“(The Marcellus) gives us the confidence to say we think we can grow at 20% to 25% for many years with improving capital efficiencies as we go forward into a better gas pricing environment,” said Jeff Ventura, Chief Executive Officer of Range Resources (ticker: RRC), in the company’s Q1’2014 conference call with investors and analysts on April 29, 2014. Ray Walker, Range COO, said during the conference call: “We’ve got a really top-notch technical team that’s doing tons of analysis and reservior modeling. We’re in the core position in the play which has better perm, better porosity, more hydrocarbon in place. I really think, as fast as things are changing, that we’re still only in the third inning, maybe in the top of the fourth, trying to figure out what the potential couldbe going forward.”

Q1’14 Results

Range announced average production of 1,056 Mmcfe/d for Q1’14, a company record, in its earnings release on April 28, 2014. The company surpassed the 1,000 Mmcfe/d milestone in December 2013. Adjusted cash flow totaled $262 million (20% higher than Q1’13) and net income reached $33 million ($0.20 per share).

RRC recently provided information on its marketing program in an updated investor presentation. The program, covered by OAG360 in a recent feature article, consists of different pricing formulas based on gas quality to meet the needs of customers while minimizing refinement. In all, the program has ten different indices and 85%-90% of sales are tied to what the company deems as favorable markets. The varied pricing provides a revenue increase of 25% as opposed to leaving ethane in the gas stream. The contracts are aided through increased pipeline buildout in the Northeast and allow RRC to grow production to 3,000 Mmcfe/d in the short-term. The company says 25 new customers were added in 2013 and 14 have been added thus far in 2014.

In a conference call following the release, RRC management said its resources will be selling on 20 different indices by 2017 with 15 located outside of the Appalachian Basin. Range has approximately 80% of its 2014 production hedged at weighted NYMEX prices of $3.96 and $4.38 per Mmbtu, enabling consistent returns on its production. Range has historically been one of the lowest cost producers in the region, and quarterly operating costs dropped by 6% in the most recent quarter, amounting to $0.23/Mmcfe overall. Operating costs may drop further with Range’s increased use of longer laterals.

Southern Marcellus

Range has divided its operations into four different divisions; the southern Marcellus, northern Marcellus, Midcontinent and southern Appalachia. The company turned 20 wells turned to sales in the quarter at a 100% drilling success rate.

The southern Marcellus provides the majority of RRC’s production, returning 800 gross (672 net) Mmcfe/d in the quarter. A Washington County well produced a 24-hour rate of 38.1 Mmcfe/d (65% liquids) and is believed to hold the highest single-day return in the region’s history. The drilling program previously set lateral lengths at 5,300 feet but have since expanded to as deep as 7,065 feet. Nine rigs are currently operating in the region and are expected to turn 115 wells to sales within fiscal 2014. A test Utica well is currently being drilled to 6,500 feet with results expected by Q4’14. In a conference call following the release, RRC management said it believes its position is within the dry core of the Utica. Three nearby dry gas wells drilled to 4,768 feet are expected to each produce 20 Mmcf/d once operational.

Range’s nine rig program, consisting of three air lift rigs and six horizontals, will be reduced by three horizontals by the end of 2014. Despite the reduction, Range will maintain its line of sight growth by recovering more resources on less acreage. Management said Marcellus operations have grown at an annual compound growth rate of 96% since 2009.

