Pipestone Energy Corp. Announces Progress on Its Development Program and a Significant Increase in the Value of Its Reserves and Resources

CALGARY, Alberta, March 20, 2019 (GLOBE NEWSWIRE) -- (PIPE – TSX-V) Pipestone Energy Corp. (“Pipestone Energy” or the “Company”) is pleased to provide an operational update as well as updated reserves and resources information effective as of January 4, 2019, which was the closing date of the amalgamation (the “Amalgamation”) of Pipestone Oil Corp. (“Pipestone Oil”) and Blackbird Energy Inc. (“Blackbird”). A conference call has been scheduled for Wednesday, March 20th at 9:00 a.m. Mountain Daylight Time (11:00 a.m. Eastern Daylight Time) for interested investors, analysts, brokers and media representatives.

“Pipestone Energy continues to successfully execute on its development program in 2019, which includes the construction of an integrated in-field gathering and third-party compression system, capable of supporting approximately 33,000 boe/d of sales production. We recently completed drilling the final well of a 7 well program on our 3-1 pad and are preparing to complete these wells in late spring. We have been extremely pleased with the drilling performance on this pad over the past few months as we have set several new operational milestones, including a new performance pacesetter on our final well. Pipestone Energy is well positioned to meet our 2019 exit production guidance of 14,000 – 16,000 boe/d,” stated Paul Wanklyn, Pipestone Energy President and Chief Executive Officer. “The capital efficiencies we achieved during the most recent drilling and completions activities in Q4 2018 and Q1 2019 has resulted in an 11% decrease in our well costs from $9.7 million to $8.6 million. With our large contiguous land position in the condensate-rich Pipestone Montney, committed access to processing infrastructure, product egress, and a strong balance sheet, we expect to deliver strong shareholder value.”

HIGHLIGHTS

Increased the net present value before tax, discounted at 10% (“NPV10%”) of Pipestone Energy’s Proved (“1P”) reserves from $554 million to $839 million, an increase of 51% since August 1, 2018

Increased the NPV10% of Pipestone Energy’s Proved + Probable (“2P”) reserves from $1,170 million to $1,394 million, an increase of 19% since August 1, 2018

Development program to achieve 2019 exit production of 14,000 – 16,000 boe/d is on-track and on-budget

Average final 24 hour test rate on all wells completed north of the Wapiti River of ~1,790 boe/d (45% condensate) based on raw gas and wellhead condensate production (excludes natural gas liquids) (1)

Infield operated gathering infrastructure project is 95% complete

(1)Based on the latest test results (16 tests) for each well as available (excludes initial test if the well has been subsequently retested)

2019 CAPITAL PROGRAM UPDATE

Due to weather-related delays in Q4 2018, Pipestone Energy spent ~$10 million less than expected causing a shift of the capital expenditure program into Q1 2019. As a result, Pipestone Energy plans to spend between $145 - $165 million on the 2019 capital program. The Company recently finished drilling its fourth and final well for Q1 and expects to drill 9 additional wells in H2 2019. Pipestone Energy is planning to complete 7 wells in 2019 and will have a balance of 12 wells drilled but uncompleted (“DUC”) at year end 2019. The Company may elect to accelerate the completion of 3 additional DUCs into Q4 2019 depending on prevailing market conditions.

Pipestone Energy 5 Quarter Capital Program Overview (Q4 2018 – Q4 2019)

Pipestone Montney Operated Horizontal Well Status Summary

Current (March 2019)

Sept 30, 2019 (Estimate)

Dec 31, 2019 (Estimate)

South of Wapiti River (1) (CNRL Gold Creek Processing Facility)

Drilled + Completed

9

9

9

Tied-In / On-Production

8

8

8

North of Wapiti River (1) (Keyera Wapiti & Tidewater Pipestone Processing Facilities)

Drilled

27

28

36

Drilled + Completed

16

23

23

Tied-In / Available for Production

-

20 – 21

20 – 21

(1) Tied-In / Available for Production is a subset of the Drilled + Complete category which is a subset of the Drilled category.

