Sanchez Energy (ticker: SN) revised its 2015 volume guidance by 2 MBOEPD as a result of higher than expected production volumes and wells tracking above estimated ultimate recovery (EUR) rates, the company said in its Q1’15 earnings release. The Eagle Ford-focused E&P now expects 2015 production to average 42 to 46 MBOEPD, up from initial estimates of 40 to 44 MBOEPD. This includes the recent asset transaction of 1 MBOEPD to Sanchez Production Partners (ticker: SPP), its master limited partnership vehicle.

Q1’15 volumes, released separately from its financial results, were finalized at an average of 45.2 MBOEPD. The company’s official Q1’15 results were released roughly three weeks later, and production has climbed to a record of 50 MBOEPD (72% liquids). The surging volumes led to management boosting its 2015 guidance. Its current production rate is more than 83 times greater than its 0.6 MBOEPD of volumes when the company filed its initial public offering in December 2011.

Low Well Costs Provide Significant Upside

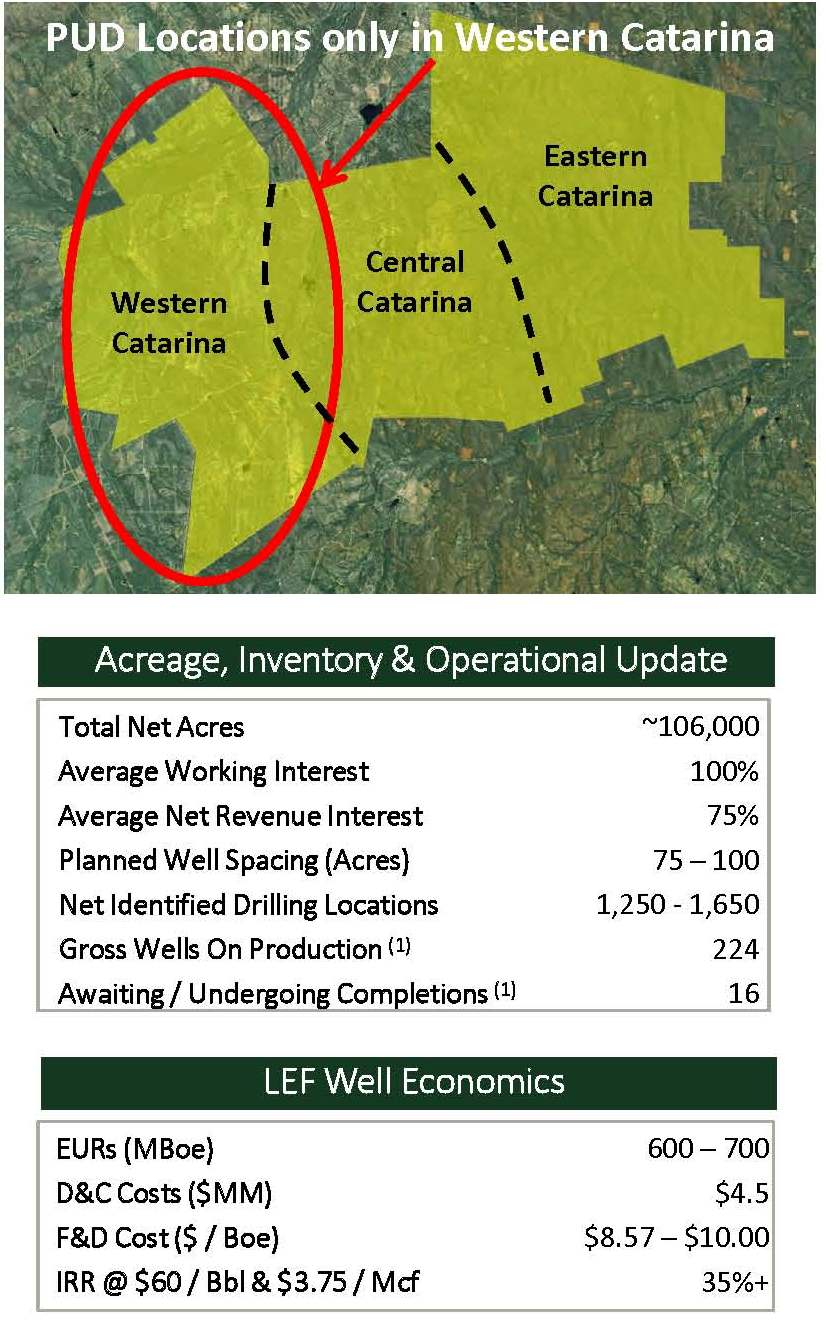

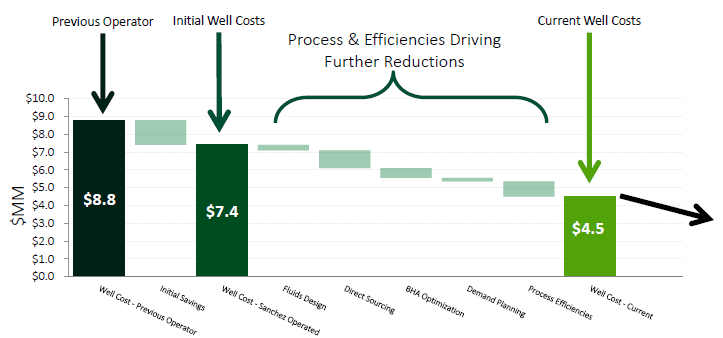

SN has three core areas in its Eagle Ford acreage; Catarina, Marquis and Cotulla/Wycross. Completed well costs in all regions are below $5.0 million, and are anywhere from 30% to 40% below costs from Q4’14.

Sanchez has been operating in the Catarina for roughly one year since it was acquired from Royal Dutch Shell (ticker: RDS.B), but has already established type curves of up to 700 MBOE on costs of only $4.5 million per well. Recent wells drilled on the western portion are tracking 20% above the type curves, while two 8,250 foot extended laterals in the region are tracking EURs of 1,500 MBOE per well.

Significantly Extended Laterals

Significantly Extended Laterals

“We’ve been pushing our average lateral lengths consistently higher. Our average lateral length is now over 6,200 feet versus the previous operators have just barely over 5,000,” said Chris Heinson, Chief Operating Officer of Sanchez, in a conference call following the release. “Now that we have some test with some longer laterals, we see the ability to actually go out there and actually improve the rates of returns and areas that may not be commercial today by using these techniques.”

The success on the longer laterals was a common theme on analyst reports. Capital One Securities explained: “Mgmt estimated long lateral wells cost ~$6.0MM, implying an F&D cost of $4/boe. This compares to a 600 – 700 Mboe EUR assumption for standard length (6,200 – 6,500’) laterals that currently cost ~$4.5MM or below, implying an F&D cost of ~$7/boe. For perspective, if we raised our Catarina EURs by 20% it would increase our NAV by ~$5/sh.”