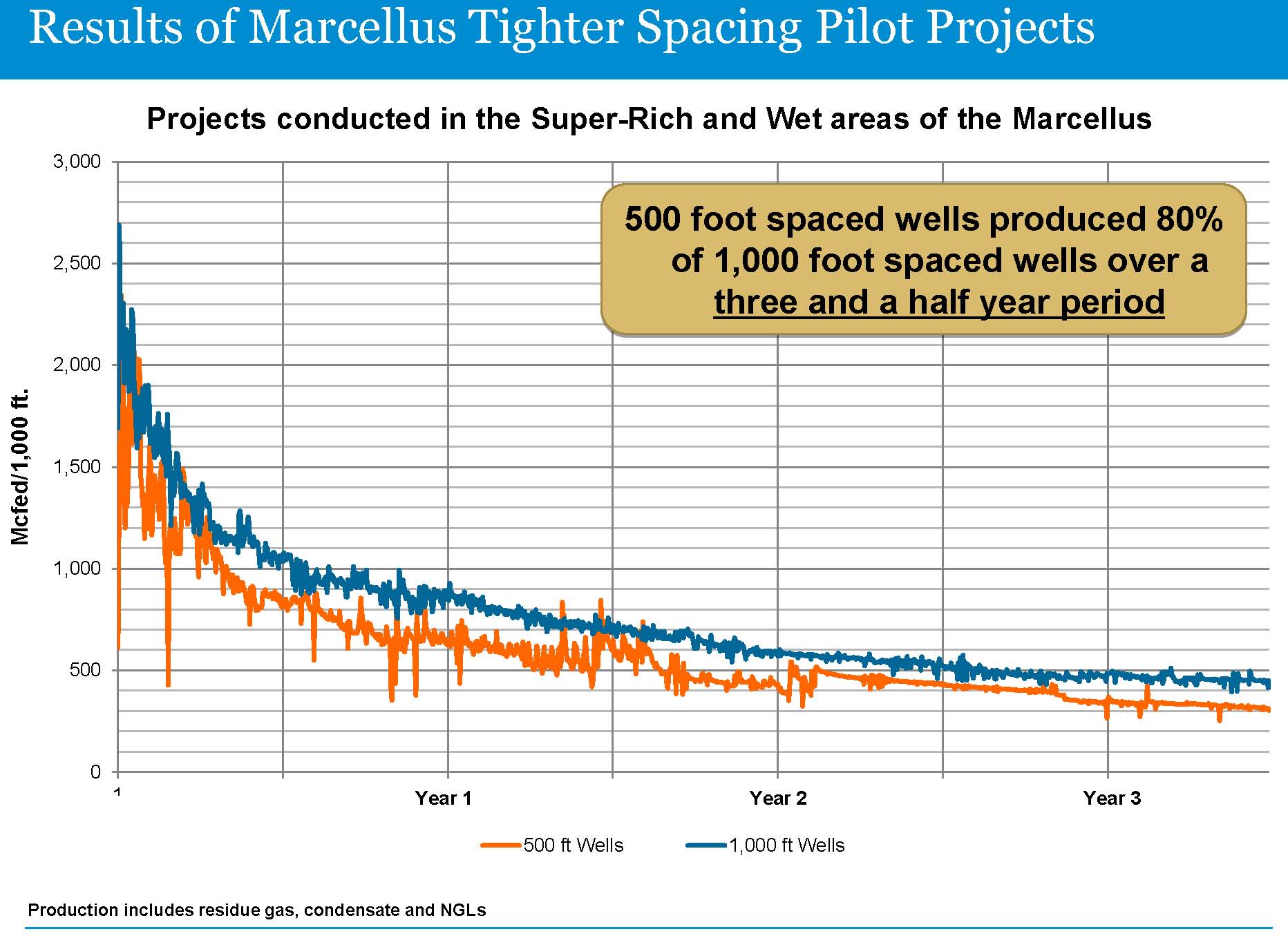

In the conference call, Ventura said: “We intend to develop that entire position and, remember, that position is about 530,000 net acres. On 80-acre spacing just in the Marcellus, there are over 6,000 locations to drill lands. And it looks like we can go tighter.”

RRC is currently producing from only 8% of its southern Marcellus position.

Remaining Operations

The northern Marcellus produced 232 (195 net) Mmcfe/d in Q1’14 and has nine backlogged wells waiting on pipeline completion. A total of 13 wells are expected to be turned to sales within 2014 on one rig. A four-well pad drilled in 2013 is still producing 11.8 Mmcf/d in its 150th day online, amounting to more than 7 Bcf total.

The Midcontinent produced 84.5 net Mmcfe/d (39% liquids) as part of Range’s horizontal Mississippian Chat program. Five wells were turned to sales and produced average seven day rates of 457 BOEPD (68% liquids). A St. Louis well returned a 24-hour rate of 11,431 Mmcfe/d. The company continues to monitor well performance and is testing larger frac designs. Three rigs are currently in the region and are expected to bring 16 wells online within the fiscal year. RRC management said delineation of the region is in future plans and estimated ultimate recovery is 485-600 MBOE per well.

The southern Appalachia has one running rig and is targeting coalbed methane, tight gas and horizontal Huron Shale wells. Overall production averaged 70 net Mmcfe/d and RRC believes it is strategically placed to benefit from high gas prices in nearby Virginia properties.

Guidance

Range has forecasted line of sight growth of 20%-25% in many of its recent releases, and the trend for 2014 remains intact. Daily production in Q2’14 is expected to reach 1,065-1,075 Mmcfe/d and eventually reach 1,160-1,210 Mmcfe/d in Q4’14. At Q4’13’s midpoint, production would represent a 24% increase compared to Q1’14 totals. Liquids are estimated to make up 30%-35% of the stream. A total of 161 wells are forecasted to go online within the fiscal year, with 22 in the Midcontinent and 139 in the Marcellus. Capital expenditures remain consistent with the $1.52 billion estimate.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.