OPERATIONS UPDATE

Completions and Well Test Results

During Q4 2018 and Q1 2019, the Company completed 6 wells on its 15-14-70-8W6 (“15-14”) pad using high intensity plug & perf (“P&P”) completions. Following the completion of these 6 wells, the 15-14 pad now has a total of 10 completed wells, which will be equipped and tied-in during H2 2019. Pipestone Energy achieved an average completion cost of ~$4.5 million ($710 per tonne) on the six wells completed during Q4 2018, a savings of ~22% from the internally budgeted cost of $5.8 million, as a result of more efficient program execution.

15-14 Pad Completion Details:

Well ID

Lateral Length (metres)

Stages / Entry Points (1) (#)

Sand Placed (tonnes)

0/12-22-70-8W6

2,691

31 / 213

6,811

2/12-22-70-8W6

2,599

30 / 205

6,560

2/13-22-70-8W6

2,476

30 / 199

6,400

3/13-22-70-8W6

2,335

27 / 185

5,824

0/14-22-70-8W6

2,435

29 / 196

6,049

0/14-18-70-7W6

2,197

26 / 172

5,568

(1) The 6 recent wells on the 15-14 pad were completed using P&P technology. In P&P operations, an entry point refers to an individual “perforation cluster” within a wellbore. Multiple perforation clusters (i.e. entry points) generally make up a single frac stage.

The Company is pleased with the test results from the recently completed six wells that were all tested on flow-back at restricted rates based on regulatory flare permit constraints. Testing provided a preliminary view of the rates, pressures and composition, as well as removed a portion of the frac water prior to production start-up in Q4 2019.

Given the large volume of water being pumped in each of these fracs, which averaged 24,500 m3 per well on the 15-14 pad, and the limited allowable flowback time, the initial test results may not be indicative of ultimate productivity and condensate ratios. Historically, Pipestone Energy has observed substantial improvements in both total production rates and condensate to gas ratios (“CGRs”) through providing “soak” time to wells by allowing them to sit for 6 – 12 months after completion or flow back on an extended basis. In the 6 wells that Pipestone has had the opportunity to re-test, the average final 24-hour daily condensate production rates have increased by 200%, along with 60% improved CGRs. Post testing the 15-14 pad, during January 2019, Pipestone Energy re-tested the 3-27-71-7W6 well, which exhibited a 222% improvement in its daily condensate rate and a 29% improvement in its CGR as compared to the initial flowback test during March 2018.

Recent Final 24-Hour Test Details:

Well ID

Montney Layer

Total Production (boe/d)

Condensate Production (bbl/d)

Raw Gas Production (MMcf/d)

CGR (bbl/MMcf)

Water Production (bbl/d)

Flowing Pressure kPa)

H2S (%)

Load Fluid Recovered (%)

15-14 Pad

0/12-22-70-8W6

B

2,192

1,115

6.5

173

2,601

4,308

2.0

%

8

%

2/12-22-70-8W6

C

1,118

241

5.3

46

886

16,044

5.5

%

9

%

2/13-22-70-8W6

B

1,876

711

7.0

102

3,759

5,601

3.5

%

8

%

3/13-22-70-8W6

C

1,211

274

5.6

49

1,077

12,599

5.5

%

10

%

0/14-22-70-8W6

C

1,223

313

5.5

57

1,000

14,849

5.5

%

6

%

3-27-71-7W6 (re-test)

B

1,629

635

6.0

106

1,462

4,159

1.4

%

13

%

Lower Montney Test Result

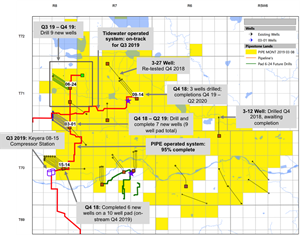

Pipestone Energy completed and tested its first Lower Montney well at 14-18-70-7W6 (“14-18”) located on the 15-14 pad. Due to H2S levels of ~10%, the well had to be restricted significantly to manage regulatory allowances related to flaring sour gas. During the final 24-hours of testing, the 14-18 well averaged 2.8 MMcf/d of natural gas, 85 bbl/d of wellhead condensate, and 805 bbl/d of flowback water at a flowing casing pressure of 13,059 kPa prior to installing a downhole choke to mitigate hydrate formation in the wellbore. Only a small amount of load fluid was recovered (6%), which may have impacted the condensate recovery. This well will be put on production once facilities are available in late 2019, at which point longer production tests will provide more indicative results on CGRs and productivity. Pipestone Energy’s in-field gathering system and pad facilities are designed to handle up to 8% H2S and Pipestone Energy will blend this gas with lower concentration H2S wells on the same pad site as required.

