PetroQuest Energy (ticker: PQ) is an independent energy company engaged in the exploration, development, acquisition and production of oil and natural gas reserves in the Arkoma Basin, East Texas, South Louisiana and the shallow Gulf of Mexico.

PetroQuest Energy announced income of roughly $2.3 million for Q4’13, according to an earnings release on February 27, 2014. Income for fiscal 2013 totaled roughly $8.9 million, or $0.14 per share. The 2013 returns are directionally positive compared to 2012’s losses of $25.4 million for Q4’12 and $137 million for the year. Oil and gas sales for 2013 increased 29% year-over-year to reach $182.8 million, while production increased 15% over the same period.

The income raised discretionary cash flow for Q4’13 to roughly $27.9 million and $93.0 million on the year – increases of 37% and 20%, respectively, for the same time periods in 2012.

PetroQuest Energy recently presented at EnerCom’s The Oil & Services Conference™ 12 on February 19, 2014.

Operations

PQ exited 2013 with an estimated 302 Bcfe of proved reserves with a PV-10 value of $479 million – roughly 99% higher than reserves at year-end 2012. The company estimates it replaced 295% of its production during 2013.

Production for the year was 38 Bcfe (104.2 MMcfe/d), with Q4’13 contributing 27% of the output. PQ added 4.5 Bcfe of production through the $189 million acquisition of Gulf of Mexico properties in July 2013. Overall, 2013 production improved on a year-over-year basis of 12%, and Q4’13 climbed 15% compared to Q4’12.

Gearing up for 2014

Charles T. Goodson, Chairman, Chief Executive Officer and President of PetroQuest, said, “Our leasing campaign and producing property acquisition in 2013 lay the foundation for what we believe sets up 2014 to be the strongest year in the Company’s history.”. Daily production is projected to reach between 125MMcfe/d and 140 MMcfe/d. The guidance midpoint would be a 27% improvement compared to 2013. Q1’14 alone is expected to reach a midpoint of 114.5 MMcfe/d, which is an increase of 10% compared to 2013’s exit rate.

