The Energy Information Administration’s (EIA) Drilling Productivity Report, a monthly breakdown on production by basins, typically forecasts production increases across the United States’ seven most prolific plays. The latest edition, released on March 9, 2015, projects production in April to be higher than the current month.

However, that increase has slowed dramatically.

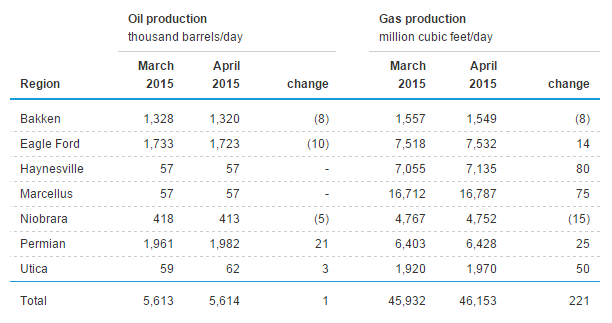

Production for March is forecasted at 5,613 MBOPD and 45,932 MMcf/d, while April is projected to be 5,614 MBOPD and 46,153 MMcf/d – increases of just 1 MBOPD and 221 MMcf/d, respectively. Out of the four major oil plays (Bakken, Eagle Ford, Niobrara and Permian), only the Permian is expected to increase its volume in April. The “other” three oil fields are projected to lose 23 MBOPD (24.5 MBOEPD, including gas) of volume next month.

With domestic production seemingly losing steam, market analysts like John Kemp of Reuters published an article titled “OPEC is winning its Battle with U.S. Shale.” The EIA has trimmed its production estimates for the last two months.

Meanwhile, the future prices for Brent were revised upward in the Administration’s Short Term Energy Outlook. The forecasted 2015 average price for Brent was bumped up to $59 from its previous estimate of $57, and prices are expected to reach $75 in 2016. West Texas Intermediate (WTI) is expected to be $52 and $70 in 2015 and 2016, respectively, down from February’s estimate of $55 and $71. The EIA is also expecting the 2015 WTI/Brent spread to widen, with the newest forecasts expanding to $7 from its previous estimate of $3.

“The Brent-WTI spread for 2015 is more than twice the projection in last month’s STEO, reflecting continuing large builds in U.S. crude oil inventories, including at the Cushing, Oklahoma storage hub,” the report says. The U.S. had added approximately 56 MMBO to its inventories in the last seven weeks, placing total storage utilization at all-time highs. Analysts polled by Bloomberg expect another 4.7 MMBO to be added to storage in the next crude inventory report, scheduled for release on March 11.

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note.