Whiting Petroleum (ticker: WLL), the largest E&P producer in the Williston Basin, shored up its balance sheet this week with a series of debt and equity raises. The deals include:

- Public offering of 35 million shares of common stock at $30.00/share for proceeds of $1.0 billion after deducting underwriter’s discounts and commissions. The underwriter has a 30-day option to purchase an additional 5.25 million shares.

- Private, Rule 144A, unregistered offering of $1.0 billion aggregate principal amount of 1.25% convertible senior notes due 2020, priced at par. The convertible senior notes will be convertible at an initial conversion rate of 25.6410 shares of Whiting’s common stock per $1,000 principal amount of the convertible senior notes, which is equivalent to an initial conversion price of approximately $39.00, which represents an approximately 30% premium to the public offering price per share of Whiting’s common stock in the concurrent public offering of Whiting’s common stock. The initial purchasers have a 30-day option to purchase up to an additional $250.0 million aggregate principal amount of convertible senior notes.

- Private, Rule 144A, unregistered offering of $750 million aggregate principal amount of 6.25% senior notes due 2023 priced at par.

All offerings are expected to close on March 27, 2015. For total considerations, Whiting raised approximately $1 billion in equity and $1.75 billion in long-term debt for total balance sheet additions of $2.75 billion. The total amount may increase to $3.0 billion if options are exercised to purchase additional shares or notes.

Whiting’s Balance Sheet

Whiting became the dominant Bakken acreage holder by acquiring Kodiak Oil & Gas – an all-stock transaction that was finalized in December 2014. Per the terms, WLL also assumed Kodiak’s senior notes in the amount of $1.55 billion, with the earliest of amount of $800 million in 8.125% senior notes due 2019.

Following the merger, Whiting had $2.9 billion drawn on its $4.5 billion credit facility with roughly $3.4 billion in long-term debt. With the recent offerings involved, WLL intends to eliminate the outstanding balance of its revolver and shift its indebtedness to the senior notes, which will total approximately $5.2 billion.

“The $3 billion in fresh capital should allow Whiting to bolster its cash balance, pay off some Kodiak bonds, and repay its credit facility just in time for redetermination,” said Jason Wangler, Senior Vice President for Wunderlich Securities.

The Reasoning

Whiting is one of many energy companies who have tapped into equity markets in recent months. Chevron raised $6 billion in February 2015 to ensure extra capital in the market downturn. The option to reset borrowing terms, rates, covenants, and principal payment dates has been a popular route to take on the cusp of borrowing base redetermination season. Byron Cooley, Senior Vice President of DNB Bank, mentioned to Oil & Gas 360® in a previous interview that current borrowing bases still reflect prices from September 2014, meaning the new redeterminations will be considerably less. Whiting, therefore, intends to wipe its revolver clean and repay Kodiak bonds before the bank reevaluation.

“[It] makes sense for the company to tap capital markets while the window is still open as it addresses Street/investor’s primary concerns, closing 2015 funding gap (2015E: ~$1.1B) and strengthening the balance sheet,” says a note from Wells Fargo Securities. “Furthermore, the capital raise enables the company to remain flexible in monetizing midstream assets, which should lead to a higher transaction value than the alternative.”