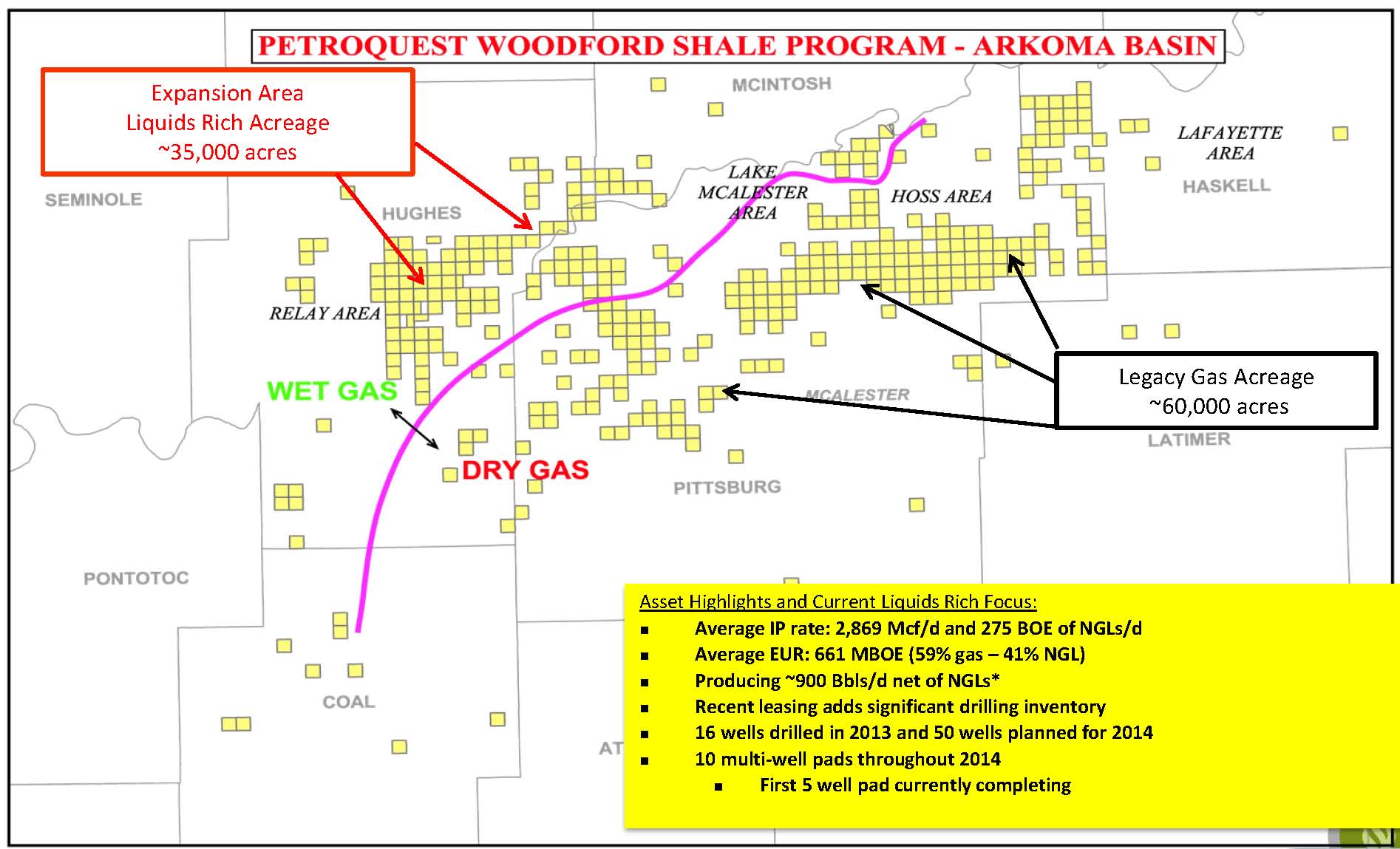

PQ’s capital expenditures program will range from $140 million to $150 million and will be funded entirely from internal cash flow. The company plans to drill an estimated 50 gross wells compared to 16 gross wells in 2013. The Woodford assets are in line to receive the lion’s share of expenditures with half of the budgeted allotment. At the time of an operations update on February 5, 2014, PQ was close to placing a five-well pad online and expects production from a separate four-well pad to commence by mid-April 2014.

Additional operations exist in East Texas, where six gross horizontal wells are scheduled to be drilled while commanding 25% (roughly $35 million) of the capital guidance. Gulf Coast operations will also receive 25% of expenditures as PQ plans to deepen an existing well that previously produced roughly 4.8 MMBOE (67% gas). The project’s pre-drill gross reserve estimate is 50 Bcfe. Rig availability for the Thunder Bayou prospect is being examined and is expected to commence drilling operations in Q2’14 The company is aiming to sell down its 75% stake in the prospect, but does not intend to have less than 50% ownership.

2014 Catalysts

- Source: PQ March 2014 Presentation

Overall guidance for 2014 includes an expected increase of more than 90% in gross well count and a 20% jump in reserve growth compared to current levels. Oil production is forecasted to increase by 54%.

In a conference call following the earnings announcement, PQ management said it will likely use production proceeds to pay down debt. The company currently has $75 million in bank debt drawn from its $200 million borrowing base but has $134 million in liquidity.

