PDC expands inventory life by at least 15 years with Delaware acquisitions

Denver-based PDC Energy (ticker: PDC) announced a $1.5 billion acquisition of two privately held companies with acreage in the core of the Delaware Basin.

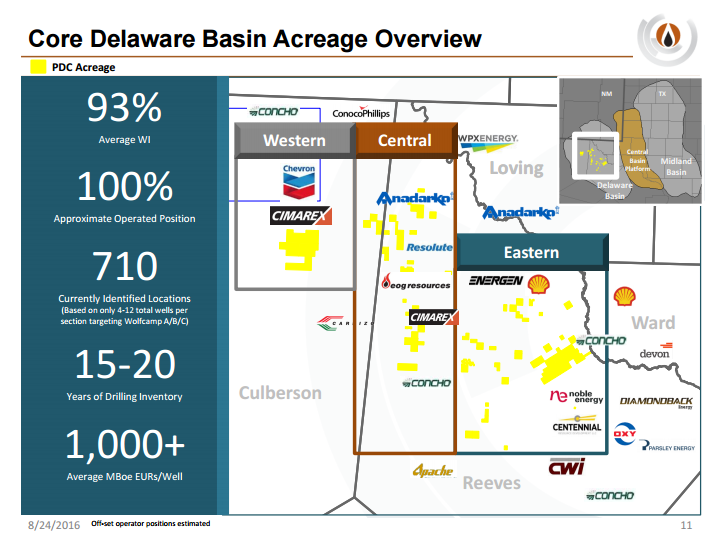

The privately negotiated transaction includes approximately 57,000 net acres in Reeves and Culberson Counties, Texas, with an average working interest of approximately 93%, according to the company’s press release. Current net production is approximately 7,000 BOEPD from 21 wells, with two additional wells in the completion and flowback phase.

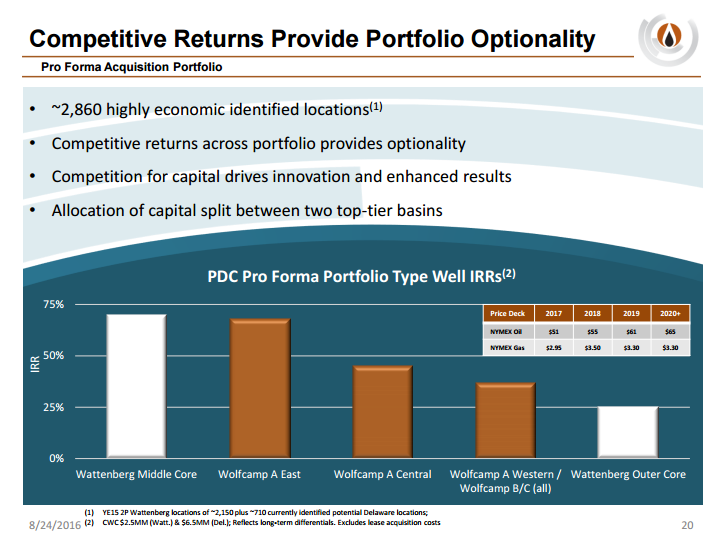

During a webcasted presentation, the company said there are currently 710 identified drilling locations on its newly-acquired Delaware Basin assets. That estimate is based on 4-12 total wells per section targeting Wolfcamp A/B/C, and PDC management believes that the potential upside for drilling locations could be significantly higher given the potential for downspacing and additional benches of pay.

When asked when PDC might start to target those additional benches, or experiment with downspacing, the company’s management said it will remain focused on the Wolfcamp while keeping a close eye on offset operators in order to decide if PDCE should consider targeting different intervals, or use tighter spacing.

