PDC: increased production, reserves and cash from operations

PDC Energy (ticker: PDCE, PDCE.com) released its year-end 2015 and fourth quarter operating and financial results, showing increased reserves, production and cash from operations for the year. According to the company’s press release, production from continuing operations increased 65% to 15.2 million barrels of oil equivalent, or 42,100 barrels of oil equivalent per day, from 2014.

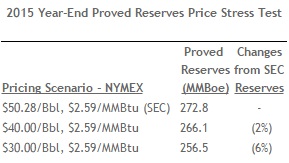

Very few companies have been able to increase their proved reserves in the current commodity market, with low crude oil prices dragging down the price deck the SEC uses to classify resources. Despite the drop in crude oil prices, PDC was able to book 273 MMBOE of reserves for the year, up 9% from 2014, and 94% of that remains economical at, or above, $30 per barrel oil, according to the company.

The company increased its proved undeveloped acreage to 74% from 70% year-over-year with through a successful Middle Wattenberg downspacing program, which the company anticipates will double its well density to 16 wells per section. PDC has also decreased the cost of its Wattenberg wells by 10% to $2.6 million, $3.6 million and $4.6 million for standard-, mid- and extended-reach laterals.

Increased production, along with greater efficiencies, helped to generate even higher levels of cash flow from operations, with PDC reporting $411.1 million from cash flow from operations, a 74% increase from last year.

Production costs for the year, including LOE, were down approximately 29% on a per barrel basis as well. PDCE reported production costs of $5.57 per barrel primarily from increased levels of production.

Targeting efficiencies in a down market

In the company’s press release, PDC President and CEO Bart Brookman said, “Our primary focus on maintaining a strong balance sheet and liquidity and the capital discipline needed to provide value-driven growth.”

According to metrics in EnerCom’s E&P Weekly, PDC Energy already has a strong balance sheet, with a debt-to-market cap ratio of just 35%, considerably lower than the group median of 165%, and a net debt-to-TTM EBITDA of just 1.7x, much lower than the median of 2.9x for the group.

In its year-end press release, the company reported liquidity of $652.2 million, up less than 1% from 2014 when the company reported liquidity of $648.4 million. PDCE reported $37 million drawn on its revolving credit facility, with $0.9 million in cash and cash equivalents. The increased liquidity was partially attributable to adjusted cash flows from operations exceeding capital expenditures in both the third and fourth quarters of the year.

The company’s TTM EBITDA on a BOE basis is also higher than the median for EnerCom’s E&P weekly at $28.11 per BOE, compared to the median of $20.17. PDC’s EBITDA margin of 68% is also well above the group median of 52%.

PDC lowered its 2016 capex budget 7% to $420 million down from $450 million in December. Brookman stated that the company estimates the 10% improvement in well costs alone will result in $40 million in savings to its current capital plan.