The Company is very encouraged by the strong initial clean-up performance of this first Lower Montney well and anticipates that the majority of its 148 net section acreage position is prospective for future development, subject to ongoing delineation work. Plans are in-place to drill a second Lower Montney evaluation well prior to year-end 2020.

Drilling

The Company has recently completed drilling the final well of a new 7 well pad at 03-01-71-8W6 (“3-1”) pad, with the seventh well achieving a new operational performance benchmark for Pipestone Energy. The anticipated average drilling cost for the seven wells, including the cost for rig mobilization and de-mobilization, is ~$2.4 million, or ~5% below the average budgeted cost per well on this pad of $2.6 million.

Infrastructure

Pipestone Energy is well underway with the construction of its in-field raw gas and condensate gathering system and pad site production facilities to be production ready in Q4 2019. Third party custom compression and natural gas processing is currently under construction by Keyera Corp. (“Keyera”) and Tidewater Midstream and Infrastructure Limited (“Tidewater”). South bound natural gas and condensate will be processed at the Keyera 03-19-067-07W6 plant with sales products being delivered to the TransCanada Corporation meter station and pipeline system (“TCPL”) and Pembina Pipeline Corporation’s Peace mainline system (“Pembina”). A key piece of the Keyera infrastructure includes the bore and pipeline pull under the Wapiti River, which has now been completed. East-bound natural gas and condensate will be processed at the Tidewater 12-35-70-9W6 Pipestone gas plant with sales products shipped to TCPL, Alliance Pipeline (“Alliance”), and Pembina. Additional marketing optionality is afforded through physical connection to the Tidewater Dimsdale Gas Storage.

Gold Creek Production – Legacy Blackbird Production

Since late November 2018, the Canadian Natural Resources (“CNRL”) Gold Creek processing facility has not been available to Pipestone Energy for production while modifications to their gas plant and processing system are underway. As a result, Pipestone Energy is not anticipated to have any significant production volumes during Q1 2019. The Company currently anticipates the resumption of production in Q2 of this year. Importantly, the lack of production has no material impact on liquidity or availability of capital, and Pipestone Energy is not revising full year 2019 or exit 2019 production guidance.

Natural Gas Transportation

During Q1 2019, the Company entered into a contract swap with a 3rd party, allowing Pipestone Energy to swap 15 MMcf/d of additional firm transportation on the TCPL system from November 1, 2021 to November 1, 2019 at the Gold Creek West meter station, which is connected to the Keyera Wapiti Gas Plant. The Company’s total firm gas transportation at the Gold Creek West meter station is now capable of handling all of PIPE’s contracted and under-option processing capacity with Keyera.

UPDATED MCDANIEL RESERVE AND RESOURCE EVALUATION

Reserves Highlights

Pipestone Energy is pleased to announce its inaugural reserves and resources evaluation (the “McDaniel Report”) performed by McDaniel & Associates Consultants Ltd. (“McDaniel”) with an effective date of January 4, 2019, to coincide with the creation of Pipestone Energy Corp., which was formed pursuant to the Amalgamation of Pipestone Oil and Blackbird.

The previously disclosed pro forma combined reserves and resources for Pipestone Energy, with an effective date of August 1, 2018, were created through the mechanical addition of Pipestone Oil and Blackbird reserve and resource evaluations. The following summary is based on the McDaniel Report and a revised development program that reflects a singular development program for the combined asset base.

Increased 1P reserve volumes by 11.7 MMboe to 90.8 MMboe (~15% increase)

Increased 1P NPV10% by $284 million to $839 million (~51% increase)

Increased 2P NPV10% by $223 million to $1,394 million (~19% increase)

Implied 2P NAV per share (excluding unbooked land value) of ~$6.78 per share utilizing a three consultants (GLJ Petroleum Consultants, McDaniel, and Sproule) average January 1st, 2019 price forecast and ~$3.19 per share utilizing March 14th, 2019 forward strip prices.

