American Eagle Energy Corporation (ticker: AMZG) is a Williston Basin focused E&P company engaged in the exploration and production of petroleum and natural gas in North America. American Eagle has developed 35 producing wells (16.3 net) in its Spyglass area targeting the Bakken and Three Forks formations.

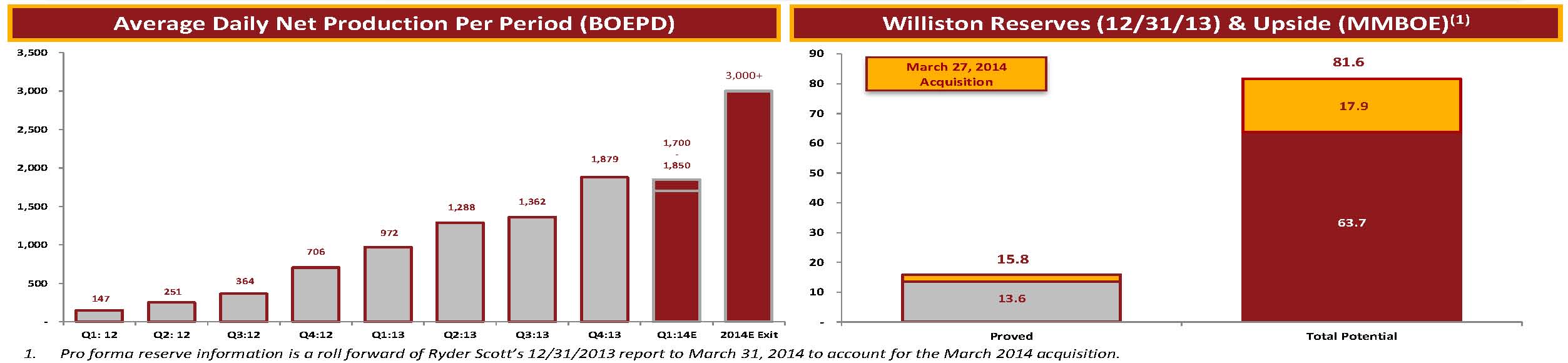

Seven gross wells (3.0 net) were drilled in Q1’14, as reported in AMZG’s quarterly earnings release on May 13, 2014. American Eagle posted quarterly sales of $12.5 million and adjusted EBITDA of $7.4 million – both slight decreases compared to Q4’13 as a result of the brutal winter in North Dakota. The respective totals have still increased by 64% and 52% on a year-over-year basis. Q1’14 yielded a net loss of roughly $1 million ($0.06 per share) but AMZG successfully boosted working interest in its focus area. Management said its PV-10 value of $383 million is 50% higher than its current enterprise value of $250 million.

Production for Q1’14 averaged 1,645 BOEPD (95% oil), but volumes have since recovered from the winter and produced an average of 2,250 BOEPD in the month of April. The streams from last month are increases of 37% and 22% compared to Q4’13 and Q3’13.

In a conference call with analysts and investors, Brad Colby, President and Chief Executive Officer of American Eagle Energy, said: “As we bring more of our recently completed wells on to production, complete our Carry and Farm-Out program and benefit from improved weather in the Williston Basin, we expect production, cash flow and proved reserves to continue to grow significantly.”

