Russia Experts Discuss How Today’s Commodities Prices and Shifting Market Dynamics are affecting the Russian Oil & Gas Industry in this Exclusive Oil & Gas 360® Analysis

Around the world, in places where oil and gas is a dominant resource, countries, kingdoms, companies and individual billionaires have been created by the extraction and sale of these fuels. The continuing importance of oil and gas production as a global economic engine can’t be overstated. This is nowhere more evident than in Russia, where 50% of the federal budget, 70% of export revenues, and 25% of the country’s total GDP comes from energy exports.

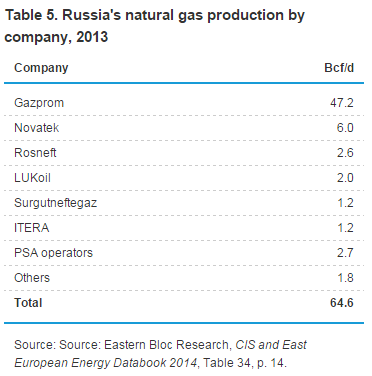

The Russian oil and gas industry is dominated by giants. The state gas giant, Gazprom (ticker: OGZPY), has reserves of 36 trillion cubic meters (1.27 quadrillion cubic feet), making up 72% of Russia’s gas reserves and 17% of global reserves. The company produces approximately 70% of the Russia’s natural gas and currently holds a monopoly on gas exports out of the country. In 2014, Gazprom reported profit from sales of 1.43 trillion rubles (about $37.6 billion, assuming an average 2014 ruble-to-dollar ratio of 38:1).

The Russian oil and gas industry is dominated by giants. The state gas giant, Gazprom (ticker: OGZPY), has reserves of 36 trillion cubic meters (1.27 quadrillion cubic feet), making up 72% of Russia’s gas reserves and 17% of global reserves. The company produces approximately 70% of the Russia’s natural gas and currently holds a monopoly on gas exports out of the country. In 2014, Gazprom reported profit from sales of 1.43 trillion rubles (about $37.6 billion, assuming an average 2014 ruble-to-dollar ratio of 38:1).

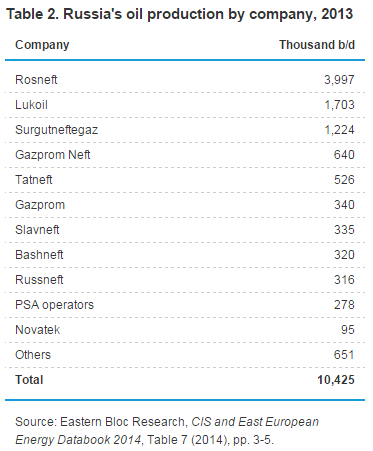

Rosneft (ticker: RNFTF), the state-run oil company, is the world’s largest publicly traded petroleum company with approximately 33 billion barrels of oil equivalent in reserves (41.8 MMBOE 1P reserves) and accounts for more about 40% of Russian oil production. The company’s downstream assets include nine large refineries, as well as 4 “mini-refineries,” which combined have overall annual capacity of 0.6 million tons of oil per annum, in Russia alone. Including its refiners in other parts of the world, the company processed more than 90 million tons of oil in 2013. The company’s 2014 sales revenues totaled 5.5 trillion rubles (about $144.7 billion, assuming an average 2014 ruble-to-dollar ratio of 38:1).

Other major players in the Russian industry include Lukoil (ticker: LKOH), which produces about 1.5-2.0 million barrels of oil per day, Novatek (ticker: NVTK), which is developing Russia’s 16.5 million ton per annum Yamal LNG project, Bashneft (ticker: BANE), and a few other vertically-integrated major players making up 95% of the countries production, while Russian energy experts say between 150-200 smaller regional companies make up the remaining production.

In 2014, Forbes identified the world’s richest billionaires. Five of the ten wealthiest oil and gas billionaires were Russians, according to Offshore Technology magazine’s analysis of the Forbes list.