January 4, 2019

August 1, 2018

Change

Proved + Probable Reserves (“2P”)

Amount

Weight

Amount

Weight

Oil / Condensate

(Mbbls)

57,062

35

%

59,619

36

%

(2,557

)

NGLs

(Mbbls)

17,971

11

%

18,120

11

%

(149

)

Natural Gas

(MMcf)

533,422

54

%

525,013

53

%

8,409

Total

(Mboe)

163,936

100

%

165,242

100

%

(1,306

)

Proved + Probable Reserves

Proved Developed

(Mboe)

13,398

8

%

13,997

8

%

(599

)

Proved Undeveloped

(Mboe)

77,366

47

%

65,044

39

%

12,322

Total Proved

(Mboe)

90,764

55

%

79,041

48

%

11,723

Probable

(Mboe)

73,172

45

%

86,201

52

%

(13,029

)

Total

(Mboe)

163,936

100

%

165,242

100

%

(1,306

)

Reserves Before Tax NPV10%

Proved Developed

($MM)

170

12

%

140

12

%

30

Proved Undeveloped

($MM)

669

48

%

414

35

%

255

Total Proved

($MM)

839

60

%

554

47

%

284

Probable

($MM)

555

40

%

616

53

%

(61

)

Total Proved + Probable

($MM)

1,394

100

%

1,170

100

%

223

2P Net Asset Value(1)

($MM)

1,429

2P Net Asset Value per share(2)

($/share)

6.78

Best Estimate Contingent Resources - Risked (“2C”)

(Mboe)

218,227

221,258

(3,031

)

Risked 2C Before Tax NPV10%

($MM)

836

810

26

(1) 2P Net Asset Value (excluding the value of unbooked land) is calculated as: (2P Reserves NPV10% - abandonment liabilities PV10%– net debt + proceeds from dilutive securities, including publicly traded warrants).

(2) 2P Net Asset Value per share is calculated as: 2P Net Asset Value / fully diluted shares outstanding.

Commodity Prices

WTI Crude Oil (US$/bbl)

AECO Natural Gas (C$/MMbtu)

January 4th, 2019 Evaluation

August 1st, 2018 Evaluation

January 4th, 2019 Evaluation

August 1st, 2018 Evaluation

2019

$58.58

$65.30

$1.88

$2.30

2020

$64.60

$66.60

$2.31

$2.75

2021

$68.20

$69.00

$2.74

$3.10

2022

$71.00

$73.10

$3.05

$3.25

2023

$72.81

$74.50

$3.21

$3.30

2024

$74.59

$76.00

$3.31

$3.35

Summary of Reserves

Oil / Condensate (Mbbls)

NGLS (Mbbls)

Natural Gas (MMcf)

Combined (Mboe)

Before Tax NPV10% ($MM)

Proved Developed

4,225

1,443

46,377

13,398

170

Proved Undeveloped

27,254

8,496

249,699

77,366

669

Total Proved

31,479

9,939

296,076

90,764

839

Probable

25,583

8,032

237,346

73,172

555

Total Proved + Probable

57,062

17,971

533,422

163,936

1,394

Reserves Future Development Capital – As of January 4th, 2019

Total Proved ($MM) (1)

Total Proved + Probable ($MM) (2)

2019

165

165

2020

205

205

2021

165

165

2022

113

113

2023

141

141

Remainder Thereafter

70

586

Total FDC, Undiscounted (3)(4)

860

1,375

Total FDC, Discounted at 10%

681

937

(1) The Undiscounted Future Development Capital for Total Proved in the August 1, 2018 Pro Forma evaluation was $1,004 MM.

(2) The Undiscounted Future Development Capital for Total Proved + Probable in the August 1, 2018 Pro Forma evaluation was $1,739 MM.

(3) The Undiscounted Future Development Capital is escalated at ~2% per year starting in 2020.

(4) Totals may not add due to rounding.

Pre-Tax Net Asset Value – Excludes Unbooked Land Value

In $MM unless otherwise stated

As of January 4th, 2019

McDaniel Price Forecast

Strip Pricing (Mar. 14, 2019)

2P Reserves, Before-Tax NPV10%

1,394

638

(-) Abandonment Obligations – unaudited (1)

(1)

(1)

(-) Mark-to-Market of Hedges (2)

(3)

(3)

(-) Net Debt – unaudited (3)

(26)

(26)

(+) Proceeds from Dilutive Securities (4)

65

65

= Implied Net Asset Value

1,429

673

Fully Diluted Shares Outstanding (millions) (5)

211

211

Net Asset Value per Share ($/share)

6.78

3.19

Note: The Net Asset Value excludes any additional land value for 102 net sections of undeveloped land.

