RPC, Inc. (ticker: RES) provides specialized oilfield services and equipment to independent and major oilfield companies. The company operates in two business segments: technical services and support services. Its Q2’14 results, announced on July 23, 2014, reported quarterly revenue of $582.8 million (a company record), operating profit of $103.0 million and net income of $63.3 million ($0.29 per share). All segments represent increases on both a quarter-over-quarter and year-over-year basis.

On a H1’14 basis, total revenues for 2014 are $1,084 million – 23% higher than H1’13. Operating profit for the same period is $168.8 million and net income is $102.7 million, which represent respective increases of35% and 36% in comparison to 2013. In a conference call following the release, management said 40% of its fleet is operating on a 24-hour basis.

The Key: Unconventional Drilling

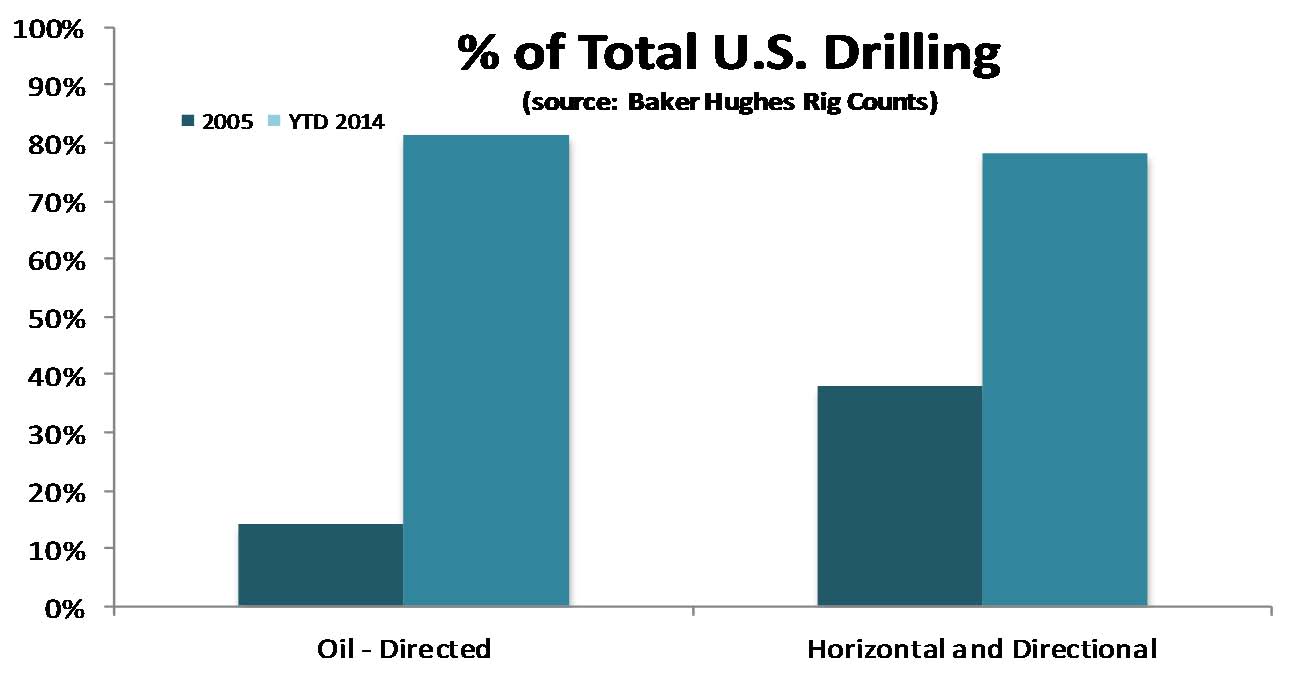

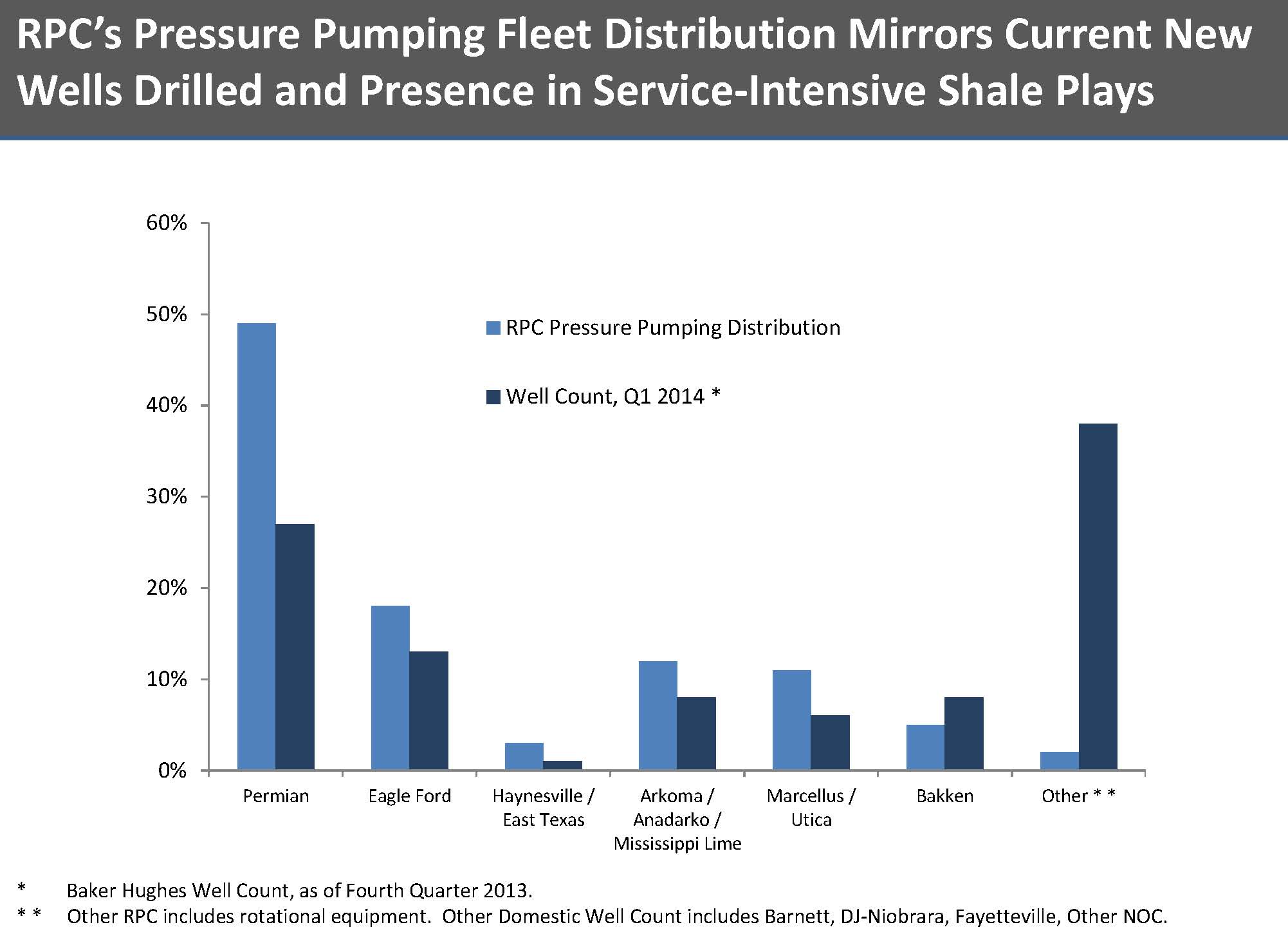

“The unconventional rig count, an important indicator of the demand for RPC’s services, increased by 11.6% compared to the prior year,” said Richard A. Hubbell, President and Chief Executive Officer of RPC. “During the second quarter of 2014 unconventional drilling represented 78.7% of U.S. domestic drilling activity. Our revenues increased by a greater rate than these industry indicators because of our presence in strong domestic oilfield markets such as the Permian Basin and the increasing service intensity of completion work in most of our markets.”

According to Baker Hughes’ (ticker: BHI) Rig Count Summary, both unconventional drilling and Permian activity continue to rise. For the period ended July 18, 2014, unconventional rigs currently account for 80.4% of all United States operations, which surpasses 2013’s mark of 75.6%. A total of 556 rigs are running in the Permian, which is 88 (or 16%) more compared to the same date in 2013. Total Permian activity accounts for nearly 30% of all U.S.-based operations.

