operations in the Eagle Ford Shale, Haynesville Shale and Tuscaloosa Marine Shale (TMS).

The TMS, located in Louisiana and Mississippi, is an emerging oil play that continues to draw industry attention. During 2014, Goodrich plans to spend 80% of its $300 million capital budget on the TMS.

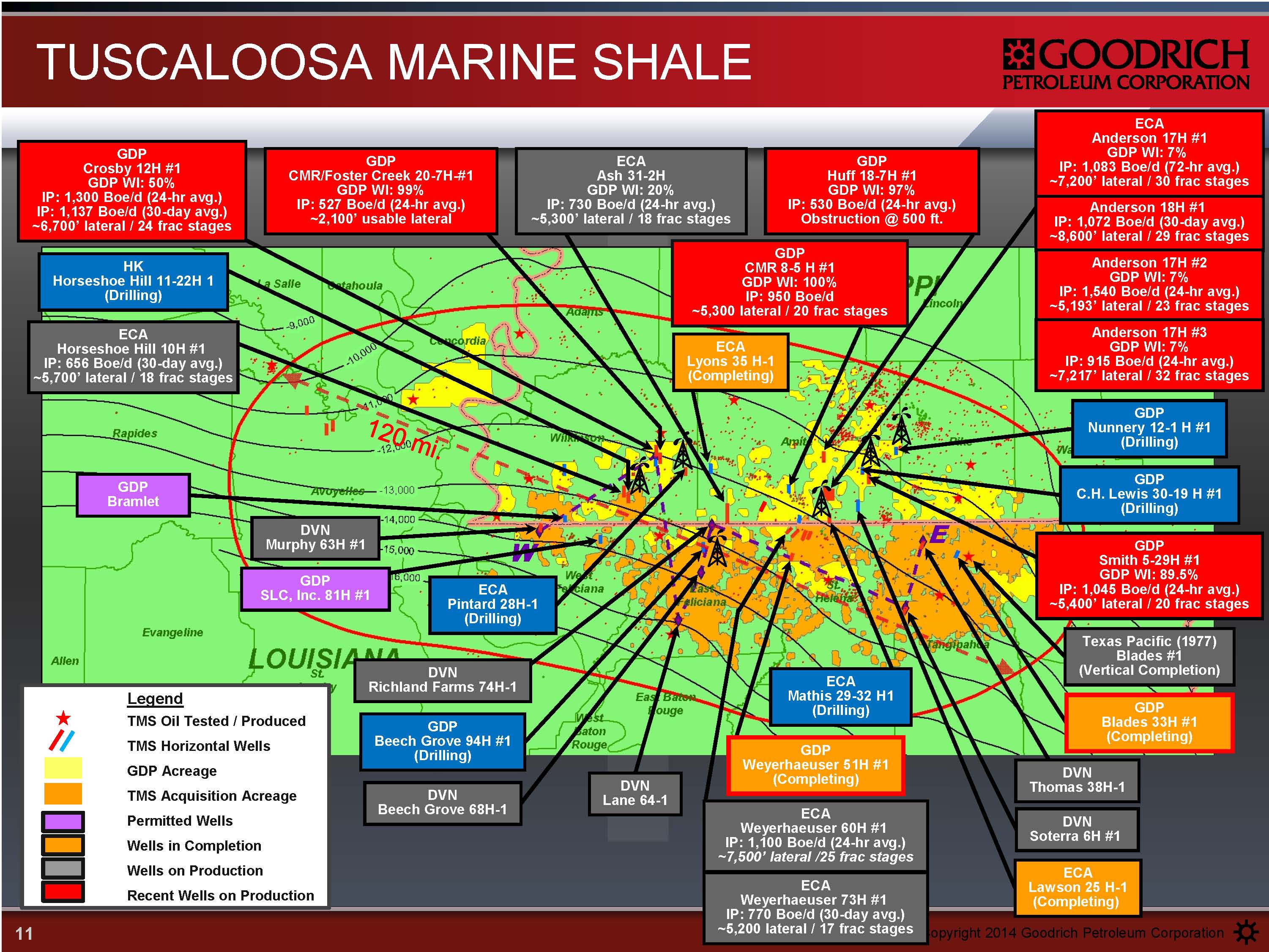

On April 14, 2014, GDP announced its Blades 33H-1 well (66.7% working interest) achieved a 24-hour production rate of 1,270 BOEPD (98% oil) from 20 frac stages. The Blades well is approximately 48 miles southeast of the Crosby 12H-1 well (50% WI), which produced a peak 24-hour rate of 1,300 BOEPD. Two more wells are being completed in Amite County, Mississippi, and are roughly at the halfway point between the Crosby and Blades wells.