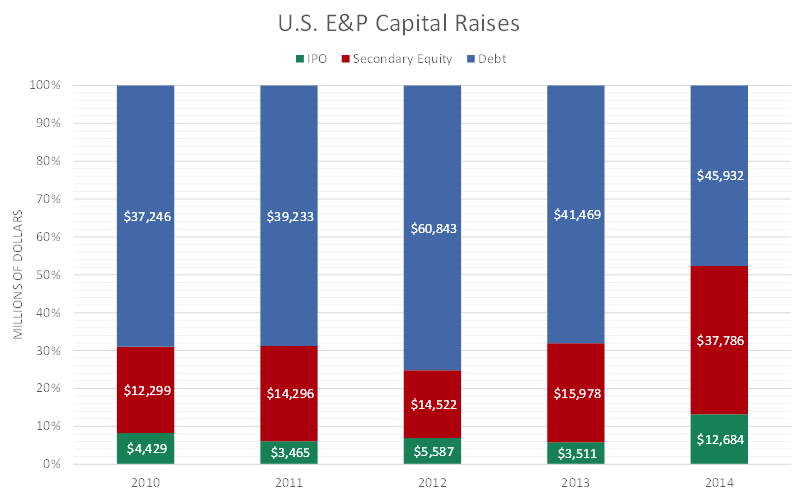

For management teams at public companies, the river of capital they can tap into includes both equity and debt, while private operators are generally dependent on some form of debt, usually secured by their proved reserves. Over the past five years, U.S. and Canadian E&Ps have raised over $349 billion in capital from IPOs, secondary equity offerings and debt, as illustrated in the chart below, which shows the proportion of capital raised by type from 2010 through year-end 2014.

By far, debt has been the most popular type of capital for E&P companies to raise. There are several good reasons to employ debt rather than equity, including:

- It’s non-dilutive to share count and the outflow of cash in the form of interest payments is deductible;

- Reduces the weighted average cost of capital as debt is generally less expensive than equity;

- The holders of the debt capital instrument are senior to the equity holders and will tend to hold the debt longer;

- It’s easier to raise as it provides a steady state flow of cash to the holders of the note.

Resetting Today for a Better Tomorrow…

Companies began accessing the equity market last month, which at first glance seemed counterintuitive given the depressed equity valuations. However, new capital inflows have happened with companies like Plains All American Pipeline (ticker: PAA), Synergy Resources (ticker: SYRG), Newfield Exploration (ticker: NFX), Encana Corp (ticker: ECA) and Noble Energy (ticker: NBL) raising more than $16.1 billion in follow-on equity and $49.2 billion in debt instruments. By comparison, in all of 2013, $15.9 billion of follow-on equity and $41.5 billion of debt was raised.

The rapid change in crude oil prices is unprecedented. Although there have been eight up and down crude oil price cycles since 2007, the severity of the present cycle is without par. The timing of the current cycle was unfortunate as companies were in the midst of setting up their 2015 capital budgets to maintain their growth strategies. The year-to-year change in capital spending is expected to be approximately a minus 43% for the E&P sector and a minus 24% for oil field service companies. We anticipate that going through the minds of every investor and executive in the North American energy business are these primary factors:

- The ability to endure the down cycle without losing strategic competitive advantage;

- The potential to acquire assets from financially distressed companies needing to raise cash;

- The prospect of emerging from the current cycle with positive momentum;

- The ability to tap the capital markets to fund plans and refinance debt coming due;

- The likelihood of banks to cut revolving credit facilities, or change their own “debt metrics,” e.g., only lending on a lower percentage of PDPs.

The dilution effect of the equity issuances is real. In a March 13, 2015, EnerCom, Inc. case study, the average equity dilution for the secondary offerings we analyzed was 19%, ranging from a low of 6.8% to a high of 33%. Somewhat counter intuitively, the average six-day equity market reaction to the equity raises was a positive 1%, ranging from a high of positive 23% to a low of a minus 20%.

Whiting’s dilution, including the allotment of extra shares, would be 24%. The $30.00 price at which the company went to the market was about a 20% discount from the previous day’s market close, but the shares closed at $31.54 on March 26.

Canaccord Genuity weighed in on the Whiting equity transaction, saying “The planned sale of common stock, along with both convertible and non-convertible debt, should help alleviate near-term liquidity concerns, but dilution from the equity and convert issuance should put pressure on the share price in the short term.”

Firms revised their respective price targets downward to account for WLL’s share dilution, but Wangler believes the drop has created an opportunity for investors. “We like the value proposition versus other medium-cap oil names as Whiting’s finances are in good shape and now operations can be the focus,” he said.

