Sanchez Energy Corporation (ticker: SN) is a growth-oriented independent exploration and production company focused on the exploration, acquisition, and development of oil resources in the onshore U.S. Gulf Coast with a current focus on the liquids-rich Eagle Ford Shale, Austin Chalk and Tuscaloosa Marine Shale (TMS). SN is currently producing 19.5 MBOEPD, coming in on the high side of its Q1’14 guidance estimates of 18 MBOPED to 20 MBOEPD. Full year guidance for 2014 is expected to average 21 MBOEPD to 23 MBOEPD, which is roughly double 2013’s average of 10.6 MBOEPD.

Efficiencies Lead SN to Reduce 2014 CAPEX Budget

Sanchez’s knowledge and efficiency in the Eagle Ford and recent shift from exploration to a manufacture-style pad drilling strategy has caused production to grow rapidly and costs to shrink. Overall, production in 2014 is expected to double and SN has already realized a 30% decrease in total well costs across its areas.

When a company announces a reduction in its 2014 CAPEX budget, it’s usually interpreted that they expect a decrease in production and/or a decrease in the amount of spud wells or wells placed on production. SN, however, is the exception.

On March 25, 2014, SN revised its 2014 capital expenditures downward to $600 to $650 million from $650 to $700 million.

Despite the decrease in capital, however:

- SN still estimates it will grow its 2014 average production to between 21,000 and 23,000 BOPD, an increase of 100% from its 2013 average.

- Additionally, the company reaffirmed plans to spud 70 net wells and complete 70 net wells.

Finally, well costs are averaging between $5.5 million to $8.5 million across SN’s entire Eagle Ford footprint. This is significantly lower than its initial $11 million to $14 million.

How are they achieving these results?

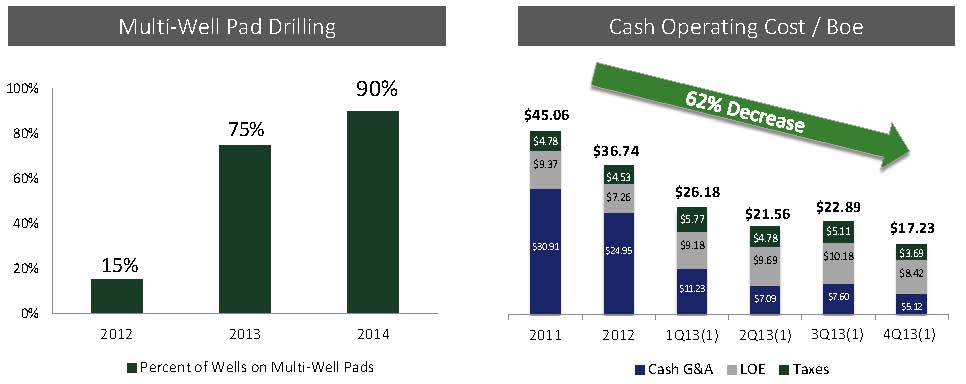

- Approximately 90% of its wells to be on multi-well pads in 2014, up from 75% in 2013.

- The increase in multi-well pads has allowed SN to achieve a 40% decrease in drilling time from spud to total depth and a 35% increase in average footage drilled per day.

- On average SN has doubled the number of frac stages pumped per day and seen services costs continue to decline due to the use of zipper fracs on its multi-well pads.

Final Thoughts on Sanchez

Well positioned. There’s not much better than reducing costs while rapidly growing production in the nation’s largest oil producing shale play.

Well funded. Sanchez currently has $154 million in cash on hand with an additional $325 million in undrawn funds from its credit facility. The company holds an option to increase its borrowing base to $400 million but we do not anticipate SN will increase it any time soon. SN’s 2014 capital plan is expected to be fully funded from a combination of internally generated cash flow, cash on hand and modest borrowings under its current credit facility.

Future upside. The sixth and final pilot well at Prost O-1 has been drilled and SN believes there is potential for a multi-horizon resource play, based on data from wire logs. Sanchez is concentrated on the Lower Eagle Ford in this region and has realized pay zones of 25-40 feet in thickness. The Upper Eagle Ford has shown similar thickness and management believes the Austin Chalk formation also holds potential. Both of the latter formations are expected to be appraised in 2H’14.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.