EnerCom analysts take a look

Advancements in unconventional drilling have fundamentally changed the types of oil and gas projects that attract capital.

When hydraulic fracturing and horizontal drilling unlocked vast hydrocarbon resources onshore in the U.S. shale basins about a decade and a half ago, the business strategy of U.S. E&Ps changed forever. And energy capital formation changed with it. Even with the crash in oil prices that came at the end of 2014, companies have been able to innovate to the point that they can operate profitably, even when oil prices fell back below $50 per barrel.

Oil and gas companies invest capital in projects they believe will create the greatest value possible. Prior to the oil price downturn in 2015 and 2016, international oil companies (IOCs) like Shell (ticker: RDSA), ExxonMobil (ticker: XOM) and ConocoPhillips (ticker: COP) often turned to larger, long-life projects to increase their reserves and to give them line-of-site on sustainable production growth.

Large offshore projects often cost billions of dollars—single wells can cost $120,000,000 to drill—but with Chinese demand continuing to increase, and oil prices in the triple-digits, companies were comfortable making those types of investments, even if they would not see returns for several years.

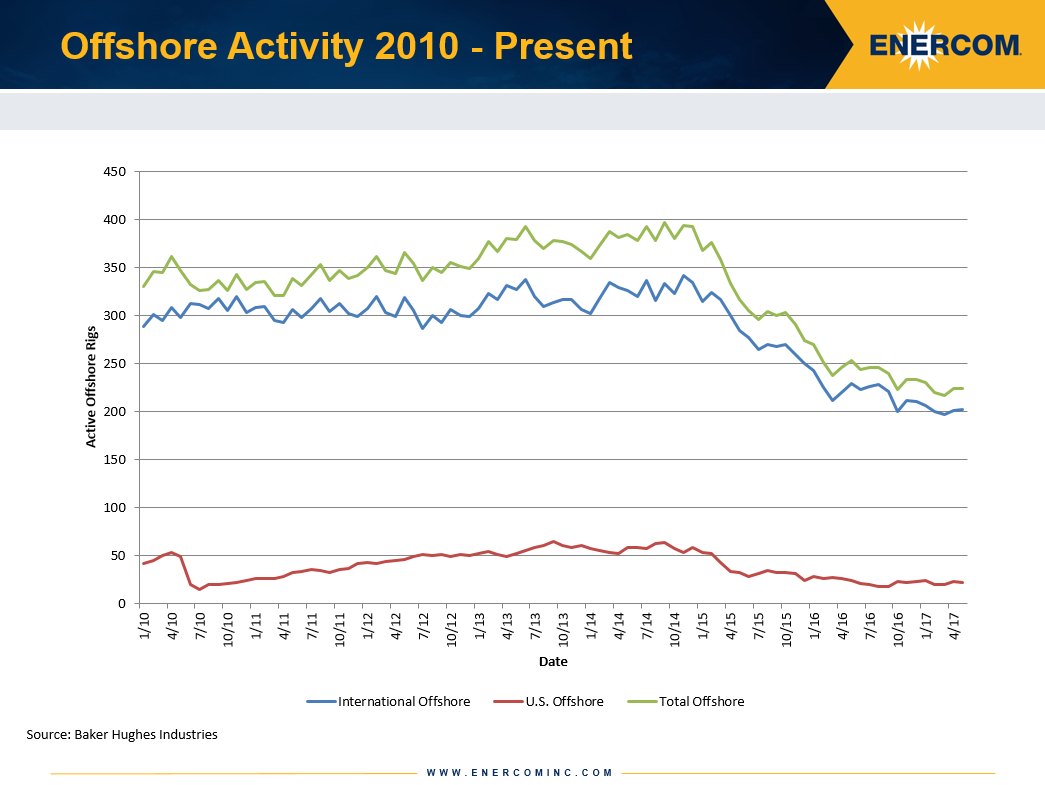

Offshore hit a peak with 394 rigs drilling

In November of 2014, the same month that OPEC made the decision to defend market share which would send oil prices crashing, international offshore drilling was at a peak with 341 rigs, and an additional 53 rigs were drilling offshore the United States. As of May 31, 2017, 202 rigs were drilling in international waters and 22 in North America, representing declines of 41% and 58%, respectively.

