Proppant plant slowdown announcements cited changing market demand and recent softness in completions activity and frac sand demand

Last week, two of the largest proppant suppliers to the oil and gas industry announced pullbacks of frac sand production volume from some of their Wisconsin facilities.

Houston-based Hi-Crush Partners (ticker: HCLP) said it has temporarily idled dry plant operations at its Whitehall facility in Wisconsin while the plant’s wet plant operations remain operational. Both wet and dry plants are also operational in other Hi-Crush Wisconsin locations: Augusta, Blair, and Wyeville, all of which are producing Northern White sand reserves.

Another large frac sand supplier, Ohio-based material solutions giant Covia Holdings Corp. (ticker: CVIA) has either idled plants or trimmed production from several of its Wisconsin plants. Operations have idled at Covia’s Shakopee, Brewer, Wexford, and Cutler facilities, the company said in a press release, and it has reduced effective capacity at its Pevely, Cleburne, and Menomonie facilities.

Covia said that it has reduced its proppant capacity by 3.3 million tons “in response to changing market demand.”

“We remain focused on integration and synergy realization … including the ramp up of eight million tons of local capacity in the Permian and MidCon,” said Jenniffer Deckard, Covia president and CEO. These changes are not expected to affect Covia’s energy and industrial production capacity, 32 and 18 million tons respectively, she said.

In the Hi-Crush announcement, Laura C. Fulton, Hi-Crush CFO, said in a statement that the decision “was driven by recent, temporary softness in completions activity and frac sand demand.” Fulton said the reduced level of expected activity is reflected in updated guidance for sales volumes of 2.8 million to 3.0 million tons for the third quarter.

“Despite temporary market dislocations, we continue to expect strong demand for Northern White frac sand and are continuing with the expansion of rail capacity at Whitehall, as well as our customer-driven expansion of our Wyeville plant and the construction of the second Kermit facility,” said Robert E. Rasmus, CEO of Hi-Crush.

Hi-Crush said its first Kermit, Texas facility in the Permian Basin continues to be fully operational with an annual production capacity of 3 million tons of West Texas-sourced frac sand. Hi-Crush has a second Kermit facility under construction.

Frac sand markets in 2018

U.S. oil and gas drillers’ use of frac sand has changed. Operators continuously refine their completion techniques, many are moving to higher intensity fracs to drive higher returns, and many are sourcing in-basin sand, especially for Texas drilling and completions.

According to a report by Industrial Minerals, in recent years, the focus of the oil and gas industry has been on the conductivity of proppants. “Conductivity refers to the ability of hydrocarbons inside the formation to flow out between the proppant particles.”

Conductivity drove oil and gas companies to prioritize particle size, roundness, sphericity, and crush strength, IM reported. “Large sand grains, with smooth edges and as close to perfectly spherical as possible, would back together with wide gaps for oil and gas to flow out. A high crush strength, meanwhile, would prevent the sand being broken down under pressure.”

Early on in the shale boom there was one known location where these large, strong, regular sand grains could be economically sourced—Wisconsin and Minnesota’s Northern White sand was considered the Cadillac of shale boom proppant.

But the oil price crash of 2014-2016 forced E&Ps and oilfield service companies to cut costs. “Companies began to experiment with lower grade sand, compromising on regularity and crush strength,” according to the report. “In addition, a trend toward longer horizontal wells encouraged the use of smaller sand grains with a rising proportion of finer mesh sand and reduced the use of the premium 20/40 and larger mesh sizes. 100 mesh sand, once considered unsuitably fine, became increasingly valued for its ability to ‘touch more rock’, going deeper into the fractures than coarser sand.

Hi-Crush says its Kermit, Texas sand is sourced from active eolian sand dunes of the Quaternary period, with a high quartz content.

As the oil industry saw oil prices stabilizing in the $50s in 2017 and then take hold in the $60s in 2018, drillers kicked activity into high gear in the shale basins–particularly in the Permian, which now has about 45% of the U.S. rig count.