…I Love You, Tomorrow…

The senior notes also provide Whiting with longer track for growth. As mentioned, the first of its notes mature in 2019, providing the E&P with an extended lifeline to exploit its Bakken and Niobrara assets. The company reduced its overall rig count to 13 from 25 in response to the downturn and expects production to remain flat year-over-year in 2015. WLL’s demonstrated efficiency as an operator is also apparent, as its Bakken/Three Forks wells are projected to average $7 million – down from $8.5 million in 2014. Its Niobrara wells are expected to cost $5 million and have a 450 MBOE type curve, which KLR Group estimates provides 20% to 25% internal rate of return (IRR). The Williston type curves are especially high at 700 MBOE, which generates an estimated IRR of 35% to 40%. Raymond James’ wrote in a note on March 25: “While the capital raise was far more dilutive than we had initially anticipated, Whiting’s balance sheet will improve meaningfully moving forward, letting the company focus once again on its post-Kodiak high-graded inventory.”

The Kodiak acquisition also bolstered Whiting’s reserve base, which grew by 29% year-over-year (pro forma the acquisition) to 780.3 MMBOE. An estimated 47% is proved undeveloped properties and includes 14,226 future gross drilling locations (53% in the Bakken) in Whiting’s portfolio. Its rising efficiency in the field allows WLL the freedom to expand its operations at cost-effective margins, as evidenced by the asset intensity model in EnerCom’s E&P Weekly. Asset Intensity, defined as the percentage of every EBITDA dollar required to maintain production, is just 44% for Whiting, meaning $0.56 of every EBITDA dollar earned can be reinvested into increasing production or addressing the balance sheet. Whiting compares favorably to its peers: the median intensity of its 86 E&Ps is 59%, while the median intensity of 21 other mid-sized producers is 66%.

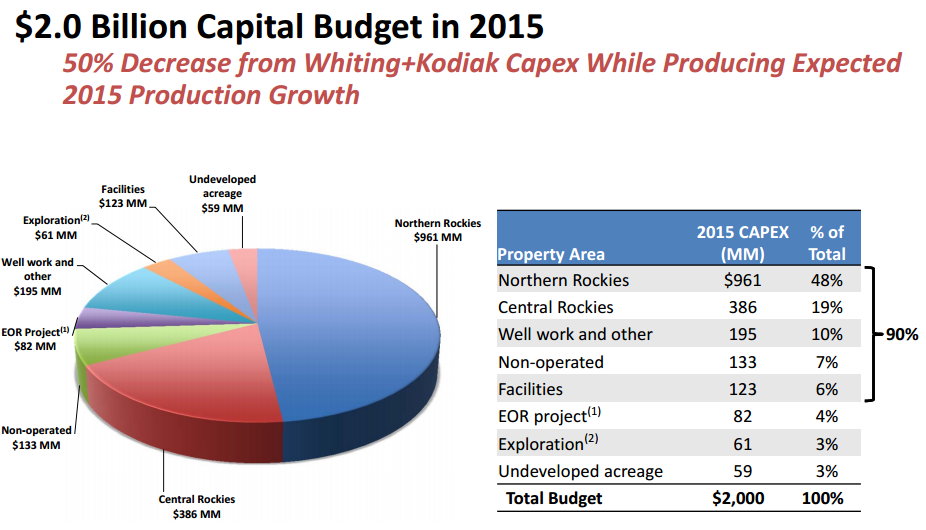

Whiting management mentioned it is also pursuing the sale of “select assets” for up to $1 billion to either reduce debt or add liquidity. The proceeds from the potential sale will further lower WLL’s debt/EBITDA multiple, which Wells Fargo and KLR Group place at respective multiples of 4.0x and 3.2x. Whiting will be fully financed for 2015 once the sales are completed, considering its $1.1 billion of availability and its estimated budget of $2.0 billion.

Baird Energy Research places the multiple even lower at 2.8x, and adds: “We view this level of indebtedness as manageable with further production growth and potential realization of contango implied in the futures strip to offer opportunities for leverage reduction going forward.”

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.