(1) The net present value of decommissioning obligations included above is incremental to the amount included in the present value of 2P Reserves as evaluated by McDaniel & Associates.

(2) Hedges include floating-to-fixed interest rate swaps on the term loan.

(3) Net debt represents bank debt net of working capital.

(4) Assumes the 175 million listed warrants (unconsolidated) and the 35 million Blackbird options (unconsolidated) are exercised for cash proceeds.

(5) 190 million basic shares outstanding plus the full dilutive impact of the 175 million listed warrants (17.5 million Pipestone Energy shares) and 35 million Blackbird options (3.5 million Pipestone Energy shares).

FINANCIAL RESULTS UPDATE

Pipestone Energy also announces that in accordance with the requirements of National Instrument 51-102 - Continuous Disclosure Obligations (“NI 51-102”) it expects to file the audited financial statements for its predecessor, Pipestone Oil, for the year ended December 31, 2018 on or before March 29, 2019. As Pipestone Energy was the “reverse takeover acquirer” (as defined in NI 51-102) of Blackbird in the amalgamation of Pipestone Oil and Blackbird pursuant to a series of steps under a plan of arrangement under section 193 of the Business Corporations Act (Alberta) completed on January 4, 2019 (the “Arrangement”), Pipestone Energy is required to make this historical filing.

For clarity, the reporting period of Q1 2019 will be the first quarter that the combined entity financial statements of Pipestone Energy and the accompanying Managements Discussion & Analysis will be published. The Q1 2019 financial results of the amalgamated Pipestone Energy are expected to be publicly released and filed on SEDAR on or about May 15, 2019.

Conference Call

Pipestone Energy will host a conference call to discuss the operational update and updated reserves and resources evaluation. The details of the conference call are below. An updated corporate presentation is also available on Pipestone Energy’s website at www.pipestonecorp.com.

Pipestone Energy will host a conference call on March 20, 2019, starting at 9:00 a.m. MT (11:00 a.m. ET). To participate please dial toll free in North America (866) 953-0776 or International (630) 652-5852 and enter 2673739 when prompted. An archived recording of the conference call will be available shortly after the event and will be available until March 27, 2019. To access the replay please dial toll free in North America (855) 859-2056 or International (404) 537-3406 and enter 2673739 when prompted. The conference call will also be archived on Pipestone Energy’s website at www.pipestonecorp.com.

Advisory Regarding Forward-Looking Statements

In the interest of providing shareholders of Pipestone Energy and potential investors information regarding Pipestone Energy, this news release contains certain information and statements (“forward-looking statements”) that constitute forward-looking information within the meaning of applicable Canadian securities laws. Forward-looking statements relate to future results or events, are based upon internal plans, intentions, expectations and beliefs, and are subject to risks and uncertainties that may cause actual results or events to differ materially from those indicated or suggested therein. All statements other than statements of current or historical fact constitute forward-looking statements. Forward-looking statements are typically, but not always, identified by words such as “anticipate”, “estimate”, “expect”, “intend”, “forecast”, “continue”, “propose”, “may”, “will”, “should”, “believe”, “plan”, “target”, “objective”, “project”, “potential” and similar or other expressions indicating or suggesting future results or events.

Forward-looking statements are not promises of future outcomes. There is no assurance that the results or events indicated or suggested by the forward-looking statements, or the plans, intentions, expectations or beliefs contained therein or upon which they are based, are correct or will in fact occur or be realized (or if they do, what benefits Pipestone Energy may derive therefrom).

In particular, but without limiting the foregoing, this news release contains forward-looking statements pertaining to: timing for the construction of necessary facilities and their timing to become production-ready; completion of Pipestone Energy’s 3-1 pad; anticipated 2019 exit production; 2019 production generally; 2019 capital expenditure plans; 2019 drilling plans and anticipated costs per well; 2019 well completion plans; Pipestone Energy’s ability to accelerate completion of its wells; processing plans and locations involving third parties; and marketing optionality for Pipestone Energy afforded by physical connection to third party facilities; and Pipestone Energy’s proposed drilling locations.

