Whiting Petroleum stays on target with capex budget while exceeding production forecast

Denver-based Whiting Petroleum (ticker: WLL) announced its fourth quarter and year-end numbers today. The Williston-focused company reported that average production for the fourth quarter averaged 118.9 MBOEPD, above the company’s high end for guidance of 117.4 MBOEPD, which also translated into higher than expected cash from operations. Whiting said that cash from operations reached $236.8 million, more than twice the $114.9 million the company spent on capex for the quarter, according to WLL’s press release.

Production in fourth quartered totaled 10.9 MMBOE, comprised of 84% crude oil and natural gas liquids (NGLs). Enhanced completions contributed to production exceeding guidance and to lease operating expense (LOE) per BOE coming in at the low end of guidance. LOE also benefited from the sale of higher cost properties and continued efficiency gains in the field, Whiting said.

In addition to the stronger than expected operational results, Whiting also reported that it closed its sale of its North Dakota midstream assets for approximately $375 million, and redeemed all of its outstanding $275 million of 6.5% senior subordinated notes due 2018. Since March 2016, the company has paid off $2.4 billion, or 42%, of its debt.

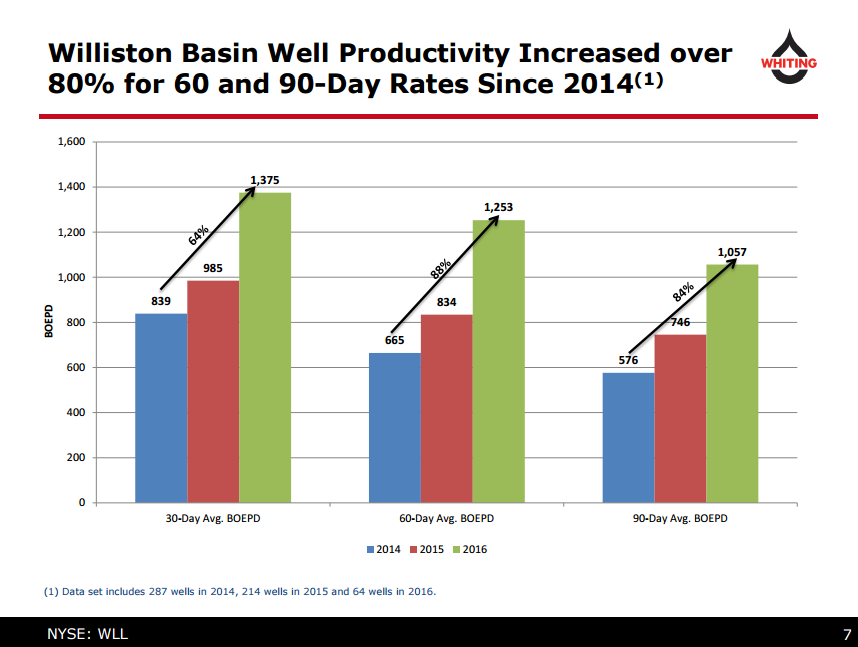

“In 2016, we worked to position the company for strong growth through balance sheet improvement and a focus on operational improvements that resulted in a 42% increase in per well productivity over 2015,” said Whiting Chairman, President and CEO James Volker. “In 2017, we are focused on increasing production, reserves and net asset value through a capital efficient plan that further enhances our balance sheet metrics through growth. We project a total capital budget of $1.1 billion in 2017. Based on this capital plan, we forecast that production grows 23% from first quarter to fourth quarter 2017.”

With the repayment of its notes due 2018, Whiting now has zero bond maturities until 2019. The company also reported that it has $500 million drawn on its $2.5 billion borrowing base as of February 2, 2017.

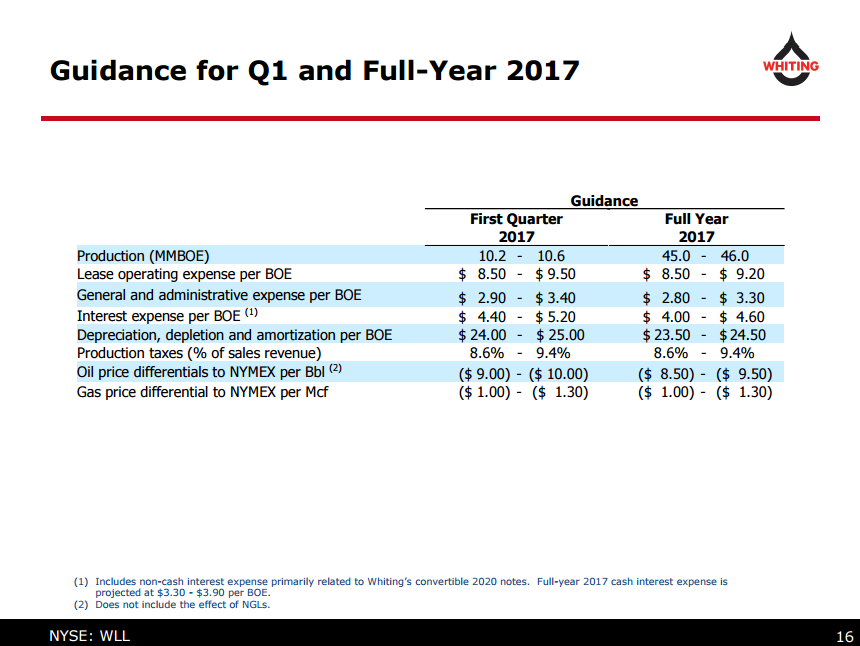

Whiting projects 45.0 to 46.0 MMBO of production for 2017

The company said that, based on its 2017 capital plan, it forecasts 2017 production of 45.0 to 46.0 MMBO for the year, or 123.0 to 126.0 MMBOEPD. Production is forecast to increase to a fourth quarter average rate of 140,000 BOEPD, according to Whiting. This equates to a 23% projected increase from first quarter to fourth quarter 2017.

Whiting announced that it plans to spend $1.1 billion in capital expenditures over the course of 2017. WLL said that 96% of that would be used to develop its core Williston Basin and DJ Basin properties.

Whiting plans to run five rigs and spend $580 million on development activities in the Williston Basin where it targets the Bakken/Three Forks formations and the company said it would run one rig and spend $420 million on development activities in the DJ Basin where it targets the Niobrara “A”, “B” and “C” zones and the Codell/Fort Hays formations.

The DJ Basin activities include the planned completion of 105 drilled uncompleted (DUC) wells. In addition, $60 million has been budgeted for non-operated drilling located primarily in the Williston Basin, the company said in its release.

Whiting’s proved reserves at the end of 2016 totaled 615.5 MMBOE, the company said. Of that, 47% of year-end 2016 proved reserves were proved developed reserves and 81% of year-end 2016 proved reserves were crude oil and NGLs. Adding back asset sales that totaled 114.4 MMBOE and applying a price neutral (equivalent to the SEC 2015 price deck case of $42.75 per barrel of oil and $2.49 per MMBtu of gas) scenario, proved reserves would have totaled 851.5 MMBOE. This represents an increase of 4% relative to year-end 2015 despite a 76% decrease in capital spending from $2.3 billion in 2015 to $554 million in 2016.