Total sand volume soared, both because horizontal wells were getting longer, and because the amount of sand used per foot of lateral was increasing—a move to higher intensity completions began driving up volumes of frac sand.

Return of CapEx, ramping of activity driven largely by the Permian frenzy, longer laterals and bigger fracs drove what IHS called “extreme demand” for frac sand

Last week’s announcements of frac sand plants idling weren’t expected. The news came on the heels of a-month old report from IHS Markit that proclaimed that sustained oil and gas exploration and production activity growth, coupled with rising U.S. CapEx investment and escalating proppant intensity were driving “extreme demand” for frac sand.

Total North American proppant demand, which includes sand as well as resin-coated sand and ceramic, is expected to exceed 168 billion pounds in 2018, representing a 27 percent year-over-year growth (2Q 2017 compared to 2Q 2018), according to the IHS Markit Proppant IQ 2Q2018 Analysis. IHS said that most of this demand is for sand, which accounts for 162 billion pounds (about 96 percent) of total North American proppant demand in 2018.

IHS calculates sand demand growth at nearly 29 percent year-over-year, for 2Q 2017 to 2Q 2018, but considering this week’s actions by Hi-Crush and Covia, in which two large suppliers slowed down their Wisconsin frac sand production, the industry numbers may tell a different story in Q3 and Q4.

IHS’s August report predicted that by 2023, North American frac-sand demand will reach an estimated 231 billion pounds, representing an increase of 113 percent above peak demand levels for 2014. By contrast, the market for frac sand for U.S. onshore oil and gas operations in 2011 was slightly more than 51 billion pounds.

Exclusive Interview

Q&A: Logistics expert Laura Fulton explains the market changes in an exclusive interview with Oil & Gas 360®

The issue is one of temporary oversupply, much more efficient completions, and logistics, according to Hi-Crush CFO Laura Fulton. Fulton is more than the company’s CFO. She happens to be a logistics expert from her time working with a large chemical company where she learned logistics management first hand as well as how to adapt a company to the cyclicality of the energy industry. Oil & Gas 360 spoke to Laura Fulton Sept. 27 for this interview.

OAG360: There was a comment in your press release about part of the Whitehall shutdown being due to softness in completions activity, lower frac sand demand. Can you talk about what you’re seeing there?

Hi-Crush CFO Laura Fulton: The softness in completions activity is really versus the expectations of where a completions growth would go throughout 2018. What we’ve seen is a lot of E&Ps have spent through their CapEx budgets because their well completions were much more efficient than they anticipated when they set those budgets.

For example, they were expecting to complete three to four to five stages per day, but they’re actually completing six or seven stages per day and so they’re getting through the well completions more quickly and therefore starting to run through their budgets faster.

And many E&Ps have pledged that they were going to stay within their cash flows and not get over their skis.

At the same time, the Permian takeaway capacity is approaching that point of being limited. There’s still some availability today, but as you go forward, there are some companies that are saying “well I need to pull back on my production generation just because I’m not going to have a place to take it away, therefore why add to the issues. Instead, I’ll just defer and wait until 2019 when the takeaway capacity is there.”

So, for a variety of reasons I think the completions activity was accelerated more than what people anticipated in the first part of the year, but now has started to slow down. That’s not to say there isn’t a heck of a lot of completions activity going on out there. It’s just you don’t have the same growth that you did earlier in the year or [the continued pace of growth that] was expected.

So, from a sand perspective, you’ve got increased supply that everybody anticipated coming from the new in-basin sand supply that’s been built in the Permian.

Admittedly, that [in-basin supply] came on a whole lot more slowly than what people expected. You’ve got more supply that is now finally starting to come to the market at a time when the demand for sand just isn’t growing as much as the supply is.