Money from the export of oil and gas fuels economic growth in Russia, but with oil prices at less than half their year-ago value, and increasingly tense relations driving a wedge between Russia and the political West, the outlook for the country’s lifeblood looks increasingly uncertain.

To better understand the significance of the oil and gas industry to Russia, and how the world’s largest producer of crude oil, and second-largest producer of dry natural gas sees the world market today, Oil & Gas 360® spoke with Dr. James Henderson, senior research fellow at the Oxford Institute for Energy Studies, and Dr. Tatiana Mitrova, head of the oil and gas department at Energy Research Institute RAS, coauthors of a study published in September titled “The Political and Commercial Dynamics of Russia’s Gas Export Strategy.”

In their research, Henderson and Mitrova found that commercial and political circumstances have combined to put Russia and its energy industry in a tight spot, though perhaps not as pessimistic a place as is sometimes portrayed.

The combination of company and state: Russia’s reaction to changing commercial circumstances

Because of the prominent role of the government in its major producers, the two companies, especially Gazprom, which has an export monopoly, are often viewed as tools of coercion.

“I think one of the most common misconceptions [about the Russian oil and gas industry] is the weapon, the threat, that [the industry] offers,” Henderson said. “Exports and prices are used as a political tool, but mainly it’s used to offer discounts. For sure, various countries have been offered discounts in order to get pipelines built, or keep them in the Russian sphere of influence, but what’s happening now is Russia is being forced to react to changing commercial circumstances.

“The whole concept of a ‘gas weapon’ has really diminished. I think the whole mentality, the picture of Putin standing by a pipeline near the flange to turn the lights off in Europe, is one that is massively exaggerated.”

Government comes first, but not at the peril of the Russian oil and gas companies

The government’s goals are always considered when making a decision, like helping develop heavy oil production in Venezuela or shutting off gas transit through Ukraine, but the companies must remain commercially viable. “There’s no point in the state bankrupting its major company to achieve a political goal because then the company is essentially unable to achieve either commercial or political objectives,” said Henderson. “It’s a balance.”

A good relationship with the state is necessary to do business in Russia, say the researchers. Even private companies heed the word of the Kremlin. “These are the rules of the game,” said Mitrova. “Companies understand that without a favorable attitude from the state, their operational activities will be much more difficult. You must have a good relationship with the state in order to function without problems.”

Unbundling Gazprom

One of the structural changes that is often proposed for the Russian oil and gas industry is unbundling the state’s gas giant, and allowing other companies the opportunity to export. In the early 2000s, gas market liberalization was being explored by Russia until President Putin put a halt to those talks, said Mitrova.

“Now these talks are back, and now they are inspired by Rosneft and Novatek, Gazprom’s major competitors,” she said. “They are trying to promote the idea of splitting Gazprom into a transportation company and several potentially private upstream companies to liberalize domestic markets, to move to the spot market, and to liberalize exports.”

Despite the pressure from within to change the structure of Russia’s main export vehicle, both Henderson and Mitrova agreed that the chances of such a drastic unbundling were remote at best. “Frankly speaking, I think this is the least favorable market to discuss market liberalization you could imagine,” said Mitrova.

“Russia is currently in a siege mentality, and I think the last thing the Russian state would do is create what would be a pretty chaotic situation by breaking up its major gas producer, as well as one of its major commercial and political tools,” said Henderson.

Some of the issues are being addressed in Russia, from the idea of allowing other companies to export, to the state taking 100% control of the pipelines. The most likely outcome, Henderson believes, is that Gazprom will act as a coordinator, or hold the export contracts while sourcing the gas from other companies.