Lower commodity prices have made expensive offshore developments far less attractive in terms of absolute returns, but investors have also become increasingly risk adverse, preferring instead to put their capital into projects with faster, relatively predictable returns—the “factory” drilling opportunity of shale. Committing billions of dollars of capital to a project that might not generate returns for several years, if ever, became too much for the industry to stomach. Shell’s venture in Alaska’s Chukchi Sea is a good example. Shell pulled the plug on its Chukchi Sea venture in the Arctic in 2015, writing off more than $4 billion.

While Shell did find indications of oil and gas at the well, “these are not sufficient to warrant further exploration in the Burger prospect. The well will be sealed and abandoned,” Shell said in a statement when it announced the result after years of preparation, permitting and finally drilling its exploratory well in the harsh environment.

In the release about its Burger J well results, Shell also said it “will now cease further exploration activity in offshore Alaska for the foreseeable future. This decision reflects both the Burger J well result, the high costs associated with the project, and the challenging and unpredictable federal regulatory environment in offshore Alaska.”

Greater risk can still equal greater reward

Low oil prices have made offshore development an extremely high-risk proposition for all but supermajors and IOCs, but even they seem to be shying away from deepwater drilling as they look for quicker returns on their investments.

The average cost of a deepwater well targeting the Miocene, which benefits from higher estimated well productivity and relatively shallower reservoir depth compared to other zones, is $120 million. Even assuming the relatively high per-well cost of $8 million for a shale project, a company could drill 15 wells onshore for the same cost as one offshore well, and with much less risk.

Supermajors like BP (ticker: BP) continue forward with some offshore drilling, such as the company’s Mad Dog Phase 2 project, in spite of the risk. The project will consist of 14 wells producing a combined 140 MBOPD, according to the company.