Not a red flag: sand supply outpacing oil and gas industry demand is destined to be temporary

So, the demand for sand is still growing and the proppant intensity is still strong, the well completion activity is strong, but the supply growth is overtaking that demand growth and that’s why we think it really is a fairly temporary issue because when you go into 2019, E&Ps will refresh their CapEx budgets and are likely to start going and completing again, this time anticipating the greater efficiencies and the sand demand that goes along with that.

And then as the takeaway capacity gets built, then we’re expecting even more well completion activity, more sand demand. And at that point I think the sand supply that is out there will start to be overwhelmed by the demand growth for sand and you’ll get back into the market that we were in in the first part of ’18 which was demand outstripping supply and therefore we had pricing power. But that’s kind of, again, why we believe this is temporary because there are a lot of factors that are at play here.

OAG360: Sand seems to be following the cyclical aspect of this industry—ups, downs, booms and busts.

Hi-Crush CFO Laura Fulton: It is an interesting time because everything is still going in the right direction, but some things got a little bit ahead of others and so you’re having this pullback, and I think investors particularly are fearful that the pullback means a downturn like what we experienced in 2015 and ’16.

That is not at all what’s happening here. Oil prices are still really strong. Demand is strong. It’s just that there are some constraints here and there that are causing some rebalancing of where the sand supply is going. It just happens to be all hitting right around now—in the third, fourth quarter of 2018. But it really is a pretty short-lived issue.

OAG360: Looking at the fact that you guys chose to slow down production at the Whitehall facility, why there and not somewhere else?

Hi-Crush CFO Laura Fulton: We’ve got the four facilities in Wisconsin and one right now in West Texas, and we’re building the second one in West Texas. When we looked at the outlook that our customers provide us with—their well completion activity, there’s always a normal slowdown in the fourth quarter anyway. But that seems to have been accelerated into the third quarter, and so we were looking at what are our customers’ needs going to be and answering some important questions:

- What grades of sand are they going to be requiring?

- Where are they going to be requiring that sand?

- And what are our options as far as producing the lowest-cost from a production standpoint, but also from a transportation standpoint for our customers?

The Kermit Facility in West Texas is still continuing to operate above full capacity doing really well. There is a tremendous demand for sand coming out of that facility. And then when we looked at the Wisconsin plant, given what our freight rates are for the Class I rails and what the reserves themselves will actually produce, it made more sense to shut down the Whitehall Plant that has more of a course-grade reserve compared to our other facilities. It’s also located on the Canadian National, which has been a little less beneficial to us from a freight-rate negotiation standpoint.

So when we looked at the all-in cost of producing the sand, even though our Augusta plant technically has a higher production cost per ton, the delivered cost per ton from that facility may be less than Whitehall going to several different locations where our customers are going to need the sand. So, we said if we’re going to have to cut back on one facility, it makes more sense to do Whitehall.

And it makes a whole lot more sense to operate three plants at nameplate or above nameplate capacity than it does to operate four plants at partial rates. It was all about optimizing our production to meet our customer demand, given what we see occurring or what we think will occur in the fourth quarter leading into the first quarter of 2019.

It’s more of a ‘long weekend’ than a longer term shutdown

The silver lining to all of this is that we have remarkably flexible operations. To shut the dry plant down for this temporary idling is not a big process. It’s kind of like turning it off for the weekend. It’s just going to be a long weekend. And then to turn it back on again requires going around and doing some safety checks and things like that, and then bringing our workers back online and then you’re up and running again within a week or so because we’ve got wet sand in an inventory there ready to go. It just needs to go through the dry plant process.

Having our four plants that are all remarkably similar in construction means that we have a unique opportunity right now.

