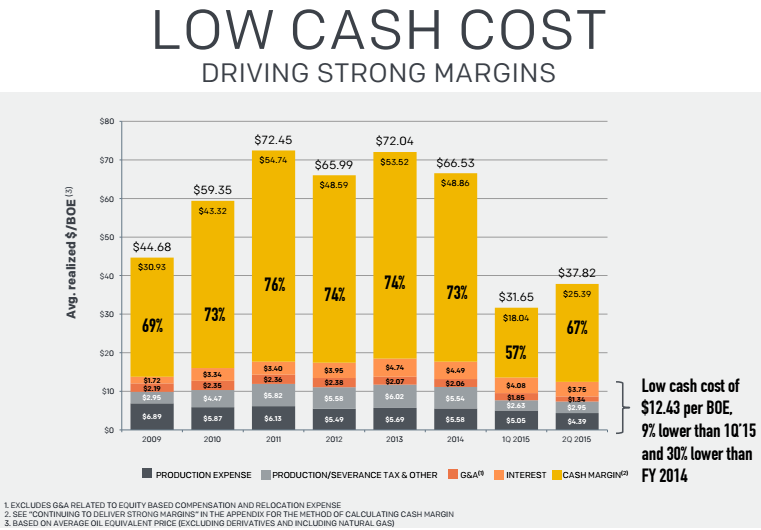

Maintains Guidance Despite 12% Budget Cut

Citing low commodity prices, Continental Resources (ticker: CLR) cut its 2015 non-acquisition budget to $2.35 to $2.40 billion, down from its previous guidance of $2.70 billion. In a company release, management said the adjustment is designed to “better align spending with cash flow at current commodity prices.” Well completion activity will be deferred barring any contractual obligations. Its gross uncompleted well count is expected to rise to 160 from its original plan of 100.

CLR plans on reducing its Bakken rig count to eight by the end of September, down from its current Bakken fleet of ten. The region had 19 CLR rigs at year-end 2014 – the second most of any operator. The company maintains its production growth rate of 19% to 23% and expects to exit 2015 with volumes of 200 to 215 MBOEPD. Continental anticipates spending $1.6 to $2.0 billion in 2016 to sustain a flat production rate.

“While we do not believe today’s low commodity prices are sustainable long term, we are committed to living within cash flow until they recover,” said Harold Hamm, Chairman and Chief Executive Officer of Continental Resources.

The Latest Chapter for CLR and OPEC

Hamm has been one of the figureheads for the North American oil industry in the midst of the commodity crash. The energy magnate has been rather vocal and critical of competition from the Organization of Petroleum Exporting Countries (OPEC), accusing the cartel of trying to “wipe out US production.” In an act of defiance, Continental monetized all of its hedges in its Q3’14 earnings release, issued on November 5, 2014. At the time, the monetization resulted in proceeds of $433 million and allowed CLR and Hamm to “fully participate in what we anticipate will be an oil price recovery.”

Other major E&Ps without any hedges include Apache Corp. (ticker: APA), Cabot Oil & Gas (ticker: COG) and Occidental Petroleum (ticker: OXY). CLR anticipates being cash flow neutral in a $50/barrel environment, while a $40/barrel environment would result in $150 million of overspend. The Oklahoma City-based company currently has about $1.3 billion in available liquidity under its credit facility.