Whiting Petroleum Corporation (ticker: WLL) is an independent oil and gas company that explores for, develops, acquires and produces crude oil, natural gas and natural gas liquids primarily in Williston Basin and Permian Basin regions of the United States. The Company’s largest projects are in the Bakken and Three Forks plays in North Dakota, Redtail Horizontal Niobrara development in the Denver Julesburg Basin in Colorado, and North Ward Estes, its enhanced oil recovery field in Ward and Winkler Counties, Texas.

Whiting management said the company’s objective is to generate double-digit production growth while maintaining a healthy balance sheet. The company expects to grow production in 2014 by 17% to 19% over the previous year, assuming a 2014 capital budget of $2.7 billion.

Whiting reported production of 9,000 MBOE, or roughly 100.1 MBOEPD (88% liquids), in its Q1’14 earnings release on April 30, 2014. Discretionary cash flow reached $482 million, a company record, and net income totaled $109.1 million ($0.92 per share).

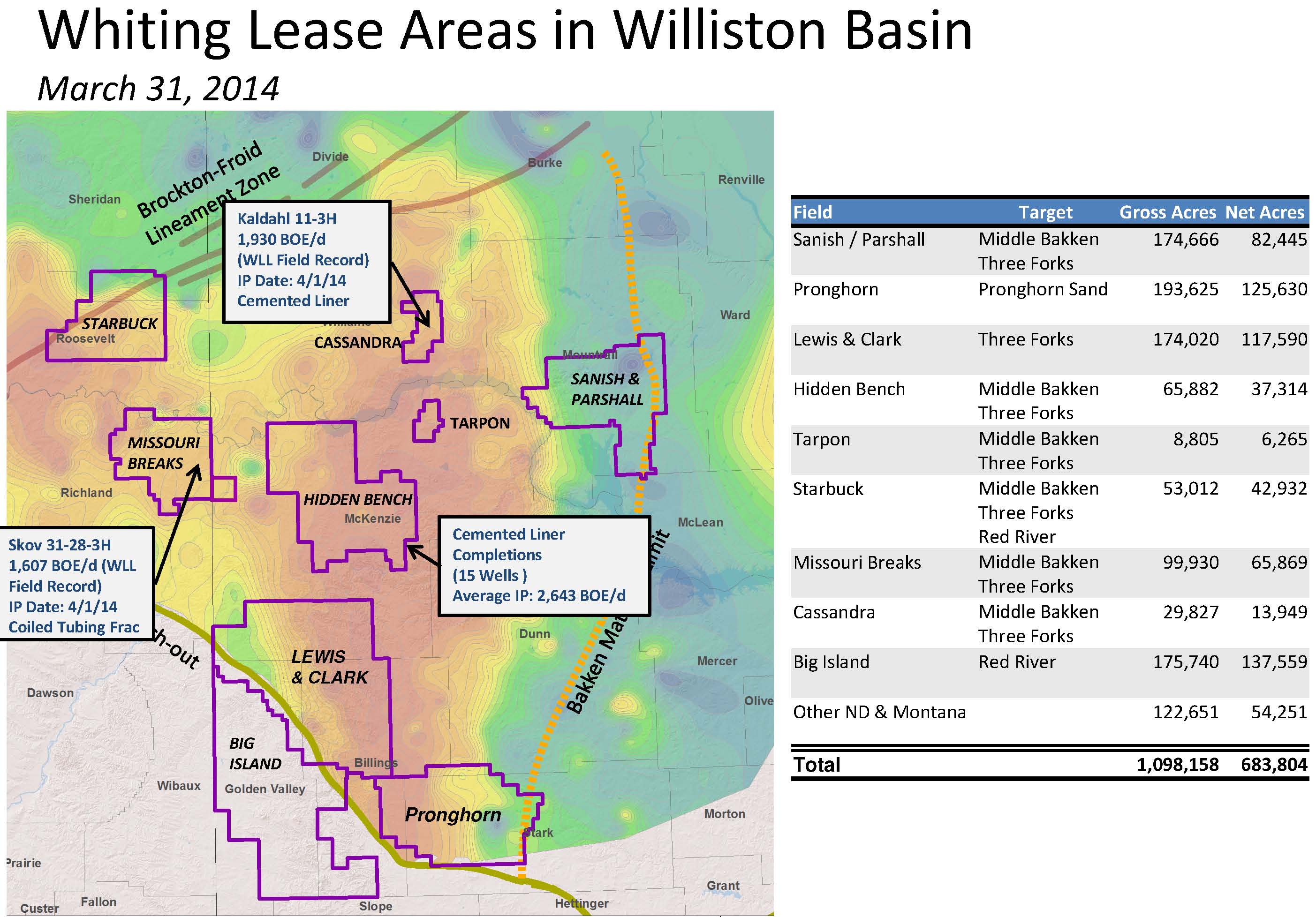

Williston Overview

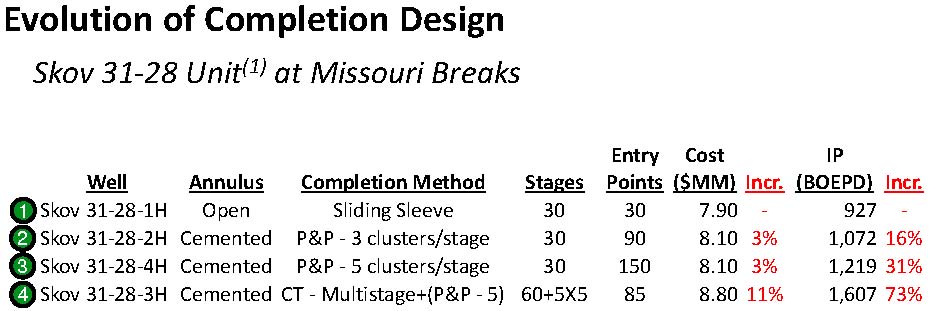

The lion’s share of WLL’s production is sourced from the Williston Basin, where the company boosted rates to roughly 73.3 BOEPD in the quarter (27% higher than Q1’13). The Williston represents 73% of the company’s overall production volume. The use of new completion methods in the Missouri Breaks Field are increasing returns, and the use of coiled tubing fracs resulted in an IP rate of 1,607 BOEPD at one of its Skov wells. Additional Skov wells have posted IP rates of 927 BOEPD through a sliding sleeve and an average of 1,145 BOEPD from cemented liners.