We’re looking to hire people in West Texas for our second Kermit Facility. [EDITOR’S NOTE: according to Bureau of Labor Statistics data, the civilian unemployment rate for the state of Texas for August 2018 stood at 3.9%. Midland, Texas, had a 2.2% civilian unemployment rate for July 2018, according to the BLS]. Because of the Whitehall dry plant shutdown, we can actually bring some of our Wisconsin workers down to Texas temporarily to help us get that plant started, help us train the new employees and then go back to the Wisconsin facilities possibility right at the same time we were trying to start up the facility. It’s kind of just rebalancing our employee base as opposed to really having to worry about getting our workforce back. It really provided us with the best optionality to take advantage of the relationship we have with our employees, the things we’re doing in West Texas, and then the driver was what is the optimal cost structure for us to still be able to serve our customers?

OAG360: With that in mind and kind of thinking through what the customer needs are going to be coming up, do you have any sort of guidance on when you think you might turn the Whitehall plant back on?

Hi-Crush CFO Laura Fulton: Not at this time. I think we’re anticipating sometime probably middle of the second quarter or third quarter of 2019 because of my thoughts about what will happen with the Permian takeaway capacity [ramping up] and what’s going to be needed as far as sand supply at that point. But, like I said, we’ve got great flexibility and so if we need to start it back up again December 1, January 1, February 1, or whatever, we can do that at any point in time, given the wet sand inventory and the flexible nature of the operation.

OAG 360: How much of the frac sand demand in the Permian Basin area can be supplied by your Texas facilities, or is the industry always going to be having to use rail to bring sand down from Wisconsin?

Hi-Crush CFO Laura Fulton: That’s a really interesting question because you think that there’s going to be an easy answer. Demand for sand in the Permian right now is a lot of 100 Mesh, which is being produced locally in the Permian, as well as 40/70 sand, some of which is being produced in the Permian Basin, but not nearly to the extent that 100 Mesh is.

And so long term, we can see a scenario where 100 Mesh sand would be supplied out of the in-basin mines and maybe no Northern White 100 Mesh is going into the Permian.

Then on the 40/70 side, some of that would be supplied by the in-basin mines and some of it by your Northern White sand mines and still be railed in.

The interesting dynamic to that is that all the sand mines in the basin are basically located in this one kind of crescent-shaped area between the Midland Basin and the Delaware Basin. And to satisfy the demand that some people are projecting, you may need as much as 5,000 or 6,000 trucks per day all descending upon that same little area and then dispersing out to all the different well sites in the Delaware and the Midland basins.

From a logistics standpoint, it may be really hard to have all of that sand being supplied locally even though physically the sand exists and maybe mathematically you say yeah it could all work, but speaking logistically, it may be difficult to have all of those trucks coming into one area and trying to then disburse out with sand.

For that reason, we think that there still will be some amount of demand for Northern White sand coming from Wisconsin for both 40/70 and 100 Mesh, maybe greater than what the in-basin supply would indicate. Because logistically even though it may cost a little bit more to get it from the Wisconsin mines to Texas via rail, it’s going to be easier to access it because it’s right there in the middle of the Delaware basin coming out of our terminal, for example.

OAG360: Isn’t the industry being affected by the truck shortage and shortage of drivers in Texas?

Hi-Crush CFO Laura Fulton: That’s not just happening in the energy business, although the energy business certainly is a big piece of it. I think it’s happening with inter-modal and all sorts of different things. Right now the country needs the skilled labor for the different mining jobs and energy jobs that are out there, and you need them for the transportation jobs. The workers with these skills are hard to find. There just isn’t the workforce for some of those positions available right now because we as a nation stopped training people after high school for them.

OAG360: The way you bring in all the moving parts that make up the whole picture, you don’t sound like a typical CFO.

Hi-Crush CFO Laura Fulton: Well it’s because we’re not the typical company. I think a big piece of why I talk that way is because as a company, Hi-Crush is focused on logistics and when you look at our competition, they are not.

There are one or two other sand companies that have something to do with logistics. One of them in a bigger way with their container isolation, another one is still trying to figure out what they’re going to do with the silo solution that they purchased.