Shifting European market conditions, production surplus points Gazprom toward China

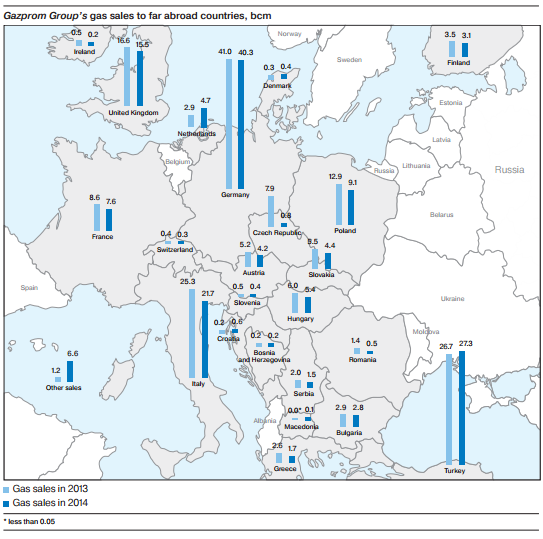

Historically, Russia’s main buyer for energy exports has been Europe and the former Soviet Union (FSU), but with political relations souring over Russia’s involvement in Ukraine, many of those countries are now looking for ways to diversify supply in order to reduce their dependence on Russia. With U.S. shale gas coming to Europe in the form of liquefied natural gas (LNG) on the horizon, renewable energy in Europe becoming increasingly pervasive, and increased competition from other companies in Russia, the state’s energy giant Gazprom has been left with a surplus in capacity totaling as much as 100 billion cubic meters per annum, according to Henderson and Mitrova.

Gazprom hoped to solve the overhang in its production by finding new outlets in markets to the East, especially in China where sales have been contemplated by Russia since the 1990s. Unfortunately for Russia, China used the gas giants weakened bargaining position to obtain deals that Gazprom might not have agreed to at other times. This, combined with slowing demand in China, has left Russia without much leverage in negotiations with eastern markets.

Add on top of that sanctions from the U.S. and Europe over Russia’s involvement in Ukraine, cutting off vital financing for capital intensive projects like LNG, worsening political relations sending Russia’s key market looking for new supplies, and prospects for the Russian oil and gas industry look dark, to say the least.

Most catastrophic scenario we could have imagined

“It’s definitely not the future we were looking for,” Mitrova told Oil & Gas 360® from Moscow. “It’s quite an unpleasant surprise. The whole development of the market for both oil and gas in Europe and Asia is quite disappointing. I would even say it looks like the most catastrophic scenario we could have imagined if we had tried to draw the most pessimistic scenario five years ago.”

The effects of sanctions on Russia

Sanctions from the U.S. and Europe have come in two broad types: technological and financial. The technological side of the sanctions regime prevents companies in the West cooperating with their Russian counterparts in the energy sector through the exchange of technologies used in support of the exploration or production of oil or gas from deepwater, Arctic offshore, or shale projects, according to the U.S. State Department. So far, the technological sanctions have not had major impacts, say the experts, but the sanctions cutting Russia off from financial markets are cutting deeper.

Financial sanctions have cut Russian companies off from critical financing to develop new projects and continuing growing. And while only a handful of companies are on the official sanctions list, the fear that more might be added has kept Western banks from giving money to other Russian company.

“Large companies, small companies, state-controlled companies, private companies, it doesn’t matter. The Western banks are being extremely cautious in dealing with them and they prefer to refuse any loan to any Russian company,” said Mitrova. Under the current sanctions regime, loans to Russia can be no longer than 30 days if they come from the U.S., and 90 days if the loans are from European lenders.

This has not delivered a killing-blow to most Russian oil and gas companies, however. Aside from Rosneft, which has a large debt burden from acquisitions of other companies, most companies’ balance sheets are sound, said the two experts.

“The companies themselves, other than Rosneft, have relatively secure balance sheets, so there’s not really any prospect of them defaulting or going bust. What we are seeing is a reassessment of capex budgets,” said Henderson. The inability to access investment could eventually lead to production declines, but Henderson does not believe the Russian oil and gas sector has hit that point yet.