Johnson Rice & Co. said Sanchez’s Middle Eagle Ford wells are exceeding the rates of the previous operator by more than 40% – a result of changing the completion design. “The early performance of Sanchez’s operated wells are significantly better than assumed in its acquisition case, driving increased production guidance and changing the opinion of many that doubted the attractiveness of that acquisition last summer,” the note said.

The Hotspot

“Our experience to date with Catarina leads us to believe that strong performance can be sustained going forward,” said Tony Sanchez III, Chief Executive Officer and President of Sanchez Energy, in a conference call following the release. Catarina accounted for 60% of the company’s production in Q1’15. Appraisals are underway on the eastern Catarina, and management believes the potential of its 37,000 net acres are “encouraging.” Two additional appraisal wells in the Southeastern corner are expected to be online in the upcoming quarter.

“With regards to our appraisal and development at Catarina, we’re becoming increasingly confident in our ability to develop the Lower Eagle Ford and Middle Eagle Ford across the majority of Western Catarina,” said Chris Heinson, Chief Operating Officer of Sanchez, in the call. “Additionally, in the Northwest region of Catarina, recent well results have provided evidence that a third bench can be targeted in the Upper Eagle Ford.”

Catarina production has more than doubled since SN completed the acquisition nine months ago. Sanchez’s rapid growth is evident in EnerCom’s Weekly Benchmarking Report; its 3-year Production Replacement of 927% ranks tenth among its 88 peers and is well above the median of 358%.

Focus in 2015

Sanchez’s primary 2015 focus will be on its Catarina and Cotulla/Wycross assets. A total of 42 wells (29 operated) were brought online in the quarter, and SN now has a total of 549 gross producing wells throughout its acreage, with all but 13 in the Eagle Ford Shale. A total of 322 gross wells have been added to its portfolio since Q1’14 (146 gross wells from existing operations). SN management said it has more than 10 years of “high return drilling opportunities” if development continues at its current pace.

The Marquis asset, its third Eagle Ford focus area, is largely held by production and any future production will likely not occur until 2016.

Q1 Results

Sanchez reported a net loss of $501.3 million in Q1’15, including a non-cash impairment charge of $441.5 million. Revenues of $110.6 million declined 18% compared to Q1’14, even though the average sales price per BOE (including the realized impact of derivative adjustments) declined by 56%.

The company spent $213 million in Q1’15 and anticipates spending a total of $600 million to $650 million throughout the fiscal year. SN has $645 million in liquidity as of March 31, 2015, with $345 million in cash and an elected commitment of $300 million on its $550 million borrowing base. Approximately 58% of anticipated production rates are hedged at a floor of $60/barrel in 2015.

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.