Spyglass Focus

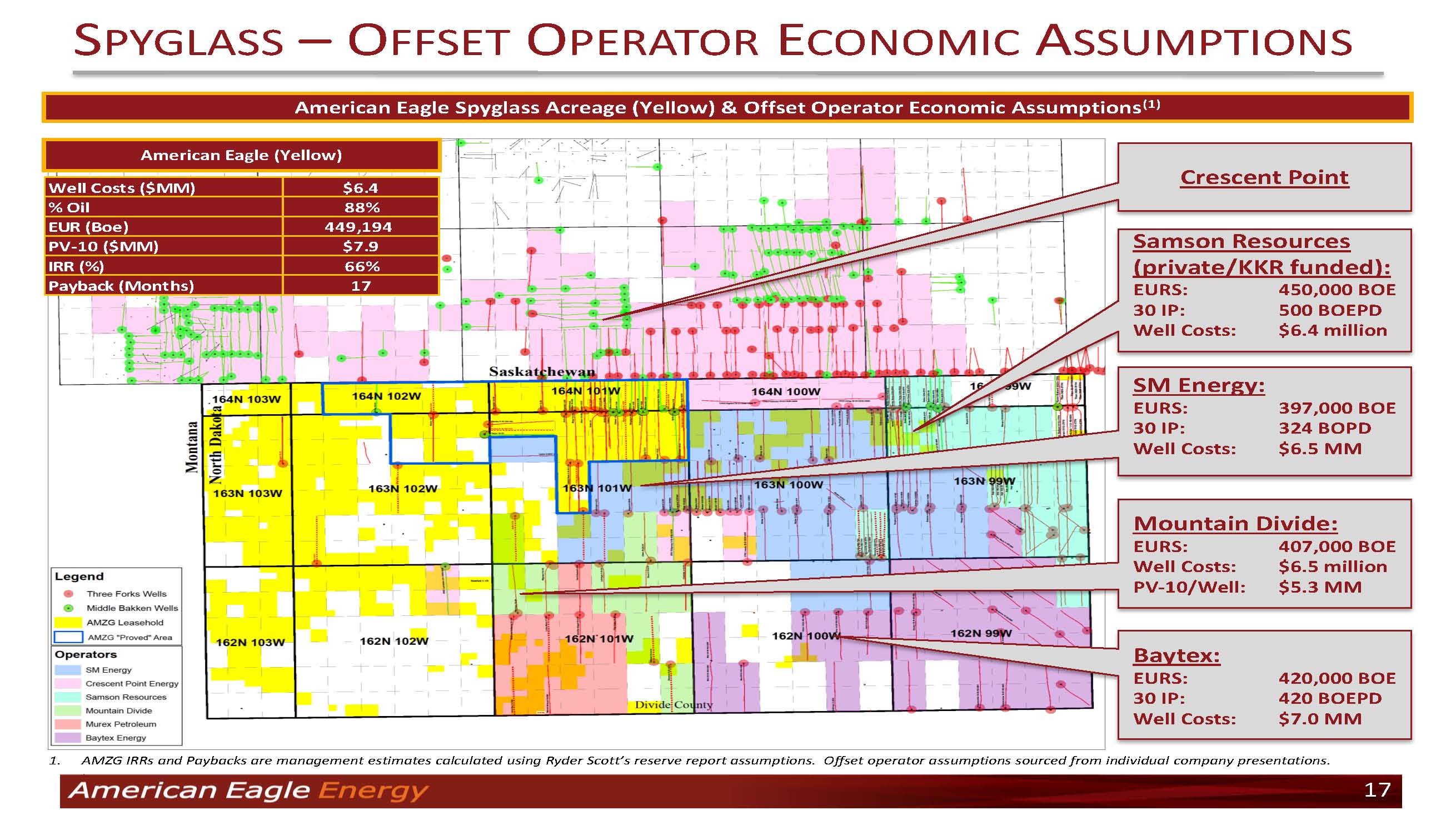

American Eagle’s Spyglass area now consists of 45,600 net acres to the company. AMZG has consistently raised its working interest and footprint in the play for the past year. Its working interest is now 68% in the total area and 67% in the proved Spyglass area. An 8,000 acre addition closed in March and cost less than $1,500 per acre.

“This is a significant increase from the 16,000 net acres, with an average working interest of 25% in our operating area that we had as recently as eight months ago,” said Colby.

AMZG is running a two rig program and the seven gross wells drilled in the quarter produced a cumulative 30-day IP rate of 1,705 BOEPD. Five of the wells were drilled to the Bakken formation and the remaining two wells in the Three Forks were the first wells drilled on their pads. Eight additional operated wells (six in Three Forks) are in various stages of completion, and three Three Forks wells are the first on their respective pads.

“The Bakken wells continue to de-risk and delineate our Spyglass Bakken well locations and should be additive to our future reserve reports,” said Colby in the call.

The company plans on focusing the remainder of 2014 on the Three Forks in the central and eastern areas of its play. An operational update will be released prior to the announcement of its Q2’14 earnings in August. Type curves are established at 315 MBOE to 338 MBOE. AMZG has contracts to hedge more than 80% of production at a $10.75 discount to the WTI spot price.

Operations Guidance

American Eagle expects to bring six gross wells into production per quarter for the remainder of 2014. Total forecasted drilling includes bringing 24 gross (16 net) wells online in 2014 – an increase from its prior guidance of completing 21 gross wells (10 net). The company expected to drill just 18 gross wells in its Q3’13 release. OAG360 notes the increase in net operated wells is reflective of AMZG increasing its working interest through recent transactions.

The company has increased its well development budget to $100 million for 2014 as opposed to its initial guidance of $65 million. The 2014 drilling model, in terms of expenditures and operations, is expected to be similar in 2015. Management placed emphasis on Management says its current two rig program will provide 18 years of inventory.

The company maintains its 2014 exit rate of more than 3,000 BOEPD, which would represent an increase of 33% compared to rates in the month of April. Operations are expected to be funded from its $50.1 million in cash and its $200 million in credit availability, which reflects a recent increase. The company holds $108 million in total debt outstanding.

Crescent Point Enters the Fold

Crescent Point Energy (ticker: CPG) closed an acquisition on May 15, 2014, with CanEra Energy for $1.1 billion in exchange for 260 net land sections north of AMZG’s Spyglass project. The region produces an estimated 10 MBOEPD and CPG plans on drilling 45 net wells through the remainder of fiscal 2014. A breakdown on locations can be seen in the map above.

The low-decline, high-quality production we gain is expected to help drive our total payout ratio down in 2015, which is a key benefit,” said Scott Saxberg, President and Chief Executive Officer of Crescent Point, in a press release following the announcement.

Colby said: “It’s nice to see other operators, much larger than us, are acquiring acreage in the Spyglass area, as we have known for years the low cost wells and flat decline curves in Spyglass for great well economics.”

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.