In the conference call, Hubbell said: “The transition to more unconventional completion work in (the Permian) creates more opportunities for RPC’s services to be on location longer. We anticipate this recent and favorable development will continue.”

Unconventional Forecast: Up

A feature article by Platts in December 2013 uncovered predictions and estimates from analysts and upstream experts – many of which 2014 will continue to ramp up operations, particularly in the Permian. Barclays projected upstream companies will spend a total of $156 billion in 2014 development, an increase of 8% compared to 2013. The 2014 Annual Energy Outlook, published by the Energy Information Administration, believes unconventional production will increase until the year 2021 and top out at annual production of 4.8 MMBOPD. The projected total would more than double 2012’s rate of 2.3 MMBOPD and would represent more than half of overall U.S. production.

RBC Capital Markets believes horizontal well count will increase by 8% and 7% in 2014 and 2015, respectively. The group expects horizontals in the Permian to jump by 30% in 2015.

Financially, RPC is well positioned to move forward in both unconventional operations and the Permian. RPC’s total debt of $131.4 million is low compared to its peers, according to EnerCom’s OilService Weekly for the period ended July 18, 2014. Its debt to market cap ratio of 2.5% is well below the industry median of 17%, which takes into account 59 other service companies.

“We remain conservatively capitalized both by our historical standards and relative to our peers and we have plenty of capacity for our fleet expansion and additional working capital requirements as they may arise,” said Ben Palmer, Chief Financial Officer of RPC.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.