Producing at post-Soviet record levels, but Russia’s financial markets not able to fund growth

In September, the Russian oil and gas industry reached a post-Soviet production record at 10.74 million barrels per day. The gains came in large part from foreign-led projects and Rosneft, according to information from the Russian Ministry of Energy. The ministry’s data showed oil output under production-sharing agreements with foreign firms jumped 10% to 300,000 barrels per day in September from the previous month.

For the time being, Russian oil and gas companies should be able to continue functioning as they are, but the Russian financial system will not be able to support the kind of capital spending required for an industry as investment-dependent as oil and gas in the long-run. “In the modern world, developing any investment project without attracting loans is an unsustainable model,” said Mitrova.

“The Russian financial market is very weak and undeveloped. It is not able to provide sufficient financing for all the investment needs of the Russian energy sector,” she said. “This is the major threat at the moment.”

The pivot east

In order to make up for lost financing from markets in the West, and hopefully expand its customer base into the fastest growing demand center in the world, Russia decided to make a pivot to China. Deals were struck between the two as Russia looked to export the gas Europe was no longer looking to buy to Asia, and also secure financial support from China, but the deals have not amounted to what Russia had hoped for when it first looked to find a new market.

“The problem is [Asia has] seen Russia coming, and they understand that Russia really needs to sell its gas, meaning [Asia] can drive a very hard bargain” Henderson said. “It would be great if [Russia made a successful pivot to Asia]. It would be very useful, but I think what Russia is going to find is that they are going to have a much smaller pivot to Asia over the next ten years, which will leave them very dependent on their Western exports.”

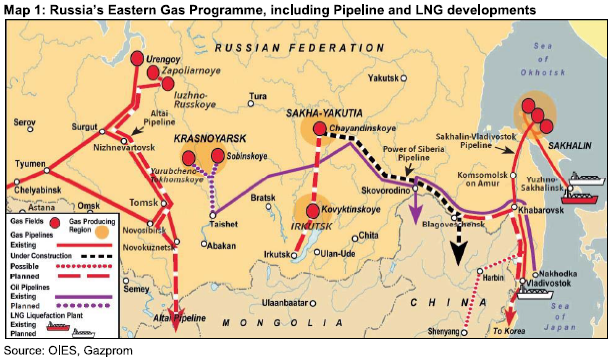

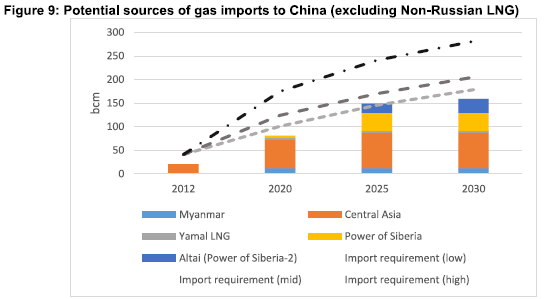

In their report on Gazprom, Henderson and Mitrova discussed the ways in which the gas deal with China for over two trillion cubic feet of gas over the course of the next 30 years was not the deal Russia had hoped to receive. The Chinese insisted on a pipeline route that ran to their major demand centers in the east of the country from eastern Siberia where Gazprom is just beginning to develop, rather than from Western Siberia where gas that would traditionally be shipped to Europe is beginning to create a bubble in the market.

China being extremely cautious

China has been tighter with its purse strings than Russia expected. Gazprom was unable to close on a $25 billion down payment for the Power of Siberia pipeline that would ship natural gas to eastern China, and other loan amounts have been relatively small thus far. “China is being extremely cautious about providing any kind of support,” said Mitrova. Loans from China have been in the range of $7-$8 billion, “for comparison, Gazprom’s investment program alone is more than $30 billion,” she added.

