Synergy Resources (ticker: SYRG) is approaching the ownership of 100,000 net acres in the greater Wattenberg area, aided by the purchase of 4,300 net acres on September 15, 2015.

The Platteville, Colorado exploration and production company secured the acreage in a deal with privately held K.P. Kauffman Company, Inc., for $78 million, consisting of 4.4 million SYRG shares and $35 million in cash. The properties are currently producing net volumes of 1,200 BOEPD from five net wells (25 gross), and the transaction is expected to close no later than October 30.

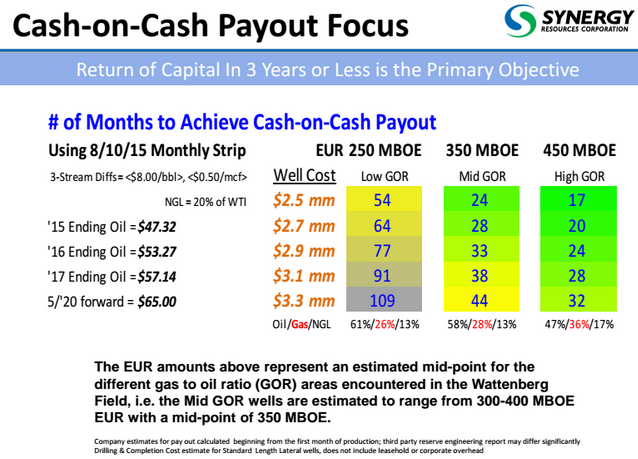

Wattenberg Acreage Valuations

Johnson Rice & Co. was particularly impressed with the acquisition, saying a high gas/oil ratio (GOR) mix would break down the valuation to $6,600/acre. “Needless to say, this is a strong price, especially for Mid/High GOR acreage, which has the quickest paybacks in the basin (17-24 months),” the firm said. Stifel models Middle Core Wattenberg type curves at 300 MBOE

SunTrust Robinson Humphrey pointed out that the deal is “within range of basin transactions though at the low range of prior Synergy deals closer to ~$7-13k/net acre.” Synergy’s last acquisition, excluding deals upping its working interest, occurred in December 2014, when the company paid $125 million for 4,053 net acres and 1,200 BOEPD.

Capital One Securities said the $7,500/acre price tag for the undeveloped acreage is far above its valuation of $3,200/acre for Bonanza Creek (ticker: BCEI), who operates nearby. Noble Energy (ticker: NBL) is also a neighboring operator and recently increased its horizontal volumes from the Wattenberg by 30% on a year-over-year basis.

2015 In Review

Synergy posted average production of 8,700 BOEPD in fiscal 2015, which ended on August 31. The rate is 47% greater than 2014’s fiscal average of 5,894 BOEPD – fueled by drilling 46 gross operated wells in the time frame. A total of 38 net wells were brought online in 2015 while an additional 12 wells are in its inventory. Four laterals with lengths of 7,200 feet are expected to be complete by the end of December.

The company estimates production from Q4’15 will approximate 10,800 BOEPD. In order to maintain a flat production profile for 2016, the company plans on running a one rig program at an estimated cost of $120 million. This compares to July guidance that estimated 2016 capital expenditures of $250 to $300 million. No further information was given on its 2016 guidance, but declining well costs ($2.5 million on its latest pad, down from $3.7 million in April 2014) may factor into possible capex adjustments.

SYRG is already in a favorable financial position according to EnerCom’s E&P Weekly Benchmarking Report; its debt to market cap is only 14%, coupled with an EBITDA margin of 73%. Green Hunter Securities endorsed SYRG’s one rig program in a note, saying the proposed scale-down results in “a minimal outspend and a balance sheet likely to be the most unlevered in the space.” The firm believes SYRG’s net debt/EBITDA could be below 0.25x by year-end 2016, leaving the window open for future consolidations. Irene Haas, Senior Research Analyst for Wunderlich Securities, described Synergy as “one of the most iron-clad names in our universe, and a company that we believe is well positioned to emerge from this downturn bigger and better.”

The company is scheduled to discuss its Q4’15 results via conference call on October 16, 2015.