RPC, Inc. (ticker: RES) provides specialized oilfield services and equipment to independent and major oilfield companies. The Company’s services include snubbing services, coiled tubing services, pressure pumping services, marine services, firefighting and well control, and rental of drill pipe and other equipment.

Recent Financial Results

RPC announced year-over-year increases in revenue, operating profit, net income and EBITDA in its Q1’14 earnings release on April 23, 2014. The company says higher drilling activity and increased service needs contributed to the increase.

Compared to Q1’13, RPC increased revenue by 18% ($501.7 million from $425.8 million), operating profit by 14% ($65.2 million from $57.2 million), net income by 12% ($39.4 million from $35.1 million) and EBITDA by 9% ($120.8 million from $110.6 million).

Services Overview

RPC operates in two business segments: technical services and support services.

The technical side includes managing oilfield services to increase flow rates from oil and gas wells. Other aspects, such as pressure pumping and well control, are also a part of maintaining this segment. Technical services revenue increased 18.5% compared to Q1’13, primarily due to higher levels of pressure pumping. In all, the technical aspect accounted for 93% of total revenue in Q1’14, with pressure pumping contributing roughly 57% of all revenue from consolidated service lines.

The support side of RPC’s service business including inspections and equipment rentals increased 9% for the same time period. The increases are attributed to larger amounts of rentals as part of the increase in service activity. RPC’s support segment is only a minority (7%) of its revenue stream as the company aims to operate the bulk of its equipment.

Source: RPC March 2014 Presentation

Additional Details

Management said, despite the revenue increases, total returns were constrained by approximately 5% due to freezing conditions in January and February. RPC experienced higher than normal pressure flows in March to offset the tightened gas markets, but were not enough to completely offset the effects from the inclement weather. However, management said operations in March were “extremely strong” and revenues from the month contributed to more than 40% of revenue for whole quarter, according to comments made in a conference call following its earnings release. The increased activity continued into April but the company declined to release exact revenue amounts.

An important indicator of services demand can be traced to the unconventional rig count, says RPC. The rig count in Q1’14 is 5.7% higher than the count in Q1’13. Gas prices rose by 27% overall on a quarter over quarter basis, increasing industry demand and therefore the need for RPC’s services.

Richard A. Hubbell, RPC’s President and Chief Executive Officer, said United States E&Ps are improving drilling efficiency, further boosting hydrocarbon flow in addition to the higher rig count. The greatest increase has occurred in the Permian – home to the majority of RPC’s pressure pumping fleet. The company also expects normal transportation methods via rail to resume in 2014 after delays resulted in slightly reduced profit margins for the quarter.

Balance Sheet

Source: RPC March 2014 Presentation

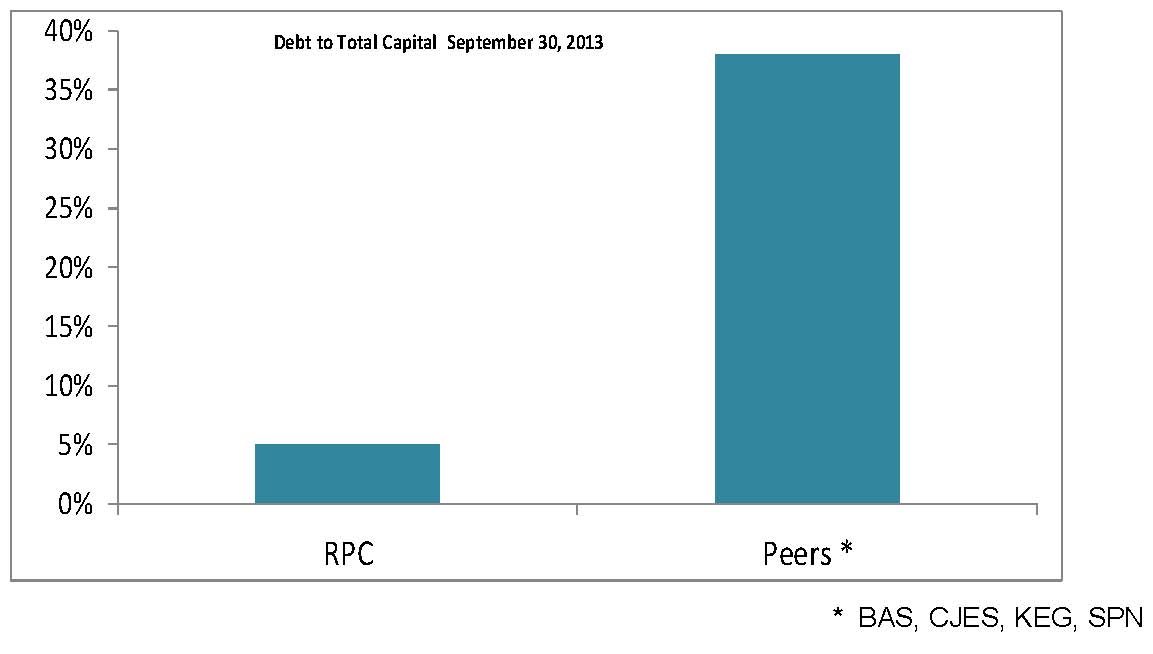

Market conditions in 2013 limited RPC’s need to grow its fleet, so the company instead spent $38 million for maintenance during Q1’14. The company’s all-around approach to the OFS market has allowed compounded annual revenue growth rate to climb by 17% since 2001. Its debt has remained below 10% of its $4 billion market cap since late 2012 and currently sits at a ratio of 7.6%. The company repurchased nearly 400,000 shares in Q1’14 and declared a cash dividend of roughly $0.10 per share payable in June 2014 as part of ongoing efforts to boost value to its shareholders.

In the earnings conference call, management said RPC’s low debt allows it to maintain its fleet – a serious problem for several of its smaller, capital-restricted competitors. The company projects to spend a total of $375 million in fiscal 2014, with the bulk of expenditures focusing on increasing pressure pumping horsepower. The additional power will become fully operational in 2015. Management said 50 pumps are in the process of being refurbished and will assist the company’s growth in a surging Permian Basin market. The serviced pumps will be operational by the end of 2014.

Final Thoughts

Natural gas inventories are at their lows providing the OilService segment an opportunity to capture additional E&P spending as companies potentially begin ramping up drilling operations in natural gas basins to take advantage of an inflated price. As of April 18, 2014, natural gas inventories held 899 Bcf – approximately half of the natural gas inventory level at this point in 2013. With cold weather delays behind them, we believe the remainder of 2014 should be a busy time for the OS sector.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication.