Down more than 50% Year to Date

Down more than 50% Year to Date

Oil and gas companies are tightening the purse strings for 2015, as several news releases on guidance are showing capex declines of 20% or more. Commodity hedges may protect most companies from further capital deterioration for the time being, but repercussions from the oil price collapse will be truly felt once the hedge contracts begin to expire. For some companies, that time is only a few months away.

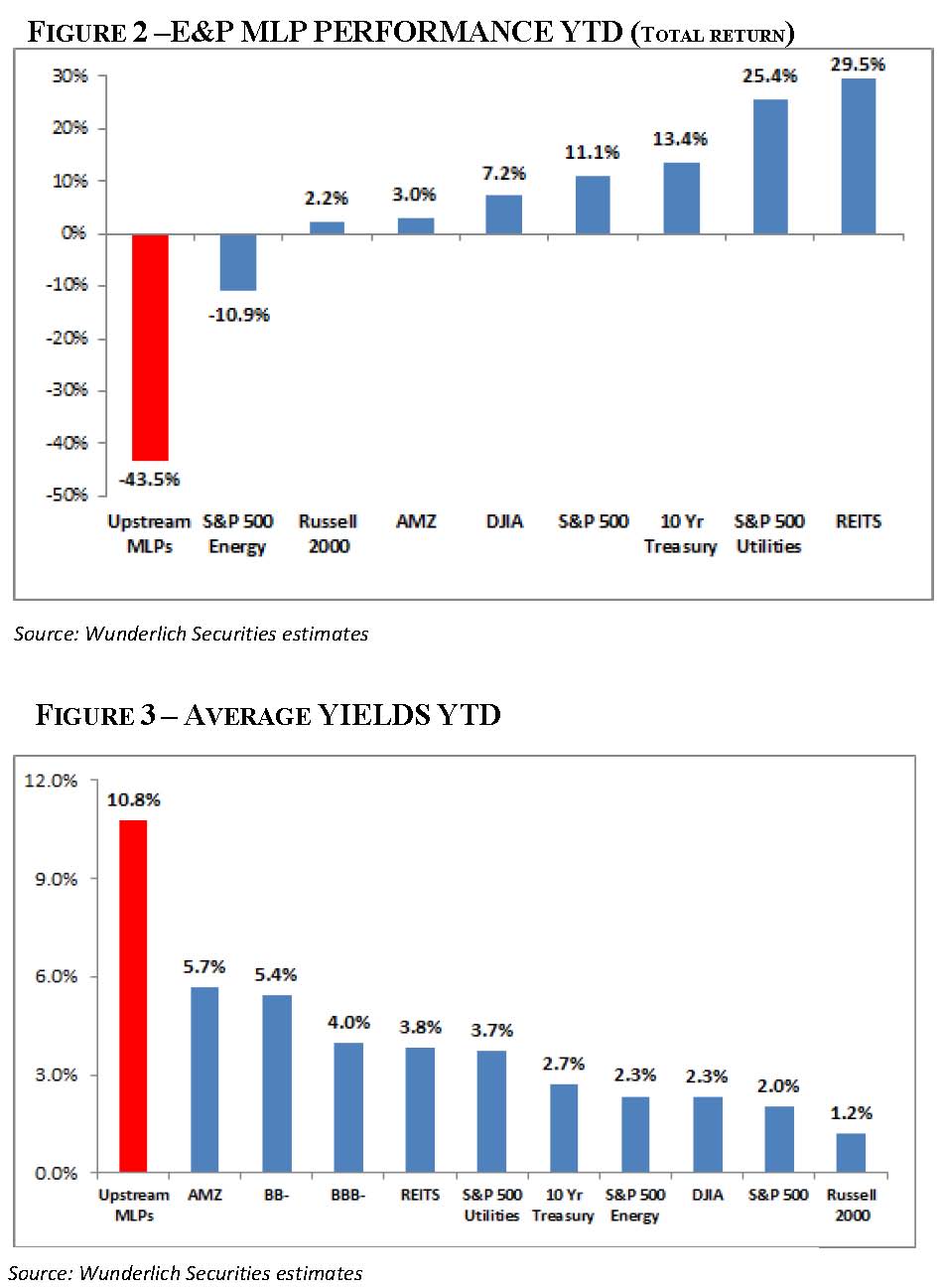

Groups facing the most exposure to commodities have been hit the hardest in recent months, particularly the E&P and drilling segments. According to EnerCom’s Weekly database, the stock performance of the two respective segments has dropped an average of 46% and 50% year-to-date. Upstream MLPs have fared even worse, falling by 53% in fiscal 2014. The metrics of various MLPs can be accessed in EnerCom’s MLP Scorecard, a weekly feature that began running in September.

Unlike MLPs in the midstream sector, upstream companies are much more exposed to commodity prices due to their focus on production. Midstream MLPs serve more as “toll takers” and are subject to more consistent cash flows. The yields presented by the upstream MLPs are also much higher, raising questions on if the group can continue to meet their investor friendly policies in a sub-$60 oil market.

Firms Slashing Target Prices

The target prices of upstream MLPs could be confused with a Black Friday fire sale. Several investment firms, including Baird Energy and Wunderlich Securities, drastically reduced both their outlook and target prices on upstream MLPs in recent investor notes.

The target prices of upstream MLPs could be confused with a Black Friday fire sale. Several investment firms, including Baird Energy and Wunderlich Securities, drastically reduced both their outlook and target prices on upstream MLPs in recent investor notes.

“If oil prices do not rally, upstream MLPs will be forced to cut distributions to realign their balance sheets and costs of equity with the new oil paradigm, which we see as structurally lower for the foreseeable future,” says the Baird note. “Overall, we believe MLP investors should avoid the upstream MLPs and focus on non-cyclical subsectors such as crude logistics and retail fuel distribution.”

The firm downgraded six companies and cut the target prices on eight companies by an average of 32%.

Wunderlich was even more bearish, cutting price targets on nine companies by an average of 39% in a note on December 18, 2014. The firm explains: “Unfortunately there is more pain coming in early 2015 before things get better, hopefully in the latter part of the year. We could see downward revision in 2014 reserve estimates of the companies. The sector is also less than 50% hedged in 2016 and much less in 2017. A low commodity price and a backwardated curve would prevent the companies from layering on additional hedges at least in the near term. A low commodity price, drop in reserves, and a low hedge profile would have negative implications on the companies’ borrowing base redeterminations that would further squeeze their liquidity.”

Source: Wunderlich Securities

Wunderlich identified six positive themes it sees in MLPs, including:

- Growth is a positive but not at the expense of balance sheet and coverage

- Moderate, steady distributions are preferred over high yet inconsistent growth

- Drop downs are favored over third-party acquisitions

- A balanced commodity sheet is preferable and provides insulation from one-sided price drops.

- Value of hedges can never be overemphasized

- Coverage and balance sheet strength

The firm believes both commodity prices are still unstable and the swing in oil prices overshadowed movement on the gas side. Therefore, hedging was again singled out as a “paramount” asset of upstream MLPs.

“Most of upstream MLPs have robust oil hedges in 2015 with an average floor price of ~$90/Bbl; however, hedges significantly weaken in 2016,” says Wunderlich. “The low oil price environment and a backwardated curve would also prevent the companies to layer on additional hedges in the outer years, a risk not suitable for the MLP profile. Although we expect commodity to improve toward the back end of 2015, if prices remain low or deteriorate further, valuations of many of these upstream MLPs could remain depressed for a long time. Lack of hedges would also adversely impact the borrowing base redeterminations of the companies, which then affects the liquidity and puts them in a vicious cycle.”

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.