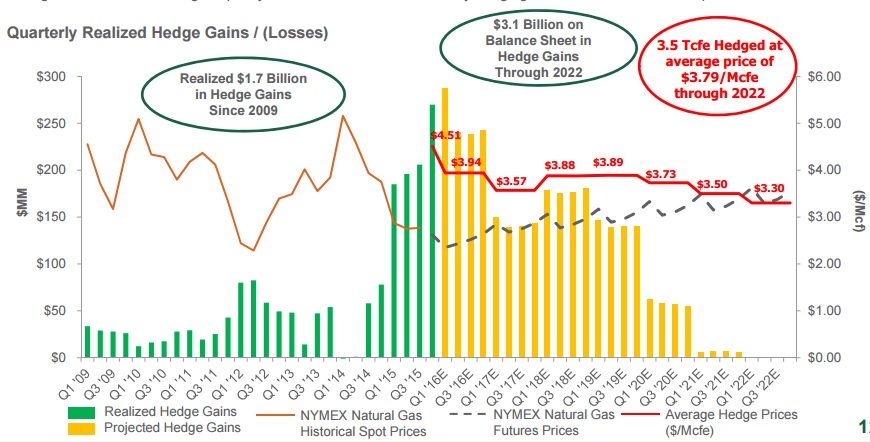

Hedge book’s mark-to-market value listed at $3.1 billion

Attractive hedges have the ability to make a significant impact on company balance sheets, and its positive effects (along with access to favorably priced markets) are apparent in a January 13 business update from Antero Resources (ticker: AR).

The Appalachia-focused producer reported a realized natural gas price (after settled commodity derivatives) of $4.40/Mcf in Q4’15 – a staggering $2.13 positive differential to Nymex spot prices. The favorable prices come at the perfect time, as Antero boosted its overall dry gas production by 18% compared to the prior quarter and virtually the same amount as Q4’14. Management attributed the increase to the commissioning of the Stonewall gathering pipeline in December, opening up lanes for AR to sell “virtually all of its gas to favorably priced markets.” The Stonewall created a negative differential to Nymex of just ($0.14), compared to December differentials in the range of ($0.80) compared to data compiled from EnerCom’s Monthly Report.

The hedge position “enables the projected 20%+ growth in 2016 despite the otherwise dismal pricing,” said a note from Capital One Securities.

The hedge position “enables the projected 20%+ growth in 2016 despite the otherwise dismal pricing,” said a note from Capital One Securities.

If It Ain’t Broke, Don’t Fix It

In association with the announcement, Antero revealed an increase in its hedge position to 3.5 Tcfe through 2022 at an average fixed price of $3.79/Mcfe. The mark-to-market value is listed at $3.1 billion and is believed to be the largest gas hedge position in all of U.S. E&P. That doesn’t include $1.7 billion of realized gains since 2009.

AR hedged 94% of its 2015 production guidance at $4.43/Mcfe, and is only increasing the book in the near term. In a January 2016 company presentation, Antero says 100% of its 2016 volumes are hedged at $3.94/Mcfe. Exact details on 2017 figures have not yet been released since AR has yet to release volume figures, but 2,073 Mcfe/d (roughly 58% higher than 2015 volumes) are locked in at $3.57/Mcfe. With the help of the Stonewall and Mariner East 2 gathering pipelines, AR believes 95% of its sales volumes have the inside track to favorable markets.

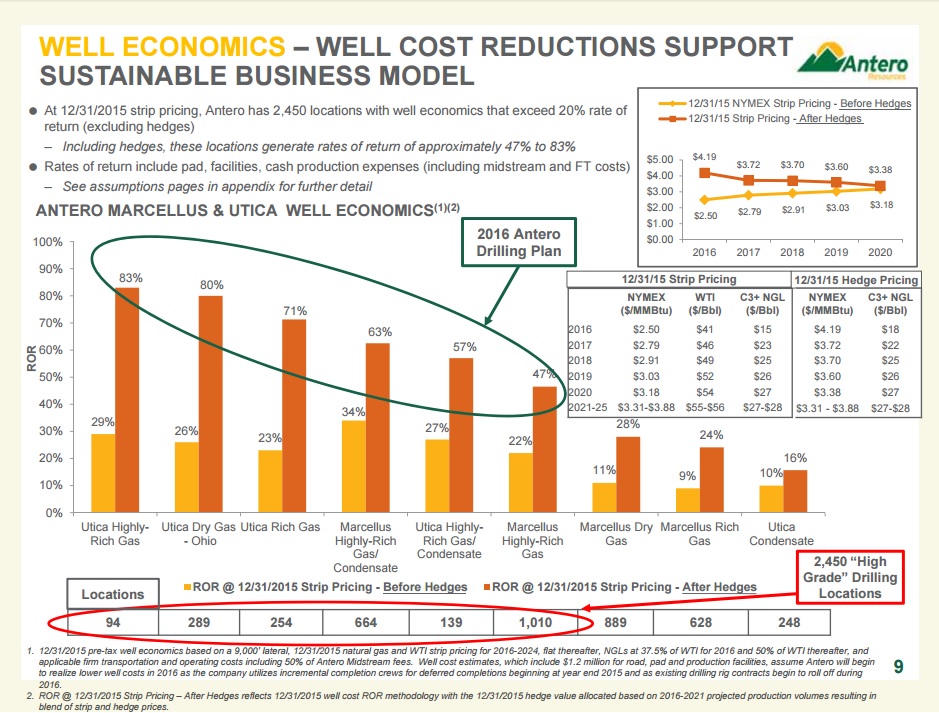

As seen in the well economics slide below, three of the nine Marcellus/Utica regions realize more than triple the price due to hedge benefits. AR is keying in on those area and was the most active regional producer, in terms of rig count, in H2’15.

Can Improvements be Made?

A note from Seaport Global Securities points out that the premium from more favorable markets “is largely offset by increasing FT costs (~$0.35/Mcfe in 2015 goes to $0.46/Mcfe in 2016) and increasing FT commitments (AR expects ~1.5 Bcfpd of excess capacity in 2016).”

In a study of seven Marcellus/Utica producers, analysis from EnerCom and Oil & Gas 360® revealed that Antero’s cash and F&D costs per Mcfe were the highest of the group. Its rapid growth stage carries some of the blame for the costs, but the growth stage is now leveling off and efficiencies are coming to the forefront. Its expenditures for 2015 are nearly half of the amount from 2014, and volumes have not suffered from the difference in activity.