OAG360 interviewed Robert Turnham, President and Chief Operating Officer of Goodrich Petroleum, on the company’s TMS operations in an exclusive interview.

OAG360: Goodrich has a long history of exploring and producing in East Texas and Louisiana. What are the unique characteristics of GDP’s past experiences that support your move into the TMS?

Turnham: [The] experience we gained from the Haynesville and the Eagle Ford plays are most applicable to our operations in the TMS. The Haynesville has a depth similar to the TMS, is over-pressured, has high temperatures and requires you run intermediate casing. When you look at the Eagle Ford, the formation is the same geologic age as the TMS and has similar completion methodologies since it is so oily.

The TMS holds certain characteristics that you don’t see in East Texas, so we initially had a bit of a learning curve. Once we discovered where to land the lateral, where to run our intermediate casing and which bits and bottom hole assemblies to use, we have been able to drill the wells in as little as 36 days. When we first started it was taking about 45 days and was costing about $13 million per well, so we have been able to cut back on our AFEs.

OAG360: How much are you saving for each day you don’t have to drill?

Turnham: We save about $100,000 for each day, and I think we can drill these in 30 days or perhaps even less in the future. If you take a look at every other play we’ve been in, we’ve been able to knock off about 13 days off the drilling curve. We feel very comfortable we can get this done in 30 days or less.

OAG360: Do you see the TMS reaching the prominence of the Eagle Ford Shale at any point?

Turnham: We do, but it’s still early. We need to step out and further delineate the acreage and prove it is repeatable. What we saw in our Blades well, for instance, is very similar to what we saw in our Crosby well, yet it is 48 miles away. We modified our completion recipe slightly on the Blades well, which was a shorter lateral yet actually had a higher production rate. We will apply this modified completion recipe to our longer laterals planned for the remainder of the year. We believe 2014 is the time for the TMS and we think it could compete with the other primary oil plays by the end of the year. We’re looking at something that is a potential company maker if the play materializes like we think it will, and we have as much leverage as anybody in the region.

OAG360: Can you elaborate on your completion techniques, particularly on the Blades 33H-1 well, without giving away any secrets?

Turnham: We pump hybrid frac jobs, which is a combination of slick water and gel. We think the slick water provides some fracture complexity and the gel transports the proppant out into the formation.

We completed the Blades very similarly to the Crosby except for a couple of minor tweaks. The only thing we really changed was when we frac the intervals, we used to do so at 270 feet per stage, and now we frac it at 250 feet per stage. We’re also pumping about 550,000 lbs. of proppant per stage versus 450,000 lbs. per stage in the Crosby. So there’s a little more sand and the frac intervals are tighter but there’s no question we saw more production per linear foot than we’ve seen on any other wells to date.

The Blades well is the first time we’ve implemented this modified completion recipe. It was a similar method but was just done on a tighter scale so we think this bodes well for future wells. We believe we can see even better production rates on an ultimate recovery basis as we drill longer laterals.

And actually we are using the technique on the two wells we are currently completing. The CH Lewis will be fraced at the end of April. It’s a 6,600 foot lateral and we’re cautiously optimistic that a longer lateral and increased proppant use will have good returns.

OAG360: Seven of your last nine TMS wells have returned a 24 hour IP rate greater than 900 BOEPD. Are these wells’ production curves holding up over time?

Turnham: Yes, when you see our wells, where we have sufficient lateral lengths and a similar frac recipe, whether it’s our wells or other operators, we’re seeing anywhere from 600 MBOE to north of 800 MBOE in EURs. So yes, we’re pleased with not only the initial rates but the decline curves are holding up very well as expected.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. As of the report date, neither EnerCom nor any of its employees has a financial interest in any equity or debt of any company mentioned in this report.