The limitations of Russia’s pivot to the east are quickly becoming apparent to the gas producer as well, said Henderson. “Russia is realizing the situation, and having to adapt their strategy in Europe from one where they can almost threaten the Europeans with ‘we’ll send our gas to Asia if you don’t want to buy it,’ to ‘oh dear, we don’t really seem to have an Asian market, we better make sure the Europeans actually want to buy our gas,’” said Henderson.

LNG projects postponed: a “huge change in the Russian export strategy”

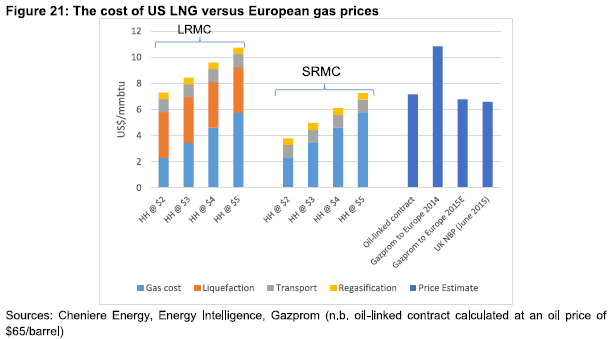

One of the main avenues Russia hoped to use to export its natural gas was by converting it into liquefied natural gas (LNG), but with Western financial markets closed to Russia, and the expertise needed to develop the projects unavailable due to sanctions, Russia has curtailed its development plans. In 2013, the Russian government granted permission for projects operated by Novatek and Rosneft to sell LNG to overseas markets while Gazprom was trying to expand its existing project on the island of Sakhalin and build a new plant at Vladivostok.

“All three companies’ plans have been set back to varying degrees by a combination of political and commercial issues,” said Henderson and Mitrova in their report. “The impact of U.S. and E.U. sanction, in particular on the ability of Russian companies to raise long-term finance, and the fall in oil (and as a result gas) price in Asia have undermined Russia’s prospective LNG projects.”

“At one point, it looked like there were projects that could have seen upwards of 50-70 million tons of Russian LNG in the market sometime in the 2020s,” Henderson told Oil & Gas 360. “Now it’s looking like a total number closer to 25 million tons by the early 2020s and we’ll see what happens after that.”

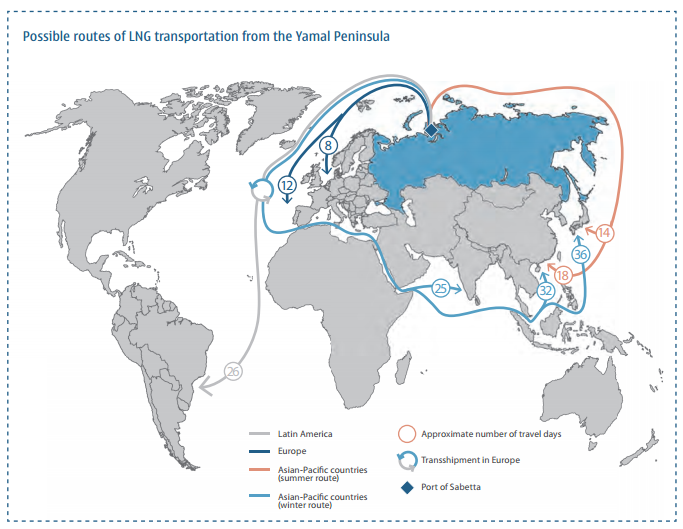

Sanctions, and the fear that they could expand, have effectively put the brakes on Russian LNG development. Even Novatek’s Yamal LNG project is struggling to finalize its financing, turning to Chinese firms to help bridge the gap. In September, Novatek announced that China’s state-run Silk Road Fund agreed to purchase a 9.9% stake in the project, joining CNPC as a Chinese partner.

“Yamal LNG managed to sign all the agreements on equipment supply before the sanctions were introduced,” explained Mitrova. “They are now struggling to finalize financing, especially since Novatek is under direct financial sanctions from the U.S.