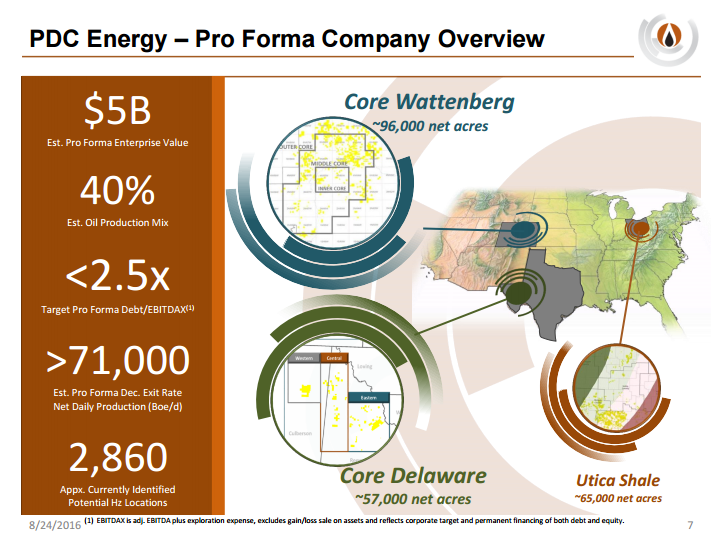

Even assuming the 710 well locations, PDC expects the acquisitions to add 15 to 20 years of gross inventory life to its U.S. assets. Along with the Wattenberg, the company’s other primary focus, PDC now has estimated net reserves potential in excess of 1 billion BOE. During the Q&A portion of the company’s webcast Wednesday, management said that it expects to spend approximately 30% of its future capex budget on the Delaware, with the remaining 70% going into the Wattenberg.

PDC management said it would like to have five rigs running in the Delaware by about 2018. The first rig will begin drilling in the central part of the company’s new assets, potentially “dipping over into the western part” of the acreage as well. The second rig to be added to PDC’s Delaware acreage will drill wells in the eastern portion of the basin, primarily drilling single well pads to hold leases.

What about the Utica?

With a 30/70 split between its Permian and DJ assets, the question that begged to be asked during the company’s webcast was: what happens to the company’s Utica assets now?

PDC Energy’s management said that it is currently waiting on the results of the five wells in the Utica it has on flowback to assess the value of the asset in its portfolio.

Potential to scale up with midstream assets

Also included in the acquisition are 100% owned and operated midstream assets across PDC’s Permian acreage. The midstream portion of deal includes approximately 50 miles of gas gathering pipeline, 30 miles of water gathering pipeline, and five salt water disposal wells, which are currently operating at less than 50% of their total capacity.

PDC believes that the included midstream assets add to the value of the assets, and plans to expand them, rather than divest. “We’re not thinking about monetization of the midstream because we would like to scale them up,” said management on the webcast. “We need to support the wells that we’re drilling.”

The company’s management also confirmed that it plans to continue executing a similar midstream buildout plan to the one it has in the Wattenberg by expanding infrastructure to meet newly drilled wells as quickly as possible and reduce potential lag times.

Deal financed with $915 million in cash and 9.4 million PDCE shares

In exchange for its new Permian acreage, PDCE will pay $915 million in cash and approximately 9.4 million shares privately placed to the sellers and valued at approximately $590 million, the company said in its press release. The company plans to fund the cash portion of the acquisition through potential equity and debt financing prior to closing, which is expected in the fourth quarter of 2016. PDC also announced that it received incremental liquidity through committed financing, bringing its current liquidity to approximately $1.4 billion.

During the company’s webcast today, PDC management said that it is targeting a pro forma debt-to-EBITDAX ratio of less than 2.5x. PDC believes that it will be able to meet that goal targeting the Wolfcamp, and, given the opportunity for further downspacing and additional intervals of pay on the acreage, may have even greater potential upside.

PDC modeling cash flow neutrality in 2019

In order to facilitate the increased drilling activity in the company’s overall portfolio, PDC is expecting to outspend cash flow by $200 million to $275 million in 2017 and 2018. The increased drilling activity should lead to cash flow neutrality in 2019, though, management said during its webcast. As prices continue to fluctuate, PDC plans to remain focused on its 2.5x debt-to-EBITDAX target, which it believes is attainable even given its modest forecasts.

The Permian gets hotter

At the 2016 EnerCom conference last week, a panel discussion with experts in the Permian basin came up with some interesting statistics and comparisons regarding recent M&A and A&D action in the Delaware and Midland basins.

Scott Rees, Chairman of Netherland Sewell, pointed out at the start of the panel’s analysis that “fifty percent of the rigs drilling for oil today are in the Permian.” Jeb Bachmann of Scotia Howard Weil offered a slide that outlines rig activity in all the counties, including Reeves and Culberson, where PCD acquired its Permian assets.

How much did PDC pay to be in the Permian?

At the EnerCom panel last week, Bachmann offered a slide detailing recent transactions in the Permian. EnerCom looked at the price paid by PDC for the Delaware basin assets.

As a point of comparison, PDCE paid $1,500 million in total consideration for 57,000 net acres and 525 MMBOE of net reserves at the midpoint, and 7,000 BOE of production. The implied metrics for the deal were $26,315.79 per acre, $75,000 per flowing BOE, and $2.86 per BOE of estimated potential net reserves reported by PDC in its presentation.