Other major players have just said we’re not even going to touch logistics, but that’s really where the industry is going. If you can’t move the sand and manage it for your customers, it’s going to be difficult to have those customers and we believe the right customers for at least our company long term are the E&Ps that really want us to manage that whole sand supply chain.

OAG360: You probably saw that Covia put out a similar announcement saying that they’re cutting back on production at a few of their plants.

Hi-Crush CFO Laura Fulton: They’ve got several smaller facilities that they had shut down or idled during the last downturn. Some of those are the same ones that they’re doing this time around, and those are typically smaller and much higher-cost facilities. The others that I think I talked about reducing the capacity. Realistically, they’re eliminating the frac sand capacity. They’re still running those plants for industrial sand.

But I think that’s recognition that the big players are doing the right things here. We’re taking capacity off the market at a time when [producing] it doesn’t make sense. There are probably a number of smaller, private players that are doing the same thing. They’re just not making announcements about it. There’s no sense in running the plants and trying to move some of the sand that people just don’t have a need for today. Let’s go ahead and put it to the side and then restart things when the demand picks up again next year with the Permian takeaway capacity issues resolved.

OAG360: In your press release when you guys referred to what’s happening as ‘temporary market dislocations’, could you fill in some more detail as to what exactly you were talking about with that phrase?

Hi-Crush CFO Laura Fulton: It’s that the demand through the first half of the year was picking up very strongly and people just expected that same trajectory to continue and so some of our customers—particularly the pressure pumpers—had ordered and received deliveries of sand.

But then some of their customers, the E&Ps, started slowing down their completion activity. It’s like you ordered a bunch of hamburgers for your cookout and then you just didn’t have as many guests show up and so you’re like, ‘ I’ve got all these hamburgers sitting here’. You’ll be eating hamburgers for the next week.

It’s kind of that scenario with sand. The pressure pumpers had inventory of sand built up in the basin and they needed to move that before they could order more sand. The other dislocation is coming from the in-basin mines whereas you’ve got new supply coming on, now the Northern White sand is being rebalanced to different basins.

And again, it’s something that everybody expected, but it’s a little bit hard to plan for, because you don’t know if your customer’s going to need that Northern White sand in the Permian in the month of July and then in the Marcellus in Utica in August, or if it’s going to be more in June and then switch in July. It’s just hard to tell because it’s so dependent upon what their customers decide to do. And sometimes you don’t have that visibility. With our E&P customers, we do have that visibility, but that’s only about a third of our customer base today, and it’s growing.

Those kinds of things are what we’re really referring to when we talked about the dislocations. It’s that rebalancing of where the sand is being delivered, combined with some of our customers and the industry itself taking more delivery of sand because they were expecting this continued trajectory of well completion activity that in fact slowed down.

###

Growth of in-basin sand supply

Saving on transportation, operators have begun a trend toward using locally-sourced Texas sand from in-basin mines and processing facilities. Texas mines are producing frac sand now and more are in the pipeline for the local oil patch in Texas, Oklahoma and other producing areas.

IHS pointed to oil producers who are self-sourcing, where oil and gas operators actually own the mine, or through partnerships or direct sourcing, where sand-mining companies purchase the storage and transportation assets to ensure greater efficiency and cost containment from the mine to the wellhead.

In early September Pioneer Natural Resources Company (ticker: PXD) announced that it had entered into a long-term sand supply agreement with U.S. Silica Holdings (ticker: SLCA). Pioneer is buying an interest in U.S. Silica’s sand reserves at its Lamesa, Texas, mine in West Texas. The agreement secures a 15-year supply of sand from that mine for Pioneer. Pioneer said it looks for initial sand volumes from the mine during the first quarter of 2019, with supply increasing from approximately 1.4 million tons in 2019, to 2 million tons per year in 2020 and future years.

That was not Pioneer’s first time to “self-supply” frac sand. In 2012, Pioneer acquired a large U.S. industrial sands company, which was renamed Premier Silica, and later became known as Pioneer Sands. The acquisition secured a logistically-advantaged brown sand supply for Pioneer in the Permian Basin.