“Other projects seem to be postponed past 2020,” she added. “That’s a huge change in the Russian export strategy. LNG is becoming unavailable for a period of time.”

More of a problem for the state than the oil and gas companies

While the cumulative effects of low oil prices, Western sanctions, and a hard bargain from the East has left Russia in a tougher position than it likely imagined before events took a turn for the worse, it is not all doom and gloom in the Russian oil and gas industry, the experts said.

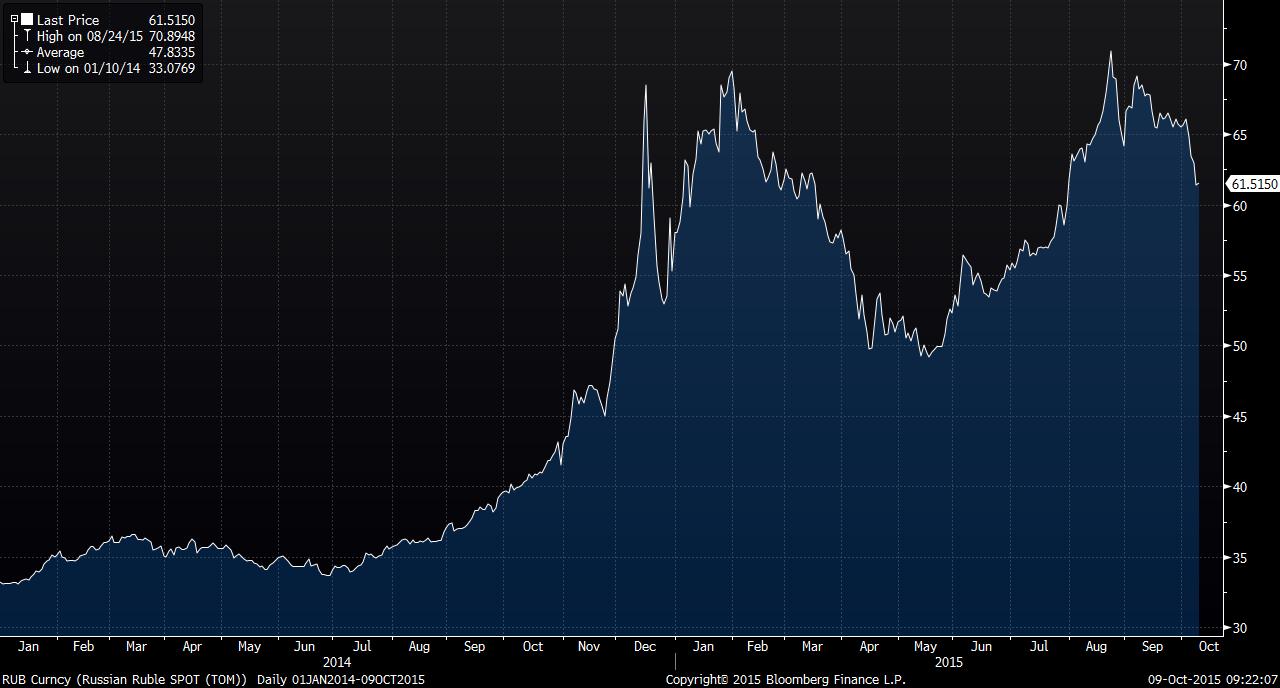

One silver lining for the industry is the significant devaluation of the Russian ruble, which traded near 30 rubles to the dollar from August 2011 to February 2012 when it began to slide following riots in Kiev, Ukraine. Events in Ukraine, and the souring of political relations that accompanied them, would see the ruble devalue as far as 71 rubles to the dollar in August 2015. It has been trading in the mid-60s to the dollar since the beginning of October.