With respect to the forward-looking statements contained in this news release, Pipestone Energy has assessed material factors and made assumptions regarding, among other things: future commodity prices and currency exchange rates, including consistency of future oil, natural gas liquids (NGLs) and natural gas prices with current commodity price forecasts; the ability to integrate Blackbird’s and Pipestone Oil’s historical businesses and operations and realize financial, operational and other synergies from the combination transaction completed on January 4, 2019; Pipestone Energy’s continued ability to obtain qualified staff and equipment in a timely and cost-efficient manner; the predictability of future results based on past and current experience; the predictability and consistency of the legislative and regulatory regime governing royalties, taxes, environmental matters and oil and gas operations, both provincially and federally; Pipestone Energy’s ability to successfully market its production of oil, NGLs and natural gas; the timing and success of drilling and completion activities (and the extent to which the results thereof meet expectations); Pipestone Energy’s future production levels and amount of future capital investment, and their consistency with Pipestone Energy’s current development plans and budget; future capital expenditure requirements and the sufficiency thereof to achieve Pipestone Energy’s objectives; the successful application of drilling and completion technology and processes; the applicability of new technologies for recovery and production of Pipestone Energy’s reserves and other resources, and their ability to improve capital and operational efficiencies in the future; the recoverability of Pipestone Energy's reserves and other resources; Pipestone Energy’s ability to economically produce oil and gas from its properties and the timing and cost to do so; the performance of both new and existing wells; future cash flows from production; future sources of funding for Pipestone Energy’s capital program, and its ability to obtain external financing when required and on acceptable terms; future debt levels; geological and engineering estimates in respect of Pipestone Energy’s reserves and other resources; the accuracy of geological and geophysical data and the interpretation thereof; the geography of the areas in which Pipestone Energy conducts exploration and development activities; the timely receipt of required regulatory approvals; the access, economic, regulatory and physical limitations to which Pipestone Energy may be subject from time to time; and the impact of industry competition.

Information and statements regarding Pipestone Energy’s reserves and resources also are forward-looking statements, as they involve the implied assessment, based on certain estimates and assumptions, that the reserves and resources exist in the quantities predicted or estimated and can be profitably produced in the future. In addition, with respect to the type curves and test rates, there is no certainty that future wells will generate results to match type curves or test rates presented herein.

The forward-looking statements contained herein reflect management's current views, but the assessments and assumptions upon which they are based may prove to be incorrect. Although Pipestone Energy believes that its underlying assessments and assumptions are reasonable based on currently available information, undue reliance should not be placed on forward-looking statements, which are inherently uncertain, depend upon the accuracy of such assessments and assumptions, and are subject to known and unknown risks, uncertainties and other factors, both general and specific, many of which are beyond Pipestone Energy’s control, that may cause actual results or events to differ materially from those indicated or suggested in the forward-looking statements. Such risks and uncertainties include, but are not limited to, volatility in market prices and demand for oil, NGLs and natural gas and hedging activities related thereto; the ability to successfully integrate Blackbird’s and Pipestone Oil’s historical businesses and operations; general economic, business and industry conditions; variance of Pipestone Energy’s actual capital costs, operating costs and economic returns from those anticipated; the ability to find, develop or acquire additional reserves and the availability of the capital or financing necessary to do so on satisfactory terms; and risks related to the exploration, development and production of oil and natural gas reserves and resources. Additional risks, uncertainties and other factors are discussed in Blackbird’s management information circular dated November 21, 2018, a copy of which is available electronically on Pipestone Energy’s SEDAR at www.sedar.com.

The forward-looking statements contained in this news release are made as of the date hereof and Pipestone Energy assumes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by applicable securities laws. All forward-looking statements herein are expressly qualified by this advisory.

Non-GAAP Financial and Capital Management Measures

“Net debt” is a non-GAAP measure that equals total debt less current assets plus current liabilities (excluding any amounts included in total debt), and includes transaction costs and the completed debt and equity financings. Total debt is calculated as long-term debt, long-term debt due within one year and short-term debt. Net debt is considered to be a useful measure in assisting management and investors to evaluate Pipestone Energy’s financial strength. Net debt is commonly used in the oil and natural gas industry but without any standardized meaning or method of calculation prescribed by International Financial Reporting Standards (“IFRS”) or applicable law. Accordingly, Pipestone Energy’s determination of this metric may not be comparable to similar measures presented by other issuers.