“Transportation costs continue to comprise more than 65 percent of sand costs, so reducing those costs and securing supply are very valuable to operators,” IHS senior market research analyst Brandon Savisky said. “The cost (of sand) landed at the well site is heavily weighted on the logistics premiums, so transportation, coupled with proximity of supply and storage, is valuable to operators trying to manage both cost and supply chain risk.”

Some Texas producers claim they have a better product. Pioneer Sand says its Brady® sand (Texas brown sand) has conductivity and permeability that is higher than Northern White sand at well depths of up to 5,000 psi.

Permian Basin sand suppliers are ramping up. On August 28, Atlas Sand’s Kermit, Texas facility fulfilled its first scheduled deliveries of frac sand ahead of schedule. Atlas said its Kermit facility registered full capacity production of over 11,000 tons per day of output, or approximately 4 million tons annualized.

Atlas said its Kermit facility has been regularly servicing more than 400 trucks per day and is scheduled for 500 trucks per day for the month of September.

Alpine Silica said in early June it plans to open two new frac sand projects—one in Van Horn, Texas and the other in Fay, Oklahoma, each of which will produce about three million tons of frac sand per year. Alpine said the Oklahoma project would break ground during the summer with a 6-month construction period. Van Horn will be on a similar schedule.

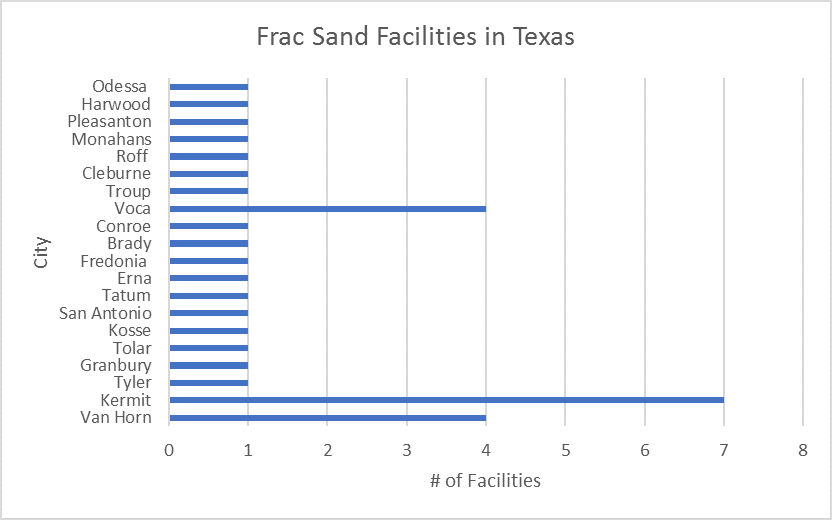

Local sand

There are currently 32 operating frac sand facilities in Texas. Most are in the Kermit, Voca, and Van Horn areas.

In-basin sand operators include Alpine Silica, Hi-Crush Partners LP (NYSE: HCLP), Black Mountain Sand, US Silica Holdings Inc (NYSE: SLCA), Vista Proppants and Logistics, Covia (NYSE: CVIA), Emerge Energy (NYSE: EMES), and Aequor.

Emerge Energy subsidiary Superior Silica Sands announced in June that it had secured a 25-year lease agreement that encompasses mining rights on 600 acres of land located approximately 60 miles northwest of Oklahoma City in Kingfisher County. Emerge said it expects volume to be about one and a half million tons per year, and it’s planning a 2018 startup for the facility.

In May, Preferred Proppants, or Preferred Sands, said it had begun construction of an in-basin frac sand mine and facility in Oakwood, Oklahoma. The mine is expected to come online in the third quarter of 2018 and will serve the prolific SCOOP, STACK and other Midcontinent formations. Previously Preferred had opened a mine in South Texas and an expansion into West Texas.