In the Hidden Bench Field in the Williston, WLL has completed its first 15 wells in the field using cemented liners, generating average IP rates of 2,643 BOEPD per well. WLL plans on doubling its downspacing program, increasing the number of wells per spacing unit to eight, up from four across each 1,280 acre drilling spacing unit (DSU). The company is doubling downspacing programs for the Sanish Field as well, and expects to drill nine wells per DSU. The liner method was also used in the Cassandra Field and three wells produced an average IP rate of 1,516 BOEPD, with the Kaldahl 11-3H flowing at 1,930 BOEPD. The three recent wells are producing 38% higher than 10 prior wells completed in the region, with the Kaldahl nearly doubling the production of its peers.

In a conference call following the release, WLL management said the wells are beginning to lean towards the high end of its estimated ultimate recovery of 400-600 MBOE. Future plans include downspacing its Pronghorn assets late in the year and resuming testing in the Missouri Breaks. The Cassandra region will be addressed in the future.

Coil Tubing Benefits

New completion techniques using coil tubing are increasing recovery rates, and WLL management said the cemented liner triples the number of entry points into the shale. The use of coil tubing further increases the entry points and is more effective.

Jim Volker, Chairman and Chief Executive Officer of Whiting Petroleum, said: “You don’t have to pump as much fluid. The pump comes down. It’ll clean the wellbore when you’re done, so you don’t have to clean it out. And you can put it immediately on production, plus faster to frac it that way too.”

Mark Williams, Senior Vice President of Exploration and Development, said, “I really can’t see any reason why this wouldn’t be very widely applicable. It really allows us to get more entry points in all these tight rocks.”

Redtail Draws Interest

The most intensive downspacing program, however, is in the Redtail Niobrara Field. Volker said: “We continue to believe that Redtail is a Whiting within Whiting. We’re blessed in this area. We’re blessed because we have great services to the North of those two takeaway interstate pipelines. We’re blessed to the East of us with a very large takeaway oil pipeline. We have the Denver oil market. We have the Wyoming oil market. And, most importantly, we have the plethora of data that is available to us from old logs that go all the way back into the 1940s, 1950s and 1960s.

“So this was the playground for the Denver independent. So we have an excellent idea of the thickness of the Niobrara A, B and C benches. It crossed our entire acreage position. And so, while one may thin or one may thicken in a particular area, we’re highly optimistic about the entirety of our acreage position working in at least one or two zones across the acreage position. And we’ve seen nothing to deter us.”

WLL is currently focused on only the Niobrara A and B zones, while the Niobrara C and Codell formations are prospective. The company plans to develop its acreage using a 16-well per DSU pattern (on 960 acres), providing more than 3,300 gross locations. The company is testing a 32-well equivalent program in May 2014 and, if successful, will double WLL’s potential drilling locations. Production from Redtail averaged 4,550 BOEPD for the quarter – a 41% increase compared to Q4’13. Type curves are established at 420 MBOE per well. Management said it plans on drilling 1,000 wells in the region as part of its five-year plan.

The company also began regional gas sales in the quarter and has a current gross inlet rate of more than 8 MMcf/d. The plant’s current net capacity of 20 MMcf/d will increased to 70 MMcf/d by Q1’15. The remaining interests in the Big Tex prospect were sold for $76 million, bringing total divestures in the area to $227 million in proceeds ($3,100 per net acre).

The progression in the Redtail Niobrara Field, along with production rise in the Williston, has WLL forecasting a sequential quarter production increase of 9% in Q2’14. Full-year production guidance is expected to reach 40.2-40.8 MMBOE – approximately 18% higher than fiscal 2013 production and 34% higher than 2012 production, pro forma for the Postle sale. The company has 53% of the its remaining 2014 production hedged to solidify the upward trend. None of Whiting’s credit facility has been withdrawn and the company has $400 million in cash on hand.

Valuation Perspectives

OAG360 notes Whiting holds favorable indices when compared to 87 peer companies in EnerCom’s E&P database. WLL’s asset intensity as of May 2, 2014, is 48%, meaning 52% of its free cash flow can be invested into growth opportunities. This compares to a median asset intensity of 62% for the 87 companies in EnerCom’s E&P database.

With a 31% ratio of debt to market cap, WLL’s leverage is also below the peer median level of 37%.

The two metrics indicate Whiting has managed its debt while simultaneously replacing its reserves.

WLL’s share price, however, trades at a 4.3x multiple to cash flow, as compared to an average of 6.3x for 25 of its mid-cap peers. EnerCom’s Five Factor Model anticipates that WLL’s P/CFPS multiple could rise to 6.7x, given the strength of past performance continuing into the future. In its last presentation, WLL reported 438.5 MMBOE of reserves – enough to last 13 years in the company’s proved reserves to production ratio. A total of 7,479 net drilling locations have been identified, a growth of 41% on a year-over-year basis.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication.