LONDON – Oil prices fell sharply on Monday, with U.S. crude briefly dropping below $20 and Brent hitting its lowest in 18 years, on heightened fears that the global coronavirus shutdown could last months and demand for fuel could decline further.

Source: Reuters

Brent crude, the international benchmark for oil prices, was down $1.98, or 7.9%, at $22.95 by 1337 GMT, after earlier dropping to $22.58, the lowest since November 2002.

U.S. West Texas Intermediate (WTI) crude was $1.31, or 6.1%, lower at $20.20. Earlier in the session, WTI fell as low as $19.92.

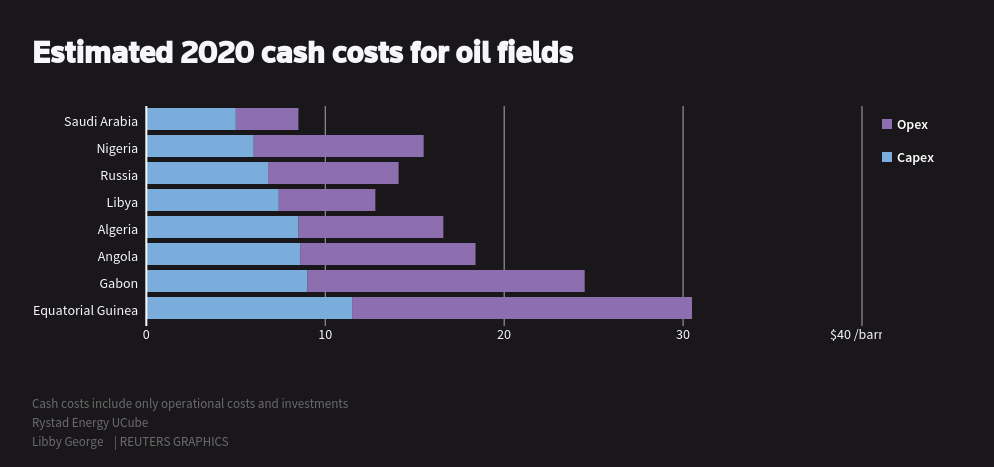

The price of oil is now so weak that it is becoming unprofitable for many oil firms to remain active, analysts said, and higher-cost producers will have no choice but to shut production, especially since storage capacities are almost full.

“Global oil demand is evaporating on the back of COVID 19-related travel restrictions and social distancing measures,” said UBS oil analyst Giovanni Staunovo.

“In the near term, oil prices may need to trade lower into the cash cost curve to trigger production shut-ins to start to prevent tank tops being reached,” he added.

GRAPHIC: Oil prices – here

Rystad Energy’s head of oil markets, Bjornar Tonhaugen, said: “The oil market supply chains are broken due to the unbelievably large losses in oil demand, forcing all available alternatives of supply chain adjustments to take place during April and May”.

These included cutting refinery runs and increasing onshore or offshore storage, he said.

Supertanker freight rates are rising for a second time this month as traders rush to secure ships for storage.

Goldman Sachs analysts said demand from commuters and airlines, which account for about 16 million barrels per day of global consumption, may never return to previous levels.

Besides the demand shock, the oil market is also under pressure from a price war between Saudi Arabia and Russia, after the collapse earlier this month of a three-year deal to limit supply between the Organization of the Petroleum Exporting Countries (OPEC) and other producers led by Moscow.

U.S. President Donald Trump said he planned to speak with Russian President Vladimir Putin on Monday.

He said that Saudi Arabia and Russia “both went crazy” following the collapse of the deal to cut output, as oil prices were pushed down by an economic slowdown caused by the need to slow the spread of the coronavirus.

Saudi Arabia said on Monday it plans to boost its oil exports to 10.6 million barrels per day from May.

“This game of attrition is likely to drag prices even lower and even a price of $10 per barrel is no longer unimaginable,” said Hussein Sayed, analyst at FXTM.

Collapsing oil prices have left some African producers facing lost revenue when they most need it to tackle coronavirus.

Sovereign wealth funds from oil-producing countries mainly in the Middle East and Africa are also on course to dump up to $225 billion in equities.

The contango spread between May and November Brent crude futures reached its widest ever at $13.45 a barrel, while the six-month spread for U.S. crude broadened to minus $12.85 a barrel, the widest discount since February 2009.

In a contango market prompt prices are lower than those in future months, encouraging traders to store oil for future sales.

GRAPHIC: Estimated 2020 cash costs for oil fields – here