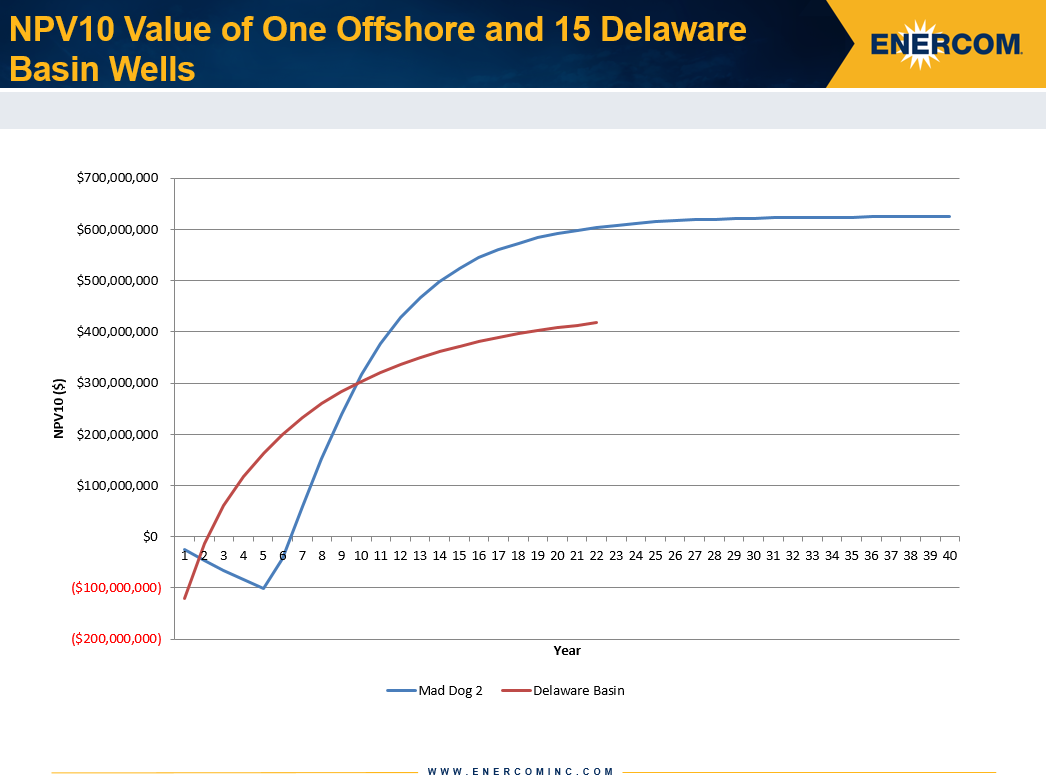

Looking at the net present value discounted 10% (NPV10) of 15 average Delaware Basin wells versus one of the 14 Mad Dog 2 wells, it becomes clear quickly why many companies choose to drill unconventional wells in a market that is cost-conscious and risk-averse. Delaware Basin wells typically pay themselves off in less than two years, making the returns much more immediate when compared to an offshore project like Mad Dog which is not expected to break even for roughly six years.

The cumulative production of an offshore well can offset the cost over time, but given the massive investment required to drill an offshore well compared to an unconventional well, the option is limited to operators who are extremely well capitalized and can absorb the risk and capital outlay.

The cumulative production of an offshore well can offset the cost over time, but given the massive investment required to drill an offshore well compared to an unconventional well, the option is limited to operators who are extremely well capitalized and can absorb the risk and capital outlay.

Given the estimated 35-year lifespan of the Mad Dog 2 project and the company’s reported 140 MBOPD of production, Mad Dog 2’s EUR is approximately 1.8 billion barrels. Through project redesigns and greater efficiencies, BP has lowered the estimated cost of the offshore project 60% to $9 billion, which works out to $5.03 per barrel of oil produced. Even with the Delaware Basin’s strong economics and significantly lower per-well cost, the average of six type-curves found that operators in the region expect to spend approximately $6.73 per BOE they produce.

So what is the verdict?

Looking at Mad Dog 2 over the course of its entire lifespan makes it a more attractive project on a cost-per-BOE basis, but it still cannot replicate the flexibility of shale operations. Once BP decided to make the investment and move Mad Dog 2 forward, it locked itself into a position where it would not be seeing any returns for at least four years.

Shale operators, on the other hand, can react much more quickly to changes in the market, drilling exactly the number of wells they feel makes the most sense at the moment, considering commodity market conditions, their individual balance sheets, access to debt or equity capital, etc.

With oil prices still struggling to move above $50 per barrel, it makes sense that companies would continue to invest money into shale where they can realize faster returns and react with more sensitivity to movements in the market.

Shale has made oil and gas companies much more nimble and unlocked a wealth of hydrocarbons onshore, but it has also made high-risk projects like offshore drilling a much harder sell, despite their stronger long-term economics and potential production volume, according to EnerCom Analtyics.

Taking the two purely on a cost-per-BOE basis, offshore projects such as Mad Dog 2 have stronger economics, but given the markets weariness of high-risk projects, shale will continue to attract CapEx dollars of the industry’s decision makers for now.

The shifting realities of a cyclical market

The massive resources unlocked by shale will likely continue to hold a dominant position in the makeup of North American oil and gas development, but it is important to remember that the big picture is always in flux.

The lack of investment in offshore projects over the last three years has many pointing to an upward correction in oil price. Paal Kibsgarrd, CEO of Schlumberger (ticker: SLB), believes that production levels have remained high since 2014 mostly through a greater reliance on existing wells, rather than through new exploration, which will eventually lead to a supply shortage as dwindling reserves are unable to match growing demand.

Others believe that prices will have to get worse before they get better. According to Bank of America Merrill Lynch technical strategist Paul Ciana, oil is headed lower. “Oil is in a downtrend and risks trending into the $30’s,” Ciana said in a research note last week.

If Ciana is correct, that level of per-barrel price for oil, if sustained over a longer period, would make it tough for both onshore and offshore operators, leading to a slowdown in drilling, followed by a drop in oil production in a year or two, leading to supply shortages the following year, followed by higher oil prices. With OPEC seemingly unable to recapture its role as swing producer, these cycles of supply and demand playing catch up with one another could prompt E&Ps to focus their capital on different types of projects in the future, if the realities of the market change significantly from where they stand today.