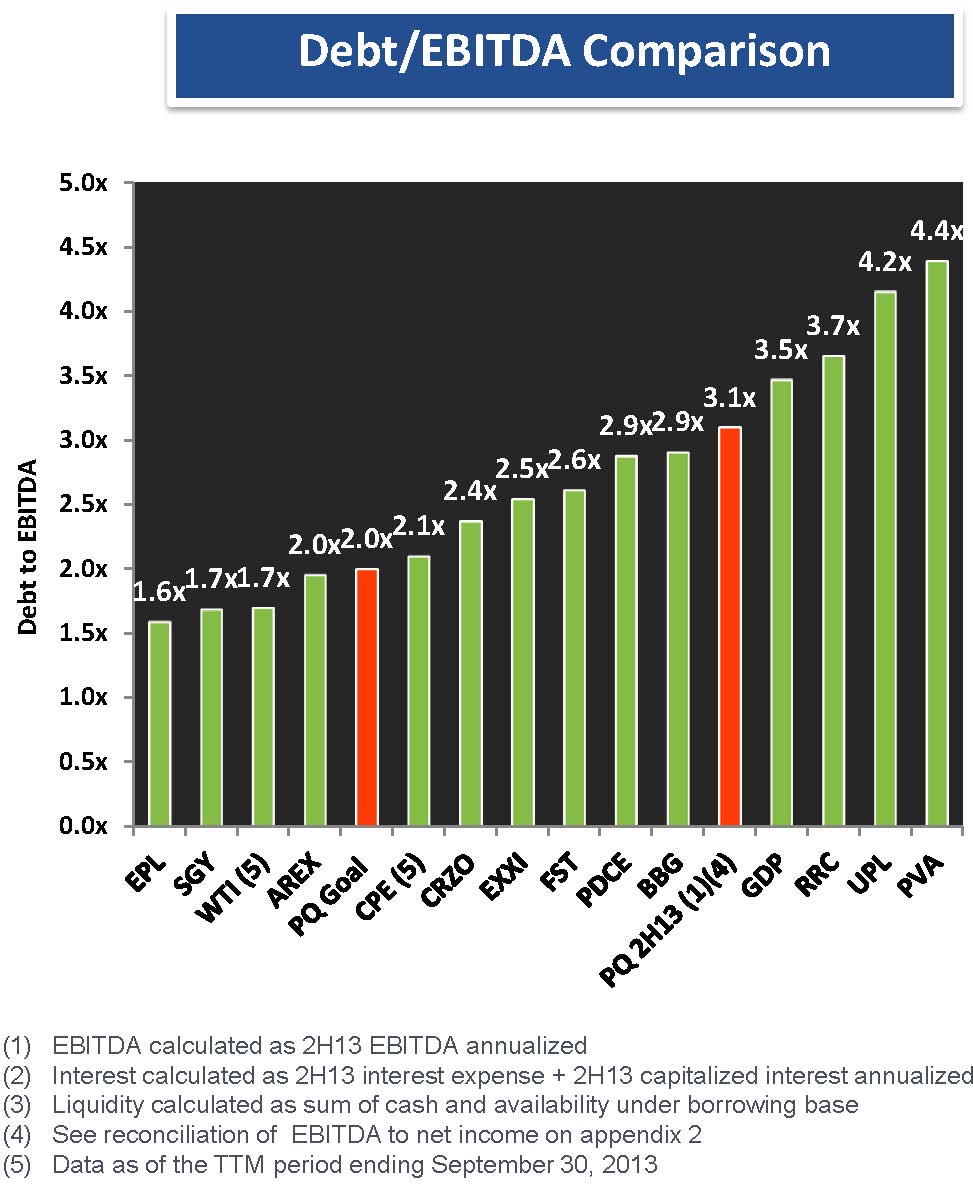

The increased production, particularly from the Gulf of Mexico purchase in Q3’13, is contributing to growth in PQ’s cash flow. Debt ratio targets have been set for 2014 as part of the company’s efforts to deleverage its financial position. PQ aims for its debt to proved Mcfe ratio to drop below $1.00. The amount was $1.41 at year-end 2013. Another interest is to drop the year-end debt to EBITDA differential to a 2.0X multiple, down from 2013’s mark of 2.9X.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication.