Oil traders experienced a moral victory today, witnessing West Texas Intermediate (WTI) close at $52.13 – the highest since January 5, 2015. The spot price has rebounded 17% in less than a week, dating back to the closing of $44.45 on Wednesday, January 27.

A note published this morning by Stifel provided more bullish forecasts for investors, and even upgraded or raised price targets on nine E&P companies. The investment firm believes declining rig counts, which are down 24% from October, will eventually slow United States supply growth and ultimately allow demand to recover. A total of 199 rigs have been laid down in the Bakken, Eagle Ford and Permian plays in the same time frame.

“One of the major problems was that supply growth was contributing to an oversupplied market, but with the rig count declining significantly, that part of the problem is getting fixed,” said Mike Scialla, Managing Director for Stifel, in an interview with Oil & Gas 360®. The firm expects the “global market, to slow, if not stall, during 2H15,” according to the note. The oversupplied market is apparent: U.S. crude stockpiles are currently the highest on record.

Scialla believes the volatility of E&P stocks will continue through earnings season even though share values experienced a spike today. “I don’t think we’re completely out of the woods, but I think there’s sight of a light at the end of the tunnel,” he said.

Inventories are the Indicator

Scialla warned last week’s inventory build of more than 8.8 million barrels may harbinger of things to come over the next several weeks. The Energy Information Administration reports total gains of more than 24.3 million barrels in the last three weeks – the most since March 2001. He explains that there is still too much oil in the market and will contribute to significant downward pressure on prices, especially with earnings season ramping up.

Stifel believes the trend could persist throughout the first half of 2015 and push WTI prices below $40/barrel, considering global supply is outstripping demand by roughly 1.5 million barrels. Iraq has also catapulted into the second-largest producer of OPEC, producing an all-time high of 4 MMBOPD in December 2014. The increasing Iraqi volumes could offset the potential pullback in U.S. production.

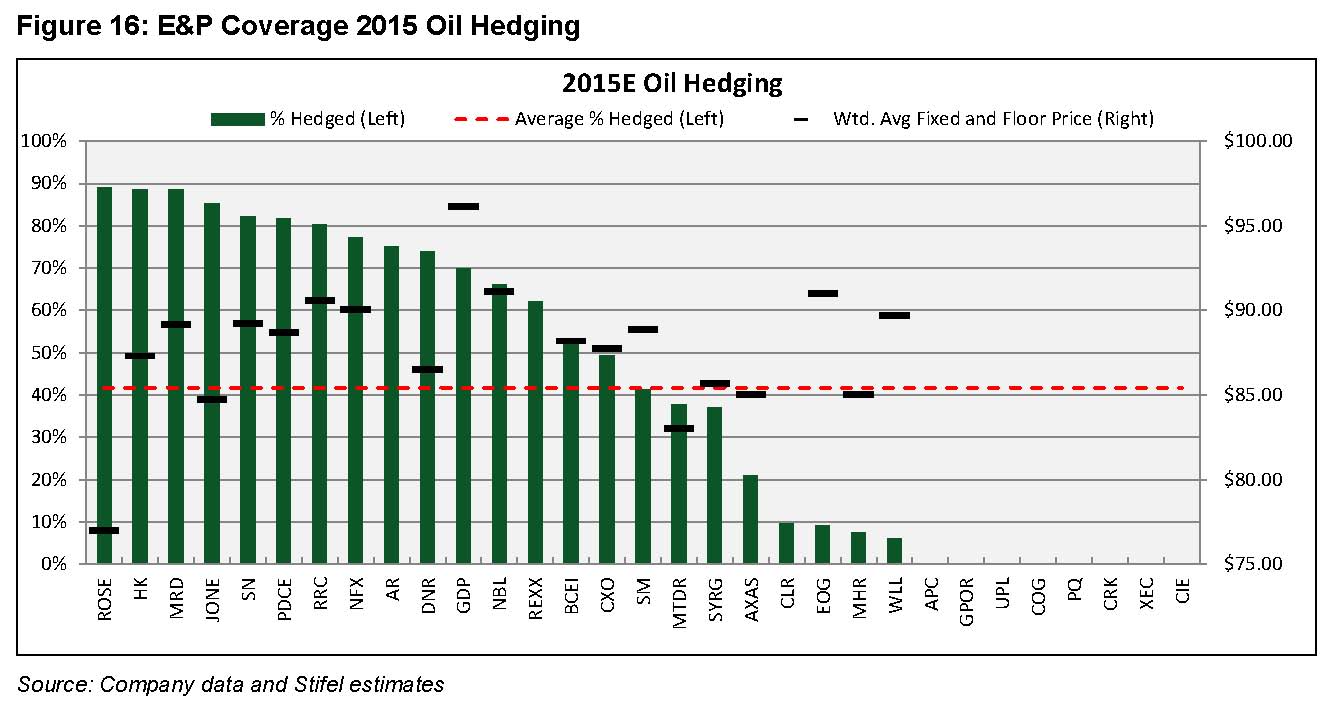

Bullish Outlook for Certain E&Ps

Stifel either upgraded or raised the target price of nine E&Ps in the release, assuming WTI prices reach the firm’s projection of $65/barrel in 2016. Beneficiaries of Stifel’s upgrade include Synergy Resources (ticker: SYRG), PDC Energy (ticker: PDCE) and Whiting Petroleum (ticker: WLL). While Scialla says WLL’s stock carries high risk, the Williston Basin’s largest producer is equipped to survive the current environment. “When they bought Kodiak Oil & Gas, they took on their debt and they didn’t have any hedges in place, but I believe their asset base is exceptional and will help them survive this downturn,” he said.

Scialla and the Stifel team also believe the “vast majority” of the downward move in WTI and Brent prices is attributable to the strength of the dollar. But that strength has a shelf life, says Stifel, and will potentially top out and begin to weaken within the next 12 to 18 months. “If the dollar does roll over, it should help both commodities,” said Scialla. “I can then see the WTI/Brent spread widening back out if U.S. inventories continue to build, since they can grow more quickly than other inventories.”

While oil prices are beginning to lean towards a recovery, Stifel does not expect WTI prices to long-term forecast of $80/barrel (WTI) for at least two years. Companies may start to become financially strained if current price levels extend into the second half of 2015. In a trickle-down effect, the firm believes well costs may decline as much as 20% due to deflation in oil field services. Companies who are well hedged, at least in the near term, are provided some insulation from the current market.

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.