Initial Production Rates and Short-Term Test Rates

This news release discloses test rates of production for certain wells over short periods of time, which are preliminary and not determinative of the rates at which those or any other wells will commence production and thereafter decline. Short-term test rates are not necessarily indicative of long-term well or reservoir performance or of ultimate recovery. Although such rates are useful in confirming the presence of hydrocarbons, they are preliminary in nature, are subject to a high degree of predictive uncertainty as a result of limited data availability, and may not be representative of stabilized on-stream production rates.

Production over a longer period will also experience natural decline rates, which can be high in the Montney play and may not be consistent over the longer term with the decline experienced over an initial production period. Initial production or test rates may also include recovered “load” fluids used in well completion stimulation operations. Actual results will differ from those realized during an initial production period or short-term test period, and the difference may be material.

Oil and Gas Measures

Barrels of Oil Equivalent – This news release discloses certain production information on a barrels of oil equivalent (“boe”) basis with natural gas converted to barrels of oil equivalent using a conversion factor of six thousand cubic feet of gas (Mcf) to one barrel (bbl) of oil (6 Mcf:1 bbl). Condensate and other NGLs are converted to boe at a ratio of 1 bbl:1 bbl. Boe may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 bbl is based roughly on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at Blackbird’s and Pipestone Oil’s sales point. Although the 6:1 conversion ratio is an industry-accepted norm, it is not reflective of price or market value differentials between product types. Based on current commodity prices, the value ratio between crude oil, NGLs and natural gas is significantly different from the 6:1 energy equivalency ratio. Accordingly, using a conversion ratio of 6 Mcf:1 bbl may be misleading as an indication of value.

Reserves and Resources Disclosure

Information in this news release regarding Pipestone Energy’s estimated reserves and resources, net present value of related future net revenue, and production is expressed on a net Pipestone Energy (as applicable) interest basis, being its respective working interest (operating and non-operating) share after deduction of royalty obligations plus any royalty interest. Estimates of future net revenue are after deduction of forecasted royalties, operating costs, estimated well abandonment and reclamation costs and estimated future development costs, but without any provision for interest costs, debt service charges or general and administrative expenses.

Reserves and resources volumes attributed to Pipestone Energy’s properties and related future net revenue are estimates only. There is no assurance that the estimated reserves and resources can or will be recovered or that estimated future net revenues will be realized. Actual reserves and resources may be greater or less than those estimated, and the difference may be material. Similarly, estimated net present values of related future net revenue attributed to reserves and resources do not represent fair market value of those reserves or resources (whether or not risked). There is no assurance that the forecast prices and cost assumptions applied in evaluating the reserves and estimating related future net revenue will be attained, and variances between actual and forecast prices and costs may be material. An estimate of risked NPV of future net revenue of contingent resources is preliminary in nature and is provided to assist the reader in reaching an opinion on the merit and likelihood of Pipestone Energy proceeding with the required investment. It includes contingent resources that are considered too uncertain with respect to the chance of development to be classified as reserves. There is uncertainty that the risked NPV of future net revenue will be realized.

The determination of oil and gas reserves and resources involves estimating subsurface accumulations of oil, condensate NGLs and natural gas that cannot be exactly measured. The preparation of estimates is subject to an inherent degree of associated risk and uncertainty, including factors that are beyond Pipestone Energy’s, as applicable, control. The estimation and classification of reserves and resources is a complex process involving the application of professional judgment combined with geological and engineering knowledge to assess whether specific classification criteria have been satisfied. It requires significant judgments based on available geological, geophysical, engineering, and economic data as well as forecasts of commodity prices and anticipated costs. As circumstances change and additional data becomes available, whether through the results of drilling, testing and production or from economic factors such as changes in product prices or development and production costs, reserves estimates also change. Revisions may be positive or negative.