“All of the spending for equipment, and taxes, all of that is set in rubles, while their revenues are in hard currencies like dollars or euros,” said Mitrova. “So actually, they have seen some additional revenues and their margins have either remained the same or, in some cases, increased slightly (in rubles).”

Russia needs oil and gas revenue to fill a hole in the budget

“The Russian government has managed to reduce the size of the budget deficit because of the ruble devaluation. The devaluation obviously isn’t a good thing, and it has impacts on the population, but it does help to offset some of the decline in oil revenues,” said Henderson. “Having said that, there is a hole in the Russian budget that they are hoping to close, to an extent, with the help of more revenues from the oil and gas sector.”

A change in taxation

The Russian taxation system is set up such that oil companies do not see a significant difference in revenues at $40/bbl of oil versus $100/bbl, explains Mitrova. Taxes are based on volumes rather than on profits, so the state sees the biggest gains when prices are high, but also takes the majority of the heat when they fall.

“For the oil companies, [the fall in prices] is not that big of a problem,” explains Mitrova. “Moreover, I would say, if you look at recent statistics, Russian oil companies have even slightly increased their oil production despite all these unfavorable conditions. For them at least, for the next two to three years, I don’t see any troubles or significant threats, except for the governmental policy, the tax policy.

The Russian government usually goes about this in one of two ways, either increasing mineral extraction taxes, or decreasing export duties and increasing upstream taxes. “Literally just this week (week ended October 2, 2015), we’ve seen the Russian government turning to the oil and gas sector and increasing royalty taxes and export taxes in the short term to help finance the budget deficit,” added Henderson.

While increasing the tax burdens on companies will not help them grow in the current commodity down-cycle, both experts agreed that it would not cause a catastrophic event inside the industry. Prices at $25/bbl or lower would spell trouble for the industry said Mitrova, but added that sub-$30 oil would spell trouble for more than just Russia.

Russian oil and gas companies: long term survival not a problem

The sanctions that were put in place to damage the Russian economy have certainly taken their toll, but they may not be as effective as the West hopes, said Mitrova.

“I think the most common misconception during the last year is that people in the West expect that sanctions and financial trouble and low oil prices could lead to a fast change in the Russian oil sector or gas sector, or lead to some revision in the institutional structure or some change in governmental policy.

“It is such an inertial sector, and the reserves accumulated during the previous years are so huge, there is so much room for the improvement in the efficiencies in this sector that, even under external pressure, the Russian oil and gas industry could survive for quite a long period of time without any catastrophic consequences. The country is so huge and these companies are so rich that they can survive under this pressure for a decade, fifteen years, maybe twenty years. It’s a very long-term story.”

Despite the resilience of the sector, it is not impervious. Gazprom, Russia’s main export vehicle has been forced to reconsider pricing mechanisms in Europe as pressure mounts on the Russian natural gas provider. The company announced its first ever spot-market auction in Europe in September as the European Commission turned up the heat on the company over accusations of abusing its position in the market.

As relationships with its traditional market become tenser, Russia is struggling to offload as much gas into new markets as it had originally hoped to be able to do. China’s slowing demand has lowered its need for natural gas, leaving it in a much stronger bargaining position than Russia, and allowing it to push for price concessions and pipeline routes that favor its needs over Russia’s.

LNG, once hoped to be Russia’s next wave of exports with 50 million tons per annum or more on the market, has been forced to cut back as critical financial and technical support is barred from the country by sanctions.

“The fact that the Russian economy is suffering due to the low oil and gas prices shows you that Russia is more reliant on those revenues than we are on [their gas,]” Henderson said from the U.K. While the Russian oil and gas industry may be an economic behemoth, it is still inextricably dependent on the markets on its borders to feed critical revenues into the country.

The country and its industry have amassed a considerable amount of financial reserves to sustain themselves through lean times, leaving them less strained by sanctions than some in the West hoped, but with a pivot to Asia looking less lucrative, both sides have been left in a standoff where neither seems ready to budge.