Unless otherwise indicated: (i) reserves and resources estimates have been prepared by McDaniel’s, Pipestone Energy’s independent qualified reserves evaluators in accordance with the COGE Handbook, have an effective date of January 4, 2019 and represent Pipestone Energy’s working interest share; (ii) drilling locations have been derived from reports by McDaniel’s; and (iii) projected and historical production volumes provided represent Pipestone Energy’s working interest share before royalties.

Certain contingencies currently prevent the classification of Pipestone Energy’s contingent resources as reserves. The 218.2 MMboe 2C Resources disclosed in this news release include Pipestone Energy’s Risked Best Estimate Development Pending Contingent Resources in the Pipestone / Elmworth Montney area. The corresponding estimate of risked before tax NPV of future net revenue for Best Estimate Development Pending Contingent Resources, using a discount rate of 10% per year, is $835.9 million. The product types associated with Pipestone Energy’s contingent resources include crude oil, natural gas, condensate, and NGLs.

All of Pipestone Energy’s contingent resources disclosed in this news release have been sub-classified as “Development Pending”, which applies in circumstances where resolution of the final conditions for development is being actively pursued and indicates a relatively high chance of development versus the other sub-classifications.

All of Pipestone Energy’s contingent resources have been risked using an 80% chance of development. In quantifying the chance of development, the factors that were assessed quantitatively to be less than one in the development risk calculation included the economic status, the project evaluation scenario status, and the development time frame. The chance of development multiplied by the unrisked resource volume estimate yields the risked resource volume estimate. As many of these factors have a wide range of uncertainty and are difficult to quantify, the chance of development is an uncertain value that should be used with caution.

Continuous development through multi-year exploration and development programs and significant levels of future capital expenditures are required in order for additional resources to be recovered in the future. The principal risks that would inhibit the recovery of additional reserves relate to the potential for variations in the quality of the Montney formation where minimal well data currently exists, access to the capital required to develop the resources, low commodity prices that would curtail the economics of development and the future performance of wells, regulatory approvals, access to required services at an appropriate cost, and the effectiveness of well fracturing technology and applications. For contingent resources to be converted to reserves, Pipestone Energy must ascertain commercial production rates, then develop firm plans, including with respect to timing, infrastructure and the commitment of capital. Confirmation of commercial productivity is generally required before Pipestone Energy can prepare firm development plans and commit required capital for the development of the contingent resources. Additional contingencies relate to the current lack of infrastructure required to develop the resources in a relatively quick time frame. As continued delineation occurs, some resources currently classified as contingent resources are expected to be re-classified to reserves.

The estimated cost reflected in McDaniel’s evaluation of Pipestone Energy’s contingent resources to bring on commercial production from the Risked Best Estimate Development Pending Contingent Resources for all four product types is approximately $3,576.3 million (when discounted at 10%, the estimated cost is approximately $1,070.2 million). The expected timeline to bring these resources on production is between the years 2022 and 2043 (in accordance with a pre-development study). Best Estimate Development Pending Contingent Resources are expected to be recovered using the same technology of horizontal drilling and multi-stage fracturing that Pipestone Oil successfully used in its Pipestone/Elmworth Montney play.

The estimates of contingent resources provided herein are estimates only and there is no guarantee that the estimated contingent resources will be recovered. Actual contingent resources may be greater or less than the estimates provided in this news release, and the differences may be material. The estimates of contingent resources and future net revenue for individual properties may not reflect the same confidence level as estimates of contingent resources and future net revenue for all properties, due to the effects of aggregation. There is no assurance that the forecast price and cost assumptions applied by McDaniel in evaluating Pipestone Energy’s contingent resources will be attained and variances could be material. There is uncertainty that it will be commercially viable to produce any portion of the contingent resources described herein, or that Pipestone Energy will produce any portion of the volumes currently classified as contingent resources.

Pipestone Energy Corp.

Pipestone Energy Corp. is an oil and gas exploration and production company with its head office located in Calgary, Alberta. The company is focused on developing its pure-play condensate-rich Montney asset in the Pipestone area near Grande Prairie. Pipestone Energy is committed to building long term value for our shareholders and values the partnerships that it is developing within its operating community. Pipestone Energy shares trade under the symbol PIPE on the TSX Venture Exchange. For more information, visit www.pipestonecorp.com.

Pipestone Energy Contacts:

Paul Wanklyn President and Chief Executive Officer (403) 228-8684 paul.wanklyn@pipestonecorp.com